A property hits your inbox at 8:12 a.m. It needs work, but the basis is right, the neighborhood is proven, and the seller wants speed over ceremony. If you're trying to buy a distressed house in Anaheim, a rental in Garden Grove, or a small value-add commercial asset in Costa Mesa, you already know the problem. A conventional lender may like the story, but the file can move too slowly to matter.

That gap is where a direct hard money lender fits. In Orange County, this isn't a fringe financing option for tiny deals. A regional directory reported an average hard money loan amount of $906,138 across 732 total loans in a three-month period, with Orange County among the major counties served, and listed typical pricing at 9.99% to 11.99% with a maximum loan amount of $1.5 million for standard programs in the region, which shows how often these loans support serious investment purchases rather than small side projects (Orange County hard money market data from Private Lender Link).

Your Guide to Fast Real Estate Funding in Orange County

A good Orange County deal can disappear before a bank loan officer finishes asking for updated statements. In Newport Beach, that may mean losing a clean off-market property to a buyer who can close on the seller's timeline. In Santa Ana or Anaheim, it often means missing a distressed asset because the property condition, title issue, or vacancy knocks it out of conventional lending.

Fast funding matters here because Orange County is not one market. It is a collection of submarkets with different pricing, buyer pools, and deal pressure. A light cosmetic fixer in Costa Mesa trades differently than a probate sale in Garden Grove or a small mixed-use value-add in Fullerton. The financing has to fit the asset, the seller's expectations, and the investor's exit plan.

A direct hard money lender in Orange County is built for transactions that need a quick answer and a clear structure. The review centers on the property, available equity, renovation scope if there is one, and how the loan gets paid off. That approach gives investors a practical option when the opportunity is real but the bank process does not match the timeline.

Where fast funding matters most

Certain deal types come up again and again across Orange County:

- Distressed acquisitions: Properties with deferred maintenance, vacancy, code issues, or condition problems that make bank financing difficult.

- Competitive bidding: Sellers who will take a lower or equal price in exchange for a shorter escrow and fewer financing risks.

- Bridge situations: Purchases that need short-term capital now, followed by refinance or sale after repairs, lease-up, or stabilization.

- Cash-out strategy: Existing equity pulled from one property to fund rehab costs, reserves, or the next purchase.

Speed helps, but speed alone is not enough.

The lender also needs to tell you where the file can stall, whether the rehab budget is realistic, and whether your payoff plan matches the term. In practice, that matters more than a quick verbal yes. A loan that closes fast but is poorly structured can create pressure on reserves, force an extension, or eat into the margin you expected on the deal.

Used correctly, hard money is a transaction tool. In Orange County, investors use it to secure time-sensitive opportunities, control properties that need work, and stay competitive in cities where sellers often reward certainty over a long approval process.

What Exactly Is a Direct Hard Money Lender

A direct hard money lender is the actual funding source on the deal. The same company reviewing the property, sizing the risk, and issuing the terms is also the company wiring the money at closing.

For Orange County investors, that distinction is practical, not technical. If you're trying to close on a value-add condo in Costa Mesa, a dated rental in Anaheim, or a property in Newport Beach that needs fast certainty, it matters whether your file stays with one decision-maker or gets passed from broker to lender to another lender's underwriter.

Hard money is asset-based lending

Hard money loans are private loans secured by real estate. The underwriting starts with the collateral, the equity position, the exit plan, and the condition of the property. Borrower experience and credit still matter, but they usually do not carry the same weight they would in a conventional bank file.

That changes how deals get evaluated in practice.

A bank often spends more time asking whether the borrower fits policy. A hard money lender is usually asking whether the property can support the loan and whether the borrower has a believable plan to sell, refinance, or stabilize the asset before the term runs out.

That approach is useful in Orange County because many profitable deals are not clean on day one. A house in Santa Ana may need major rehab. A small multifamily in Garden Grove may have below-market rents and deferred maintenance. A short-term bridge loan can make sense in those situations if the loan amount, timeline, and payoff strategy are aligned.

Direct means the lender controls the process

Here is the practical difference between the three common financing roles:

| Financing role | What they primarily do |

|---|---|

| Direct lender | Underwrites the deal, approves terms, and funds the loan |

| Broker | Collects the file and places it with a separate lender |

| Traditional bank | Reviews the loan through institutional guidelines and layered approval channels |

With a direct lender, fewer parties stand between the borrower and the credit decision. That usually means faster answers on valuation questions, clearer feedback on reserve requirements, and fewer surprises when escrow starts moving faster than expected.

