You already know the situation. A rental property has appreciated, the rehab is done, tenants are in place, and the next deal is sitting there. The problem isn't opportunity. The problem is that your cash is trapped in the property.

That's where a cash out refinance on a rental property becomes useful. For investors, this isn't a consumer mortgage conversation. It's a capital access decision. The fundamental question is whether the property can support a larger loan, whether the lender will move fast enough, and whether the cash you pull out helps your portfolio more than the added debt hurts it.

Private lenders look at that problem differently than banks do. They care less about polished tax returns and more about collateral, rent coverage, equity, and execution. If you need capital for an acquisition, rehab, payoff, or portfolio repositioning, speed and asset-based underwriting often matter more than squeezing every last basis point out of a rate.

What Exactly Is a Rental Property Cash-Out Refinance

A cash-out refinance replaces your current loan with a new, larger one and returns the difference to you in cash. On a rental property, investors usually use that cash for another purchase, a renovation, reserve buildup, or to pay off more expensive short-term debt.

Think of it as converting part of your built-up equity into deployable capital without selling the asset. You still own the property. You still collect the rent. But you're pulling money out of the equity stack and putting it back to work.

Investors continue to use this strategy even when rates are not especially friendly. ICE Mortgage Technology reported that cash-out refinances accounted for 59% of all refinance transactions in Q2 2025, with many borrowers accepting higher interest rates to access cash. That tells you something important. When enough equity exists, borrowers will still refinance to access it.

What changes in the transaction

With a standard rate-and-term refinance, you replace one loan with another and mainly aim to improve terms. With cash-out, the purpose is different. You're increasing the balance to create liquidity.

Here's the practical sequence:

- The property is valued based on its current market position.

- The lender sets a maximum loan amount using its LTV cap.

- Your existing loan gets paid off through closing.

- The remaining proceeds, after costs, come back to you as cash.

Practical rule: Equity on paper isn't the same as usable equity. Lenders only let you access the portion that still leaves enough protective cushion in the deal.

Why investors use it

A rental property cash-out refinance works best when you have a clear use for the proceeds. Good uses tend to be productive and time-sensitive.

- Acquire another property: Pull equity from a stabilized asset to fund the next down payment or all-cash purchase.

- Finish improvements: Use proceeds for unit turns, deferred maintenance, or upgrades that support rent growth.

- Replace expensive debt: Refinance out of a bridge or hard money position once the property is stable.

- Strengthen reserves: Keep liquidity on hand for vacancies, repairs, or unexpected lender requests on other deals.

What doesn't work is pulling cash just because it's available. If the added debt weakens your monthly cash flow and the proceeds don't create a clear return, the refinance can become a drag instead of a growth tool.

How Lenders Underwrite Investment Property Refinances

An investor buys a tired duplex, renovates both units, raises rents, and wants capital back fast for the next deal. A conventional bank may spend weeks asking for tax returns, personal income documents, and explanations that have little to do with the property itself. Private and DSCR lenders look at the file differently. They start with the asset, the income it produces, and the amount of protective equity left after closing.

Three items drive most approvals: LTV, DSCR, and seasoning. Credit still matters, but in private lending it rarely saves a refinance that fails on asset performance or timing.

LTV decides how much equity is actually usable

Cash-out refinances on rentals are sized from the lender's risk limit, not from the investor's total equity number. A 2025 market guide noted that most lenders require borrowers to retain at least 20% equity after the refinance, and investment or multifamily lenders may stay lower, around 65% depending on risk.

That difference matters in practice. An investor may see a large spread between value and current payoff and assume all of it is available. Underwriting does not work that way. The lender starts with the maximum loan it will allow against the property, then checks whether the refinance still fits the rest of the file.

If your target proceeds push the deal past the allowed loan-to-value cap, the request gets reduced or the deal gets declined.

DSCR decides whether the rent supports the new payment

After LTV, the next question is simple. Does the property carry the new debt?

