You're probably somewhere between excited and uneasy right now. You've run the numbers on a fixer, watched other investors post before-and-after photos, and started thinking your first flip could be the project that gets you into the business for real.

That instinct isn't wrong. But first time fix and flippers usually don't get in trouble because the idea is bad. They get in trouble because they underestimate how tight the margins can become once financing costs, delays, repairs, and resale timing all start pulling on the same deal.

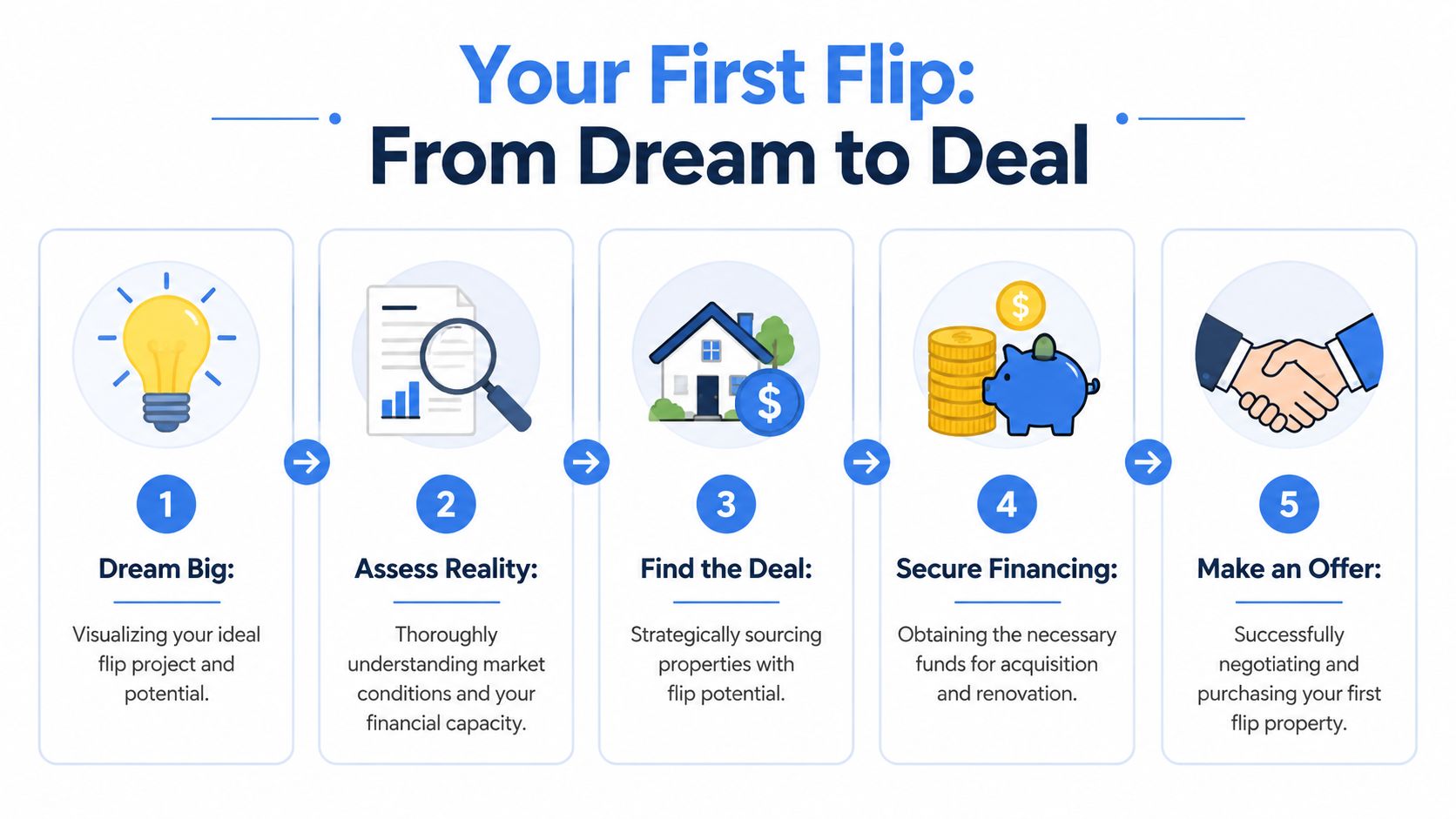

Your First Flip From Dream to Deal

A first flip can work well when you treat it like a business decision, not a HGTV episode. The upside is real. The caution is real too.

According to ATTOM-based benchmarks summarized here, the average gross profit for a house flip is around $73,500, but that number does not include rehab and holding costs. The same source notes that the national house flipping success rate is 88%, which means 12% of projects either break even or lose money.