It also makes problem-solving more straightforward. If the repair budget changes mid-transaction or title turns up an issue that affects timing, the borrower is dealing with the source of funds, not waiting for a middle layer to relay messages back and forth.

A direct lender still has to say no when the debt load is too heavy, the asset is weak, or the exit plan does not hold up. That is part of the value. Clear no's early in the process save time and protect margin.

Hard money fills a specific role. It is short-term capital built for deals where the property, timing, or business plan does not fit a conventional loan process, but the opportunity is still worth pursuing.

Why Orange County Investors Choose Direct Lenders

A Newport Beach listing hits the market on Thursday. By Friday, the seller has multiple offers and wants a short escrow with very little uncertainty. In that situation, the buyer who can get a real credit decision fast has an edge.

That is a big reason Orange County investors choose direct lenders.

In this market, speed affects price, terms, and whether you get the deal at all. A borrower competing on a dated coastal property in Costa Mesa or a light fixer in Orange often cannot wait on a bank process built around committees, layered conditions, and long appraisal timelines. Direct lending gives investors a way to act while the opportunity is still open.

Speed changes how you can bid

Fast funding is not just about closing sooner. It changes the offer itself.

An investor who knows the lender can review the file quickly can shorten financing contingencies, respond faster to seller counters, and stay credible when escrow gets compressed. That matters in Orange County submarkets where good inventory moves quickly and listing agents pay close attention to certainty of close.

Speed also has a cost. Hard money usually carries a higher rate and shorter term than bank debt. Serious investors accept that trade-off when the spread still works, the renovation plan is clear, or the property can be refinanced or sold on schedule.

Direct lenders fit the kinds of properties banks hesitate on

A large share of investor deals in Orange County are not clean, bank-ready properties. They are split-level homes in Anaheim with deferred maintenance, small multifamily assets in Santa Ana with vacancy issues, or properties in Huntington Beach that need updates before they qualify for conventional financing.

Direct lenders look at those deals through a practical lens:

- What is the property worth today?

- What needs to happen during the loan term?

- How does the borrower plan to pay off the loan?

That approach works well for value-add deals, especially where the borrower is buying below stabilized value and improving the asset. Investors comparing structures for those projects often review how ARV-based hard money lenders in California size loans around purchase price, rehab scope, and projected resale value.

Local execution matters once escrow gets real

Orange County deals rarely stay static from opening to funding. Inspections turn up old roof issues. Insurance gets more expensive on a canyon property. Tenant estoppels come in late on a mixed-use building. A seller asks for a faster release of contingencies.

Direct access to the lender helps because decisions can be made while the file is moving, not after messages pass through multiple layers. That does not mean every change gets approved. It means the borrower gets a clear answer fast enough to adjust the deal, renegotiate, or walk before more time and deposit money are at risk.

Experienced investors use direct hard money for that reason. It is not just fallback capital. In Orange County, it is often the financing choice that lets them move early, solve problems during escrow, and stay in control of the deal.