DSCR = gross rent ÷ PITIA

PITIA includes principal, interest, taxes, insurance, and association dues if the property has them. Lenders typically want DSCR in the 1.00x to 1.20x range, meaning the property's monthly rent must at least cover, and preferably exceed, the proposed monthly payment.

Many investors get surprised at this stage. A property can appraise well and still fail because the new loan payment rises faster than the rent supports. Higher proceeds mean higher debt service. If the ratio falls below the lender's floor, the file stops there.

For borrowers who do not want the deal judged primarily on personal income, it helps to review how DSCR rental property loans are structured for non-owner-occupied assets.

Plenty of equity does not fix weak cash flow. If the rent cannot support the new payment, the refinance usually does not close.

Seasoning can stop a deal before appraisal matters

Seasoning is the hold period. Many investors run into it after a fast rehab or a recent purchase.

You may have created real value in a short time, but some lenders still want to see a minimum ownership period before allowing cash out at full proceeds. The same underwriting source noted that many lenders require at least six months of ownership for cash-out on investment property, while standard conforming cash-out rules may require the existing first mortgage to be at least 12 months old. In private lending, seasoning can be more flexible, but it remains a critical screen.

Here is how that plays out on actual files:

- Fresh purchase with limited seasoning: proceeds are often restricted, even with a strong appraisal.

- Stabilized rental with documented rent: much easier to approve at better terms.

- Recently rehabbed property with no tenant in place: often better handled with bridge debt first, then a refinance after stabilization.

I tell investors to separate “improved value” from “financeable value.” Private lenders can move faster than banks, but they still want a property that is seasoned enough to support the new loan.

To round out the basics, this video gives a useful overview before you model your own file.

Short-term rentals and LLC ownership need special handling

A leased single-family rental is usually straightforward. A short-term rental or an LLC-held property needs a closer review because income treatment and entity rules vary by lender.

That changes underwriting in practical ways:

| Issue | What investors assume | What underwriting often does |

|---|---|---|

| STR income | Uses headline booking revenue | Applies an income haircut before DSCR |

| LLC title | Complicates the loan | Can work if the lender is set up for entity borrowers |

If you own short-term rentals, underwrite off adjusted income, not top-line booking revenue. If title is in an LLC, confirm early that the lender can close in entity name or explain exactly how title must be handled. Those points are easier to solve before appraisal and closing than after money has already been spent on the file.

Calculating Your Potential Cash Out A Simple Example

The cleanest way to estimate a cash out refinance on a rental property is to ignore your total equity for a moment and start with the lender's maximum allowed loan.

One common example used in rental-property guidance is a $500,000 property with a 70% LTV cap, which supports a maximum new mortgage of $350,000. That number is the ceiling. Your proceeds come from that ceiling, minus your current payoff and closing costs.

The quick formula

Use this:

Maximum new loan amount – existing mortgage payoff – closing costs = estimated net cash out

Here's the same example in a simple table:

| Item | Amount |

|---|---|

| Current property value | $500,000 |

| Lender LTV cap | 70% |

| Maximum new loan | $350,000 |

Now assume the current mortgage balance is lower than that maximum. The lender pays off the old loan first. Then closing costs come out. Whatever remains is your cash.

Why investors miscalculate this

The most common mistake is saying, “I have plenty of equity, so I should be able to pull a large amount out.” That's not how lenders size these deals.

They don't lend against all your equity. They lend up to a capped percentage of current value, and they underwrite the result.

Your usable proceeds come from the new approved loan amount, not from the total equity shown on your balance sheet.

A better way to pre-screen your own deal

Before you apply, run these checks in order:

- Estimate current value conservatively. Don't use the highest comp.

- Apply the likely LTV cap. Use a realistic lender limit, not a best-case assumption.

- Check the new payment against actual rent. If the payment rises too far, DSCR may become the problem.

- Subtract payoff and costs. That gives you a more realistic net number.

This back-of-the-napkin process won't replace a lender quote, but it will tell you quickly whether the refinance is worth pursuing or whether a different loan structure makes more sense.