That's the part new investors need to sit with. A deal can look great on paper and still go sideways if the scope grows, the contractor stalls, or the resale drags.

What new flippers usually get wrong

Most beginners focus on the fun parts first. Paint colors. Kitchen layouts. What the finished listing photos might look like.

Those things matter later. Early on, the actual work is simpler and less glamorous:

- Buy below your margin of error: If you overpay, the rest of the project has to be perfect.

- Protect your timeline: Every extra week usually means more interest, insurance, utilities, and stress.

- Control the scope: A clean cosmetic update is very different from discovering foundation, plumbing, or permit issues after closing.

- Line up the right capital: Slow money can kill a good deal just as fast as a bad budget.

Practical rule: Your first flip should feel boring on paper. If it only works with an aggressive resale price and a flawless rehab, it's not a beginner deal.

What a good first project actually looks like

A solid first deal is usually one with a clear resale story, a straightforward renovation plan, and enough room for mistakes. Not major mistakes. Just normal ones.

I'd rather see a new investor buy a plain house in a steady neighborhood with predictable repairs than chase a “home run” project with complicated additions, layout changes, or uncertain value. First time fix and flippers don't need drama. They need repetition, clean numbers, and a project they can finish.

That's why the roadmap matters more than the dream. The investors who stay in this business are usually the ones who learn how to underwrite conservatively, move quickly when a deal is right, and avoid getting trapped in a project that eats months of time and most of the profit.

How to Spot a Winning Flip Before You Buy

A first-time investor gets excited about a house with a cheap list price, walks it once, and starts picturing the after photos. Then the actual numbers show up. The roof is older than expected, the resale comps were too generous, and the contractor's bid comes in higher than the back-of-napkin estimate. That deal usually goes bad before the rehab even starts.

The buy decision sets the risk profile for the entire project.

Use ARV as your anchor

ARV means after-repair value. It is the price the property should realistically sell for once the work is done and the home matches the local market.

If that number is wrong, everything downstream gets worse. You overpay, borrow against bad assumptions, and leave yourself no room for delays or surprise repairs. I tell new investors to underwrite ARV like a skeptic, not a salesperson.

Use recent comparable sales that reflect the house you will deliver, not the nicest renovation in the zip code. Match size, layout, lot type, location, and finish level. If your plan is a clean cosmetic rehab, your comps should be clean cosmetic rehabs too.

The 70% Rule

A common screen in the flip business is the 70% Rule. The idea is simple. Your maximum purchase price is roughly 70% of ARV, minus repair costs. Many investors use it as a quick way to see whether a deal has enough margin to survive the normal problems that show up during a project. If you want a broader primer on deal structure and capital, this guide on how to finance investment property helps frame the numbers.

The formula is:

Maximum Purchase Price = ARV × 0.70 – Repair Costs

It is a screening tool, not a law. In a very competitive market, some investors stretch it. On a first flip, stretching usually means absorbing more timeline risk, more carrying cost, and less room to correct a bad assumption.

A simple example

Say your realistic resale price is $300,000.

Start with 70% of ARV, or $210,000.

If repairs are $40,000, your maximum purchase price looks like this:

$300,000 × 0.70 – $40,000 = $170,000

That spread is your protection. It covers the things first-time flippers often underestimate, including holding costs, resale costs, contractor change orders, and the possibility that the property takes longer to sell than planned.

What to check before you make an offer

Walk the house with a contractor if you can. If not, walk it like someone who has to write the checks.

I focus on four risk buckets:

- Layout risk: If the house works with the current footprint, your budget and timeline are easier to control. Moving walls, changing room counts, or reworking traffic flow can trigger bigger costs fast.

- Major systems: Roof, HVAC, electrical, plumbing, foundation, and drainage problems can turn a light rehab into a heavy one.

- Comp risk: The finished house needs to fit what buyers already pay for in that neighborhood. Over-improving is expensive and rarely rewarded dollar for dollar.

- Exit risk: You should be able to explain the likely buyer clearly. Starter-home buyer, downsizing couple, small family. If the end user is fuzzy, the resale plan usually is too.

Here's a quick visual on the underwriting mindset before you submit an offer:

Deals you should walk away from

Pass on deals where the numbers only work with a perfect rehab, an aggressive resale price, and no delays. Pass on houses with stacked unknowns, like foundation movement plus outdated electrical plus permit questions. Pass on sellers who want retail pricing for a property that still needs investor-level risk taken off the table.

A winning first flip usually looks ordinary. That is a good sign.

The best deals for new investors are the ones with clear comps, limited rehab complexity, and enough margin to absorb mistakes without turning a project into a loss.

