You found a multi-family property with the right location, clear upside, and a seller who wants certainty. The problem is the building isn't clean enough for a bank. Occupancy is soft. A few units need work. The deferred maintenance shows up fast in underwriting, and the lender that liked the deal last week now wants more time, more documentation, and more conditions.

That's where a hard money bridge loan for multi-family acquisition enters the picture. Not as a last resort, and not as a substitute for a real plan. It's a tool for a specific job. You use it when the property needs to be acquired now, improved quickly, and refinanced or sold once the business plan is executed.

The part many borrowers miss is this: the loan is never just about getting to closing. A good bridge lender underwrites the exit before they approve the entry. If the refinance doesn't make sense, or the sale path is thin, the deal is weak no matter how attractive the purchase price looks on day one.

Secure Your Next Multi-Family Deal When Banks Say No

A common scenario looks like this. An investor gets a contract on an apartment property that's underperforming for fixable reasons. Units are dated. Management has been poor. A few vacancies have dragged the numbers down. The seller won't wait for a conventional lender to work through committee, and the property doesn't present well enough to fit a bank's box anyway.

The deal still makes sense.

The buyer sees the path clearly. Clean up the common areas. Renovate the tired units. Correct lease rollover. Push occupancy back toward a stable level. Then replace the short-term debt with long-term financing that fits a stabilized building.

Why traditional lenders hesitate

Banks usually want a cleaner story at the start. They prefer stronger occupancy, fewer condition issues, and financials that already support permanent debt. If the property needs work before it qualifies, the timing gap becomes the primary obstacle.

That gap is exactly what bridge debt is designed to solve. A private lender can look at the asset, the improvement plan, and the exit path without forcing the borrower to wait for a process that wasn't built for a transitional property.

A bridge loan works best when the property is temporarily flawed, not permanently broken.

There's also a practical step many investors skip in competitive deals. Before you lock yourself into a renovation budget, get a contractor's view of the building's actual condition. This kind of early diligence matters when you're mitigating risks in property acquisition, especially on older multi-family assets where deferred maintenance can materially affect the entire loan structure.

What the borrower is really buying

Speed matters, but certainty matters more. A hard money bridge loan for multi-family acquisition gives the borrower room to act while the property is still in transition.

That usually means:

- Fast execution: You can compete against buyers who won't wait around for a bank approval cycle.

- Flexible structure: The lender can focus on the building, the scope, and the near-term plan instead of forcing the deal into permanent-loan standards on day one.

- A defined next step: The property doesn't need to stay on bridge debt forever. It needs to become refinanceable or marketable.

Used correctly, this loan doesn't just help you win the deal. It gives you a window to create the conditions for a better exit.