The Strategic Pros and Cons for Real Estate Investors

An investor owns a rental with solid equity, but the next opportunity will not wait 45 days for a bank committee. A cash-out refinance can turn that equity into working capital fast. It can also damage a good asset if the new payment squeezes the property too hard.

That is the actual decision. More cash now versus less room for error later.

Pros

For investors using private or hard money lenders, the biggest benefit is speed tied to the asset itself. If the property has value, the rent story makes sense, and the file meets the lender's DSCR, LTV, and seasoning requirements, proceeds can often be put to work much faster than with a conventional loan.

Used well, that capital solves real portfolio problems:

- Fund the next acquisition. One stabilized rental can help finance the down payment, rehab, or closing costs on the next deal.

- Pay off short-term debt. This is common after a bridge or rehab loan, once the property is leased and ready for a longer-term structure.

- Fix underperforming assets. Proceeds can cover unit turns, deferred maintenance, lease-up costs, or other work that raises rent and value.

- Simplify the debt stack. Replacing several high-cost obligations with one refinance can make the portfolio easier to manage.

Some investors also use a cash-out refi instead of layering on a second lien. In cases where preserving the first mortgage is more important, a home equity loan for rental property may be the better fit.

Cons

The trade-off is simple. You are asking one property to carry more debt.

That affects monthly cash flow first. It also shrinks your equity cushion, which matters when repairs run over budget, a unit sits vacant longer than expected, or market rents flatten. Private lenders move faster than banks, but they still underwrite risk. If the post-refi payment leaves the deal tight, the extra liquidity is not helping much.

A cash-out refinance also resets the clock on transaction costs. New origination fees, title charges, appraisal costs, and interest expense all have to be justified by what you plan to do with the proceeds. If the money is headed into a weak project or sits unused, the refinance becomes expensive idle capital.

| Advantage | Trade-off |

|---|---|

| Pull capital out without selling | Higher payment and loan balance |

| Replace bridge or rehab debt | New closing costs and fees |

| Recycle equity into another deal | Smaller equity cushion |

| Qualify based more on the asset than personal income | DSCR pressure if rents are thin |

When it usually works

These loans work best when the rental is already performing, the borrower has enough seasoning to satisfy the lender, and the cash has a defined job. Good examples include paying off a maturing bridge loan, funding a purchase with a clear margin, or finishing improvements that support higher rents.

They work poorly when the investor is trying to pull every available dollar out of a marginal deal. Low debt service coverage, shaky tenancy, or a vague plan for the proceeds usually turns a refinance into a drag on the portfolio.

The strongest files are rarely flashy. Stable rent, a realistic debt-to-equity ratio, clean property condition, and a use of proceeds that should produce a better return than the cost of the new debt.