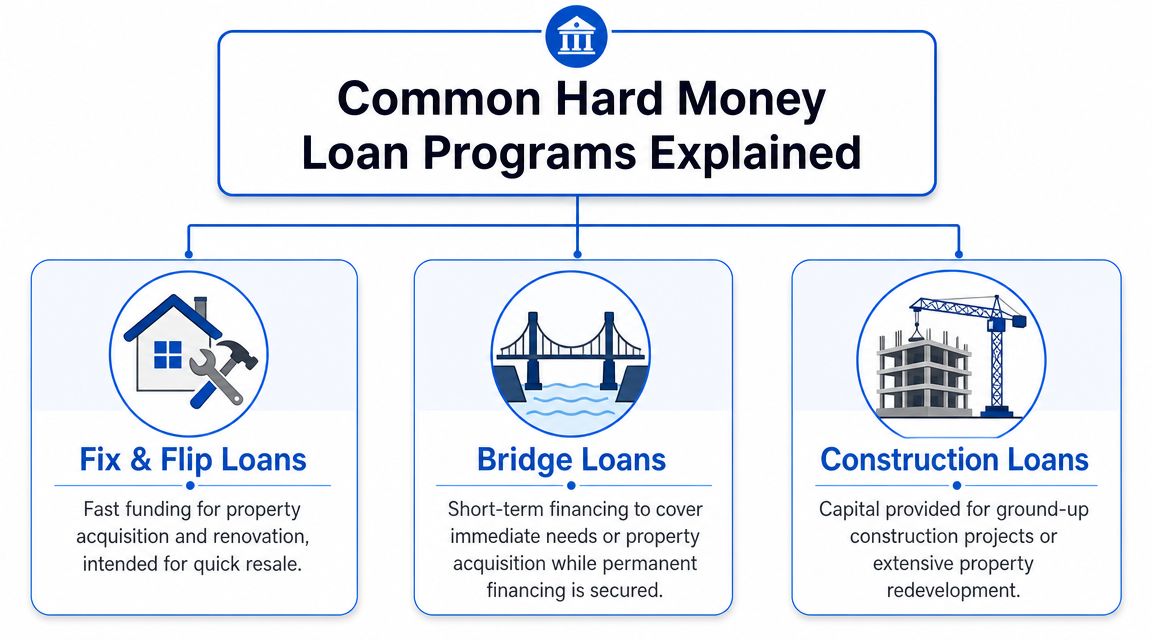

Common Hard Money Loan Programs Explained

Not every deal needs the same loan. The better approach is to match the loan to the problem you're solving.

Bridge loans

A bridge loan covers the gap between today's opportunity and tomorrow's permanent financing. This is common when an investor wants to buy quickly, stabilize the asset, and refinance once the property is in better shape.

A practical Orange County example is a borrower buying a small rental property in Newport Beach or Orange before the building is fully leased or before light renovations are complete. The property may be financeable later with long-term debt, but not today.

Bridge loans work best when the exit is clear. If the plan is vague, the short-term nature of the loan becomes a problem instead of a solution.

Fix and flip loans

This is the classic hard money use case. You acquire a property that needs work, renovate it, and sell into the market. The lender focuses on the purchase, the rehab scope, and the projected value after improvements.

For investors evaluating structure, this overview of ARV-based hard money lenders in California is useful because it frames how after-repair value affects financing options and planning.

A good fix and flip loan helps with two separate needs:

- Acquisition capital: Money to close on the property fast.

- Rehab capital: Funds for repairs, usually released through draws as work is completed.

The key mistake borrowers make is underestimating time. If your contractor slips, your carrying costs keep running.

A quick visual breakdown helps:

Rental property loans

Some investors use hard money to secure a non-owner-occupied rental quickly, then refinance into a longer-term product once the property is stabilized. This is common when the asset needs cleanup, tenant turnover, repairs, or a faster close than agency or bank debt can support.

For this strategy to work, the refinance path needs to be realistic from the beginning. If the future loan depends on major assumptions that haven't been tested, the bridge can become a trap.

The strongest rental strategy is simple. Buy right, stabilize quickly, and know your refinance target before you close the short-term loan.

Direct Lender vs Broker vs Traditional Bank

Borrowers usually compare rate first. That's understandable, but it's not enough. The better comparison is control, speed, flexibility, and how likely each option is to close your specific deal.

Financing options compared

| Criteria | Direct Hard Money Lender | Hard Money Broker | Traditional Bank |

|---|---|---|---|

| Closing speed | Usually fast because underwriting and funding sit with the same party | Depends on how quickly the broker can place the file and get lender feedback | Usually slower because of layered underwriting and formal approval process |

| Loan flexibility | Strong for distressed, transitional, or non-standard investment assets | Varies by the lender the broker ultimately finds | Best for clean, conventional properties and straightforward borrower files |

| Underwriting focus | Primarily property value, equity, and exit strategy | Depends on the actual lender behind the quote | Borrower income, documentation, credit profile, and property condition |

| Communication flow | More direct. Fewer relays between parties | More handoffs and possible delays in updates | Institutional process with less room for informal problem-solving |

| Approval odds on unusual deals | Often better when the collateral and plan are solid | Possible, but placement risk remains until a lender commits | Often lower if the property or borrower falls outside guidelines |

Where each option makes sense

A direct lender is usually the cleanest fit when the deal is time-sensitive and the asset needs common-sense underwriting. If the transaction is a bridge, rehab, cash-out, or distressed acquisition, direct access to the lender often reduces friction.

A broker can still be useful when you need broad market coverage or your scenario is unusual enough that multiple lending outlets should review it. The trade-off is less certainty early in the process. A broker can quote possible terms before a real lender fully underwrites the file.

A traditional bank is often the right answer when time isn't tight, the property is stable, and your borrower profile fits standard documentation requirements. For lower-cost long-term debt, banks still matter. They just aren't built for every investment property timeline.

The practical trade-off

Most borrowers don't lose deals because they chose the wrong spreadsheet. They lose them because they chose the wrong process.