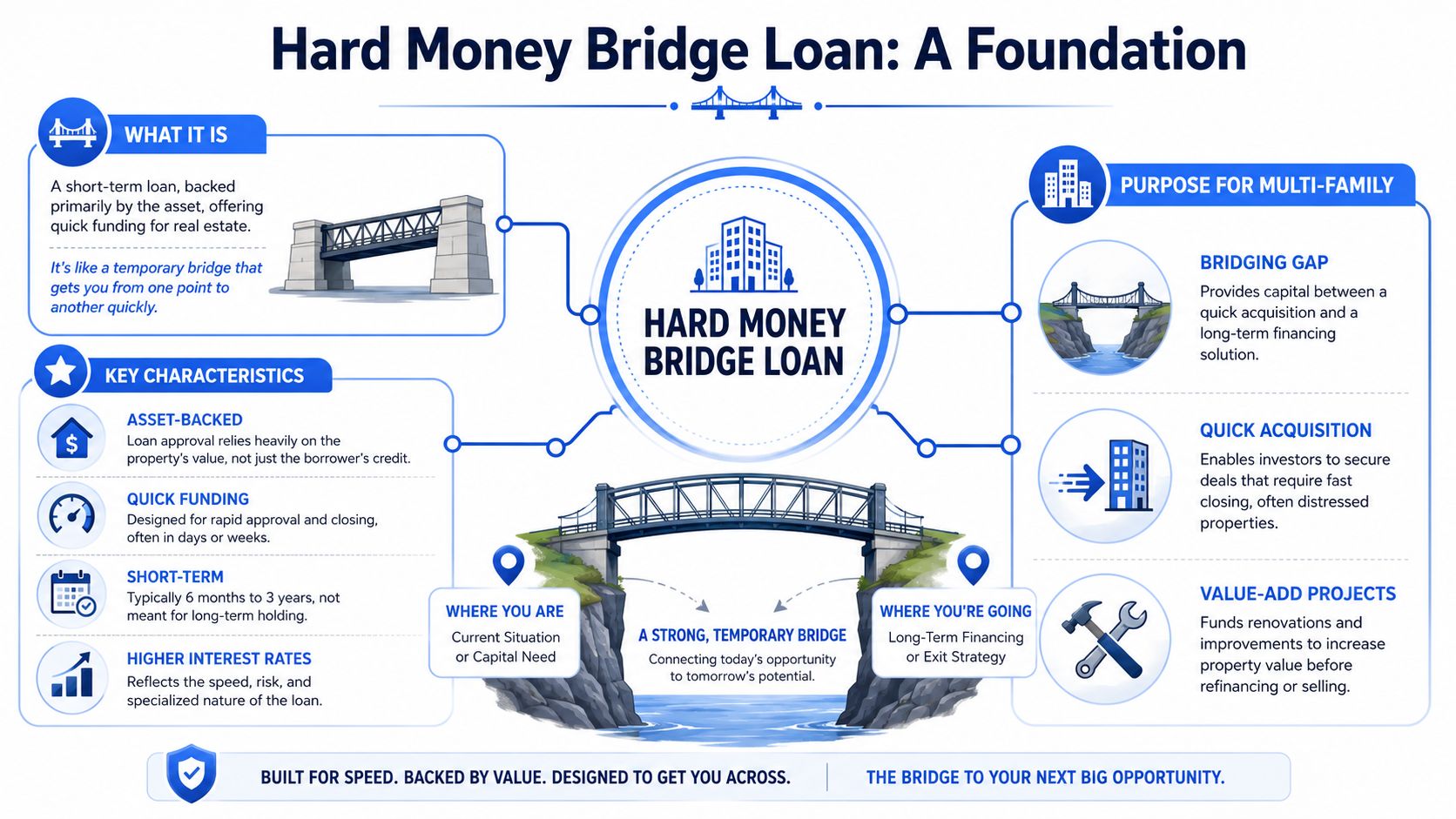

What Is a Hard Money Bridge Loan for Multi-Family

A hard money bridge loan is a short-term loan secured primarily by the property itself. Think of it as a temporary structure built to carry a property from its current condition to a stronger, financeable condition. The asset is at one point today. The business plan is intended to move it to another point soon.

For multi-family investors, that usually means acquisition first, then rehab, lease-up, stabilization, and exit.

Why it closes faster

The biggest distinction is underwriting. For multi-family acquisitions, hard money bridge loans are usually underwritten to the asset rather than borrower cash flow, which is why they can close faster than conventional debt. Industry sources describe approvals in days to 2 to 4 weeks and typical terms of 12 to 36 months, with loan sizing commonly tied to as-is value or projected stabilized value rather than permanent DSCR-only criteria, according to Avana Capital's hard money bridge loan overview.

That changes the conversation. Instead of asking only, “Does the property qualify today?” the lender is also asking, “Can this asset reach the borrower's target condition on a realistic timeline?”

How it differs from a conventional loan

A conventional multi-family loan is built for a building that already looks financeable. A hard money bridge loan is built for a building that needs time, work, or both.

Here's the practical difference:

- Conventional debt wants proven stability.

- Bridge debt can fund transition.

- Conventional underwriting leans heavily on current income and strict eligibility.

- Hard money underwriting leans heavily on collateral, sponsor experience, and the business plan.

Practical rule: If the property's current condition is the main reason a bank won't lend, you're not looking for a cheaper version of bank debt. You're looking for a loan designed for transition.

That doesn't mean bridge debt is loose or casual. Good lenders are disciplined. They evaluate risk differently. They want to know what the property is, what it can become, what work stands between those two points, and how the loan gets paid off.

Where it fits best

This type of financing tends to fit value-add acquisitions. It makes the most sense when the property needs improvements, better operations, stronger occupancy, or some combination of all three before long-term financing becomes viable.

If the building is already stable, fully occupied, and conventional-loan ready, a bridge structure may solve the wrong problem.

Typical Loan Terms and Underwriting for Multi-Family Deals

A bridge loan gets approved or declined on one question before anything else. How does this loan get paid off?

That is the center of multifamily underwriting. Rate, term, and proceeds matter, but they all sit downstream from the exit. If the lender cannot see a believable refinance or sale within the loan term, the rest of the file does not matter much.

For multifamily acquisition, hard money terms often fall in the short-term range, carry interest-only payments, and require meaningful borrower cash in the deal. One industry comparison notes common hard money ranges of 6 months to 2 years, 10% to 18%+ pricing, and roughly 50% to 75% LTV on as-is value, while multifamily bridge programs are often quoted closer to 65% to 80% LTV because they are structured around a transition to permanent debt, according to Insula Capital Group's comparison of bridge loans and hard money.

Those numbers are only the surface. The practical question is what the lender had to believe to offer them.