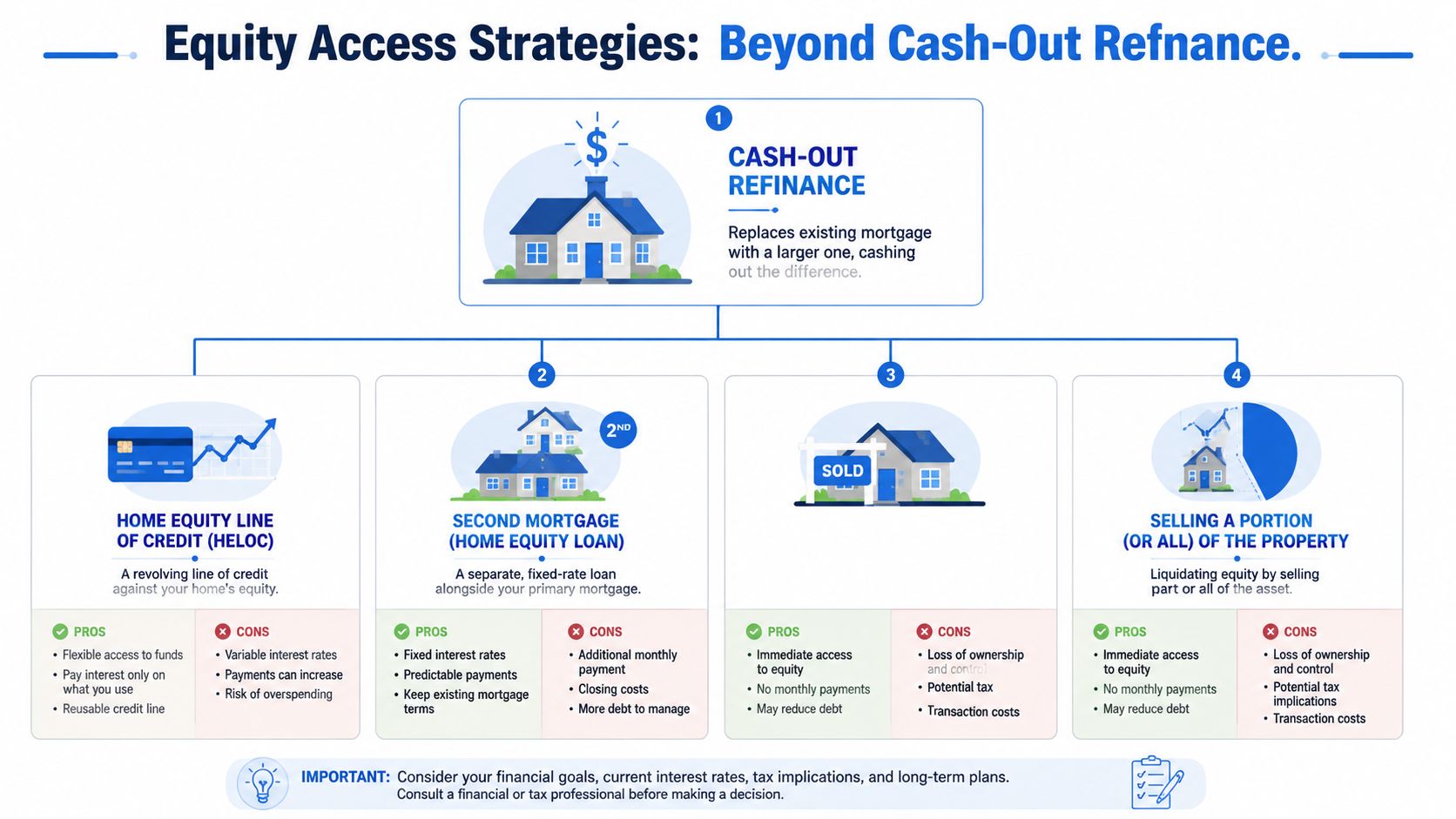

Comparing Alternatives to a Cash-Out Refinance

An investor buys a rental with short-term debt, finishes the rehab, and then hits a decision point. Replace the first lien with a cash-out refinance, add a second lien behind it, or keep the property on bridge debt a little longer. The right answer depends on timing, current loan terms, property performance, and how private lenders will size the deal.

Side-by-side comparison

| Option | Structure | Best use case | Main drawback |

|---|---|---|---|

| Cash-out refinance | Replaces current loan with a larger one | Large one-time capital need on a stabilized asset | Resets the first lien and often changes your rate |

| HELOC | Revolving line secured by equity | Repeated draws for repairs, reserves, or acquisitions | Harder to find on non-owner-occupied properties |

| Second mortgage or home equity loan | Separate loan behind the first | Keep an attractive first mortgage in place | Higher blended payment and tighter combined LTV limits |

| Portfolio or bridge loan | Asset-based short-term financing | Speed, lease-up, rehab completion, or title issues | Higher cost and shorter term |

| Sale of the asset | Full equity liquidation | Exit, 1031 planning, or redeploying capital elsewhere | You give up future cash flow and appreciation |

When a cash-out refinance is the better fit

A cash-out refinance makes sense when the property is already stable and the loan can be underwritten on rent, value, and debt coverage. For private and DSCR lenders, that usually means the asset is leased, the appraisal supports the value, seasoning is met, and the new payment still leaves enough room in the deal.