If the seller needs certainty in days, comparing a bank quote to a direct private loan can be misleading. One option may be cheaper on paper. The other may be the only one that closes in time.

The right choice depends on the property, your exit, and the seller's clock.

How to Qualify and Understand the Terms

In Orange County, qualification usually starts with the property and the exit plan, not a stack of tax returns. If you are trying to close on a Costa Mesa value-add rental or fund a Newport Beach flip before another buyer steps in, the lender wants to know whether the asset, timeline, and payoff strategy make sense.

What the lender reviews first

Early underwriting usually comes down to four questions.

What is the property?

Type, location, condition, and whether it fits the lender's box. A clean single-family flip in Huntington Beach gets reviewed differently than a mixed-use property in Santa Ana.How much basis do you have?

Purchase price, payoff amount, cash in the deal, and the loan request all matter. A stronger equity position usually gets cleaner terms.What is the plan?

Light rehab, heavy renovation, bridge to sale, bridge to refinance, or cash-out against an existing asset. Each one carries a different risk profile.How does the lender get paid off?

Sale proceeds, refinance into long-term debt, or another defined event. A clear exit helps the file move faster.

Credit and liquidity still matter. They just are not always the first filter. A direct lender will often spend more time testing whether your numbers and timeline are realistic than whether your file looks perfect on paper.

Terms borrowers need to understand

A lot of confusion starts with shorthand. Borrowers do better when they read the term sheet like an operator, not just a rate shopper.

- LTV is loan-to-value. It compares the loan amount to the property's current value.

- ARV is after-repair value. It is the projected value after the work is done.

- Points are upfront charges paid at closing.

- Draws are rehab funds released in stages after work is completed or inspected.

- Interest reserve means some interest payments may be built into the loan proceeds instead of paid monthly from your bank account.

For a more detailed breakdown, review this guide on how to qualify for a hard money loan.

Questions to ask before signing

Rate matters, but structure decides whether the deal still works if the project slips by 30 or 60 days.

Ask these questions early, before appraisal is ordered and before legal docs are in motion:

- How are rehab draws approved and funded?

- What happens if the project runs past the original maturity date?

- Is there a minimum interest period or prepayment penalty?

- What lender fees show up outside the note rate?

- Will interest be paid monthly, accrued, or reserved at closing?

- Are taxes and insurance impounded, or do you control those payments?

Those details hit your margin fast in Orange County, where carrying costs are higher and timelines can stretch because of permits, inspections, HOA requirements, or resale pacing in a specific submarket.

One California-based option in this market is LendingXpress, which offers bridge, fix and flip, and rental property loans on non-owner-occupied assets in Orange County and other California markets. The point is that borrowers should work with a lender willing to explain the term sheet in plain language before docs go out.

A solid term sheet should tell you what the loan costs, how money is released, what triggers extra fees, and what happens if your exit takes longer than expected. If a lender cannot explain those points clearly, expect friction once escrow gets expensive.

Choosing Your Lending Partner and Avoiding Red Flags

A lender can quote fast and still create problems. The true test is whether the terms stay clear when the file gets real.

Red flags that deserve attention

One major issue is pricing opacity. A lender may advertise an attractive rate but stay vague about the actual cost of capital. Borrowers should press for the all-in picture, including points, draw fees, extension fees, and any prepayment penalties, because that's where deals often get mispriced (hard money pricing transparency considerations from West Forest Capital).

Other warning signs are easier to spot in conversation:

- Large non-refundable upfront fees: Be careful if the lender wants substantial money before meaningful underwriting begins.

- Evasive answers: If basic questions about fees, timeline, or draw process don't get direct responses, expect friction later.

- No clear process: Good lenders can explain what they need, what happens next, and what can delay closing.

- No local fluency: In Orange County, local knowledge helps. A lender should understand how different submarkets, property types, and seller expectations affect execution.

What a solid lending partner does

A reliable partner doesn't promise miracles. They underwrite conservatively, communicate early, and tell you where the deal is weak before escrow gets expensive.

The strongest conversations usually sound practical. What is the asset worth today? How much work is needed? What is the exit? What can go wrong, and how will that affect the loan?

If you're comparing options, use one simple standard. Choose the lender who makes the economics and the process understandable before you sign.

If you're evaluating a non-owner-occupied purchase, bridge, cash-out refinance, or rehab deal in Orange County, LendingXpress is one place to start the conversation. Share the property address, purchase terms, scope of work, and exit plan, and the team can help you review whether a direct private loan structure fits the deal and timeline.