What lenders actually underwrite

On a multi-family bridge deal, I want four things to line up at the same time:

- The asset today: current occupancy, deferred maintenance, unit mix, collections, and any operational problems that need to be fixed

- The business plan: scope of work, budget, timeline, rent assumptions, and who is managing the turnaround

- The sponsor: liquidity, reserves, experience with similar projects, and capacity to handle delays

- The exit: refinance standards, debt-service coverage at stabilization, estimated stabilized value, and how much time the borrower really needs

The exit drives the structure. If the plan is to refinance into agency debt or bank debt, the lender underwrites toward the likely take-out requirements on day one. That means looking at future occupancy, net operating income, debt yield, debt-service coverage, seasoning, and whether the renovation plan can be finished early enough to leave room for stabilization.

A borrower may ask for maximum proceeds. A disciplined lender usually asks a different question. What loan amount still leaves enough margin for the exit to work if rents come in lower, rehab runs longer, or interest rates stay high?

Terms are set to control execution risk

Shorter terms create pressure for a reason. They force the borrower to complete the plan, stabilize the property, and start the take-out process before time runs out.

Increased equity does the same thing. More cash in the deal gives the lender a cushion, but it also gives the sponsor a reason to stay focused when the project gets harder than expected.

Extension options are another area where borrowers get tripped up. An extension is not extra free time. It usually comes with a fee, updated reserves, a current payment history requirement, and proof that the exit is still realistic. If the original business plan already needed every month in the initial term, the loan was probably too tight from the start.

For investors comparing structures, a detailed bridge loan for investment property guide proves valuable in framing the trade-offs between speed, pricing, and exit timing.

What weakens a file fast

Bridge lenders do not expect perfection. They do expect a plan that survives normal problems.

These are the issues that weaken underwriting quickly:

- Rehab budgets with no contingency

- Rent projections pulled from better properties, not true comps

- Lease-up timelines that assume every renovated unit rents immediately

- Thin post-closing liquidity

- No clear take-out lender profile

- A sale exit with no evidence of buyer demand at the projected value

This is why experienced borrowers spend time on reporting before they apply. Clear operating statements, organized leases, and current property records cut down on diligence delays and credibility questions. Teams already optimizing financial operations with AI often submit cleaner files because documents are easier to review, reconcile, and verify.

Hard Money Bridge Loan vs. Conventional Multi-Family Loan

| Feature | Hard Money Bridge Loan | Conventional Bank Loan |

|---|---|---|

| Primary use | Transitional acquisition, rehab, lease-up, stabilization | Stabilized long-term hold |

| Underwriting focus | Asset, condition, business plan, sponsor strength, exit | In-place income, property condition, borrower financials, long-term eligibility |

| Speed | Faster execution | Slower process |

| Loan term | Short-term | Longer-term financing |

| Pricing | Higher cost of capital, often with points and interest-only payments | Typically lower than bridge debt |

| Leverage approach | Often based on as-is value, rehab plan, and projected take-out feasibility | Based more heavily on current income and stabilized metrics |

| Payment structure | Often interest-only | Often amortizing |

| Best fit | Value-add or transitional asset with a clear refinance or sale plan | Stabilized property with strong occupancy |

The right way to price bridge debt is not to ask whether it costs more than bank debt. It usually does. The real test is whether the loan gives you enough time and enough flexibility to execute the plan and exit cleanly before the term becomes the problem.

How a Bridge Loan Works A Real-World Example

A bridge loan makes the most sense when the timeline matters as much as the property. Here's a simple example of how that can play out in practice.

Sarah finds a small apartment building with real upside. The location is solid, but several units need renovation, occupancy is below where it should be, and the seller wants a quick close. A bank likes the neighborhood but doesn't like the current condition and income profile, so Sarah turns to bridge financing.

The acquisition phase

Sarah presents three things to the lender: the property, the rehab plan, and the exit. The lender doesn't treat those as separate topics. They're one underwriting package.

Bridge loans allow buyers to close in days rather than months, with typical terms of 12 to 24 months and, in some markets, funding within 10 days. These loans often include interest-only payments and can be sized up to 85% loan-to-cost in some cases, according to Duckfund's overview of multifamily bridge loans.

That structure matters to Sarah because she's not buying a finished asset. She's buying time to improve one.

For investors comparing programs, a more detailed look at a bridge loan for investment property can help clarify how acquisition financing and transitional business plans are commonly paired.

The execution phase

Once the property closes, the main work begins. Sarah updates units, handles deferred maintenance, improves presentation, and works through vacancy. During this period, the interest-only structure keeps the payment focused on the short-term hold instead of forcing amortization into a property that's still being repaired and repositioned.