It is also the cleaner option when you need a large amount at closing instead of access to smaller draws over time. One loan can be simpler to manage than stacking a first and second, especially if the existing bridge note is maturing soon.

Some files still do better with another structure. Short-term rentals, properties held in an LLC, recent rehabs, or rentals with uneven income can get approved, but the lender may underwrite them more conservatively than the borrower expects. That can reduce proceeds or push the file out of refinance territory for now.

If you're weighing a refinance against a junior lien, compare it against a home equity loan for rental property before replacing a strong first mortgage.

When another option may be smarter

A HELOC or second mortgage works better when the existing first lien is too valuable to touch. Investors who locked in a low rate a few years ago often regret replacing it just to get cash today. In that case, paying a higher rate on a smaller second lien can be the cheaper move overall.

Bridge or portfolio debt fits transitional deals. Vacancy, unfinished renovations, lease-up, title cleanup, and recent acquisition seasoning can all make a long-term cash-out refinance premature. Private lenders will often make that short-term loan based on the collateral and exit plan, then refinance once the property is producing predictable income.

Selling is the right answer more often than investors admit. If the property no longer fits the strategy, needs too much capital, or has reached the point where equity can earn more elsewhere, forcing debt onto it is usually the weaker choice.

My rule of thumb is simple:

- Use cash-out refinance when the asset is stable, the DSCR works, and the proceeds have a clear job.

- Use a HELOC or second lien when the first mortgage is too good to replace.

- Use bridge or portfolio debt when speed matters or the property is not ready for permanent financing.

- Sell when keeping the asset creates more drag than upside.

The mistake is usually a timing mistake. Investors try to put permanent debt on a property that still needs six months of cleanup, or they stay in expensive bridge debt after the asset is already refinance-ready.

How to Choose the Right Lending Partner

The lender matters as much as the loan. Two lenders can look at the same rental property and reach very different conclusions based on how they handle DSCR, seasoning, LLC ownership, appraisals, and property condition.

For investors, the wrong partner usually creates friction in the same places. Slow responses. Moving guidelines. Last-minute overlays. A team that says it understands rental-property cash-out, then starts asking for a consumer-bank document package halfway through the file.

What to look for

Use a short checklist and be direct.

- Clear underwriting logic: Ask how they evaluate LTV, rent coverage, seasoning, and title structure before you submit a full package.

- Asset-based mindset: If the property is the deal, the lender should be comfortable focusing on collateral and income rather than building the file around personal tax returns.

- Comfort with investor scenarios: LLC ownership, non-owner-occupied assets, recent rehabs, and short-term rentals shouldn't trigger confusion.

- Speed to decision: In private lending, timing often matters as much as pricing.

- Direct communication: You want access to someone who can explain why a deal works, why it doesn't, or how to restructure it.

Questions worth asking early

A short conversation can save a wasted appraisal and a few weeks of delay.

| Ask this | Why it matters |

|---|---|

| How do you size cash-out on rental property? | Tells you whether they think like an investor lender |

| What usually kills these deals? | You'll hear quickly if DSCR, seasoning, or property type is the issue |

| Can you lend to an LLC-held property? | Avoids title surprises late in the process |

| How do you handle short-term rental income? | Critical if the rent story is nontraditional |

LendingXpress is one option in this space for California investors who need private lending on non-owner-occupied properties, including refinance and cash-out scenarios where speed and collateral-based underwriting matter.

A good lending partner doesn't just quote terms. They tell you early whether the deal is financeable, what the real constraint is, and what to change if it isn't.

If you own a rental property with trapped equity and need a realistic read on cash-out options, talk through the file before you order anything. The best first step is simple. Get the value, payoff, rent, ownership timeline, and title structure in one place, then have an experienced lender pressure-test the deal.

If you need a practical second look at a rental property cash-out scenario, LendingXpress works with real estate investors on non-owner-occupied refinance and equity-access deals. Bring the property details, current rent, payoff, and your timeline, and the team can help you determine whether a cash-out refinance, bridge loan, or another structure makes more sense.