Funding Your Flip The Power of Speed and Flexibility

Once you've identified a good deal, financing becomes the next filter. For non-owner-occupied flips, financing often proves a significant hurdle for many new investors. Traditional banks tend to move slowly, document heavily, and view these projects through a lens that doesn't align with the operational realities of flip projects.

Private money exists because investment deals move on seller timelines, not bank timelines.

Why first-time borrowers are underwritten conservatively

First-time flippers can still qualify for financing, but lenders usually take a more guarded position on the amount financed. According to this lending guide on first-time fix and flip requirements, private lenders typically offer 70% to 80% LTV on the purchase for first-time flippers and can fund up to 100% of construction costs for the right deal. Experienced flippers may qualify for up to 90% LTV on the purchase.

That gap makes sense. A lender is trying to protect against execution risk, not just property risk. If this is your first project, the lender wants to see that you can bring in some equity, stay liquid, and manage the plan.

Bank financing versus private money

For a flip, speed isn't a luxury. It affects whether you get the contract, whether your carry costs stay controlled, and whether your project stays on schedule.

| Feature | Traditional Bank Loan | Private Money (e.g., LendingXpress) |

|---|---|---|

| Approval style | Document-heavy, rigid guidelines | Property-focused, practical underwriting |

| Speed to close | Often slower | Built for fast closings |

| Investor flexibility | Less accommodating for first-time flippers | More flexible on non-owner-occupied deals |

| Rehab funding | Often limited or harder to structure for flips | Can include staged rehab funding |

| Use case | Better fit for long-term conventional borrowing | Better fit for short-term acquisition and renovation |

If you're comparing options for an investment property purchase, this guide on how to finance investment property is a useful place to understand the lending side more clearly.

The best loan for a flip isn't the one with the lowest headline rate. It's the one that helps you buy on time, fund the rehab properly, and exit without friction.

What rehab draws actually do

A lot of first-time investors hear “draws” and assume that means complication. In practice, draw-based construction funding creates discipline.

Instead of handing out all rehab funds on day one, the lender releases funds in stages as work gets completed. That protects the lender, but it also protects you. Contractors get paid for progress, not promises. You keep better control over the budget. If a crew goes off schedule or quality slips, you're not fully exposed.

This structure works best when your scope of work is detailed before closing. Line items should be clear. Payment milestones should match actual work in place. Ambiguity is where arguments start.

What helps a first-time borrower get to yes

New investors usually improve their approval odds when they show three things:

- A sensible purchase price: The deal has to work before financing can work.

- A believable rehab plan: Not aspirational. Believable.

- Enough liquidity for your part of the project: Even with financing, you need room to operate.

That last point matters. Private money solves speed and flexibility problems. It doesn't replace discipline. If your numbers are clean and the project is realistic, financing becomes a tool that helps you compete instead of a bottleneck that costs you the deal.

Managing Your Rehab Without Losing Your Shirt

The rehab phase is where new flippers burn through profit. Not because they picked the wrong cabinet pulls. Because they treated construction like a design project instead of a risk management project.

That distinction matters more than almost anything else in this business.

Rehab is a control problem

According to RCN Capital's fix and flip strategy guide, 35% to 50% of first-time flips fail or underperform due to timeline overruns and budget mistakes. The same source notes that a 3-week delay on an 8-week project can erode over 20% of potential profit through added holding costs alone.

That's why experienced investors obsess over scope, sequencing, and contractor accountability. They're not being picky. They're protecting margin.

Build the scope before the crew starts

A vague rehab plan invites expensive decisions in the middle of the job. You want a written scope that breaks the project into real categories, with materials, labor expectations, and completion standards spelled out.

Include items like:

- Demolition details: What's being removed, hauled away, and protected

- Core repairs: Plumbing, electrical, roof, windows, HVAC, and any safety items

- Finish package: Flooring, paint, fixtures, cabinets, counters, appliances, and exterior touches

- Punch list standards: What “complete” means before final payment

Don't leave selections open unless they need to be. Every undecided item can slow the project and create change orders.

Vet contractors like a manager, not a hopeful owner

First time fix and flippers often hire based on personality or price. That's risky.

A better process is boring and effective. Ask for references. Review prior projects. Confirm license status where required. Walk the property together and ask for a written bid that matches your scope, not their memory of the conversation.

If you need help thinking through that process, this checklist on finding the best contractor for house flipping is worth reviewing before you sign with anyone.

Field note: A cheap bid with weak supervision often becomes the most expensive line item in the whole flip.

Match payments to milestones

Good rehab management usually comes down to one simple rule. Pay for completed work, not projected work.