That's one reason bridge debt can work well on value-add multi-family. The loan is aligned with a transitional period, not a fully stabilized one.

Here's the process in a simpler visual flow.

The exit phase

Sarah's target isn't to sit on bridge debt. It's to create a refinanceable building. Once occupancy improves and the property looks stronger operationally, she applies for permanent financing. If long-term financing terms are attractive and the building now qualifies, she replaces the bridge loan and keeps the property.

If that refinance path weakens, she still needs another workable option, usually a sale.

Borrowers often spend more time negotiating rate than pressure-testing the exit. In bridge lending, that's backward.

The lesson is simple. The acquisition only works if the finish line is credible before closing day.

Planning Your Exit The Most Critical Step

Most borrowers start by asking how fast the lender can close. A smarter question is how the loan gets paid off.

That isn't a technical detail. It's the core of the file. The true execution risk of hard-money bridge loans for multifamily acquisitions is often understated. These loans are short-term, often 6 months to 3 years, and rely on an exit through refinance or sale, leaving borrowers exposed if the property does not stabilize on schedule or if capital market conditions change, according to X-Caliber's discussion of multi-family bridge loans.

What lenders are evaluating from day one

A seasoned lender doesn't wait until the end of the term to think about takeout. They underwrite the likely payoff path before issuing terms.

That review usually includes:

- Refinance readiness: Will the building qualify for permanent debt once the work is done?

- Timeline realism: Can rehab, lease-up, and stabilization happen within the loan window?

- Cash resilience: Can the borrower carry interest-only payments and absorb overruns if things move slower than planned?

- Alternate path: If the refinance stalls, is a sale still viable?

A weak exit often hides behind a strong acquisition narrative. The purchase may look attractive, but the bridge loan becomes dangerous if the property needs more time, more money, or better market conditions than the borrower assumed.

Refinance and sale are not equal in every deal

Many investors prefer a refinance because they want to keep the asset. That can be the right move, but only if the property will satisfy the standards of the permanent lender when the time comes. If occupancy, rents, condition, or market terms lag, the refinance may not be there when expected.

A sale can be the backup. But a backup only counts if the property will be marketable at a price that clears the debt and costs.

Underwriting lens: The best bridge loan files don't just show a primary exit. They show what happens if the first exit takes longer or prices worse than expected.

When bridge debt is the wrong tool

This loan is not automatically the right answer for every multi-family acquisition. If the property is already stable and qualifies for long-term financing, bridge debt can add unnecessary cost and pressure. The borrower may gain speed, but that speed can come with pricing that erodes returns if there isn't enough value creation ahead.

Bridge debt also becomes a bad fit when the business plan depends on assumptions that are hard to control. Delayed permits, contractor issues, tenant turnover, slower lease-up, and tougher refinance markets all put pressure on the exit.

The strongest deals have room for friction. The weakest ones need perfect timing.

How to Choose the Right Lending Partner

Choosing a bridge lender isn't just about rate. On a multi-family acquisition, the wrong lender can cost you the deal before closing or create trouble later by approving a structure that doesn't match the business plan.

What to look for

Start with execution history. You want a lender that understands transitional properties and can make decisions on real assets, not just on ideal files.

Look for these signs:

- Multi-family familiarity: They should understand lease-up, renovation sequencing, occupancy issues, and stabilization risk.

- Clear fee discussion: If fees, reserves, draw procedures, or extension terms are vague early, expect problems later.

- Direct answers on exit: A serious lender asks hard questions about refinance or sale from the beginning.

- Reliable process: Fast closings only matter if the lender can deliver.

Why communication matters as much as structure

In bridge lending, surprises are expensive. A lender who explains the terms plainly can save a borrower from bad assumptions about timing, rehab funds, reserves, or payoff expectations.

That's especially important for brokers and investors managing multiple moving parts at once. The lender, title company, insurance, contractor, and property management plan all need to align quickly.

One practical resource for borrowers preparing for that process is this guide on how to qualify for a hard money loan. It helps frame the kind of documentation and deal logic private lenders usually want to review.

One example in the California market

In California, LendingXpress is one lender active in this space. According to the company, it has a track record exceeding $558 million in originations, which speaks to operating history in financing income-producing properties across the state, as noted on the LendingXpress website.

That kind of track record matters less as a marketing point and more as a practical one. Experience helps when a deal has moving parts, a short fuse, or a property that doesn't fit conventional underwriting.

The best lending relationships are straightforward. The lender understands the asset. The borrower understands the exit. The structure matches the actual business plan.

If you're working on a multi-family acquisition that needs speed, flexibility, and a realistic path to refinance or sale, LendingXpress is worth a conversation. Bring the rent roll, the scope, the timeline, and the exit plan. That's what a bridge loan is built around.