That means your contractor payment schedule should align with clear stages. Demo complete. Rough work complete. Cabinets installed. Final punch done. If your financing uses staged draws, even better. The funding structure reinforces job-site discipline.

Here's a practical way to stay in control:

- Walk the site often: Photos help, but they don't replace seeing the work yourself.

- Approve changes in writing: If the scope changes, the price and timeline should change in writing too.

- Keep a running budget: Don't rely on memory. Use a spreadsheet and update it constantly.

- Protect a contingency reserve: Surprises happen. Panic spending doesn't have to.

Where first projects usually drift

The common pattern is familiar. The investor starts with a modest cosmetic plan, then adds upgrades that don't improve the resale enough to justify the spend. At the same time, the contractor misses deadlines, trades overlap badly, and the property sits longer than expected.

You don't fix that by working harder at the end. You fix it by staying strict at the beginning.

A profitable rehab usually looks organized from day one. Clear scope. Tight communication. Measured upgrades. Quick decisions. That's what keeps a first project from becoming a long, expensive lesson.

Cashing Out Staging Selling and Moving On

A first-time flipper gets through rehab, sees fresh paint and clean photos, and assumes the hard part is over. Then the listing sits for three weeks, a price cut follows, and holding costs keep eating the spread.

That last stretch decides whether the deal pays you or teaches you an expensive lesson.

Sell the house the market is already buying

Buyers do not care what the project cost to finish. They compare your property to the other move-in-ready homes they can tour this weekend.

That is why staging matters. Good staging helps buyers read the room sizes, understand how the home lives, and feel that the work is complete. It also improves photos, which matters because online clicks usually happen before a showing ever gets scheduled.

Keep it practical. A basic, clean staging plan often does the job better than overspending on high-end furniture in a midrange neighborhood.

Price from current demand

The resale number has to come from fresh comps, active competition, and days-on-market in that zip code. It cannot come from your budget spreadsheet or the profit target you had at closing.

I tell new investors this all the time. The market does not reimburse hope.

If similar renovated homes are sitting, price ahead of the slowdown. If good listings are moving fast, you may have room to test the top of the range. The mistake is waiting too long to respond while interest, taxes, insurance, and utilities keep running every day the property stays unsold.

Industry tracking from ATTOM has shown that flips often take months from purchase to resale, which is exactly why exit timing deserves as much discipline as the rehab itself.

Protect your exit before the listing goes live

The best time to fix resale problems is before buyers see the property.

Use a short pre-list checklist:

- Finish the punch list: Loose handles, paint touch-ups, and missing trim signal unfinished work.

- Get strong photography: Weak photos can make a solid flip look average.

- Pull comps one more time: Pricing from 90-day-old assumptions can cost you.

- List with an agent who sells renovated inventory: Investor resale is a different job than listing an owner-occupied home with dated finishes.

Price for the market in front of you, while you still have options.

Flexibility matters here too. If buyer demand softens, or the property rents well enough to support the debt, selling is not always the only good answer. Private lending helps on the front end because it gets you into the deal fast, but the better benefit for many investors is structure. You have room to choose the right exit based on current numbers instead of forcing a sale on a bad timeline.

Your Next Steps as a Real Estate Investor

The first flip usually looks complicated from the outside. In practice, it comes down to a few habits done well.

The four habits that keep you in the game

Buy right.

A deal with enough margin forgives small mistakes. A thin deal magnifies them.

Fund smart.

Use financing that matches the speed and structure of an investment project, not owner-occupied lending logic.

Manage tightly.

Rehab profit doesn't disappear all at once. It leaks out through delays, weak scope control, and bad payment discipline.

Exit clean.

The project needs a realistic resale plan, good presentation, and a pricing strategy based on the market in front of you.

That's the roadmap for first time fix and flippers. Not flashy. Just repeatable.

A better way to think about your first deal

Your first flip doesn't need to be your biggest deal. It needs to be the one that teaches you how to evaluate risk, protect capital, and finish what you start.

That mindset changes how you choose properties, how you build a budget, and how you talk to lenders and contractors. It also keeps you from chasing deals that look exciting but don't leave enough room for reality.

If you're serious about getting into this space, talk through your deal early. A good lending conversation can tell you whether the numbers make sense, whether the funding plan is practical, and whether the project fits the kind of timeline a flip demands.

The investors who last in this business usually don't wing it. They build a process, tighten it with every project, and stay selective. That's how a first flip becomes a business instead of a one-time gamble.

If you're evaluating your first deal and want a practical read on financing, timeline, and structure, talk with LendingXpress. Their team works with real estate investors on non-owner-occupied projects and can help you understand whether your scenario is financeable before you waste time chasing the wrong property.