A broker sends over a deal late in the afternoon. The property is non-owner-occupied, the seller wants a fast close, and the numbers work if you can move quickly. Then the critical question hits. Are you buying an asset, or are you building a business that can keep doing deals without putting your personal balance sheet in the line of fire?

That's where many investors stall. They've got a deed, a purchase contract, maybe even a rehab scope, but they haven't handled the structure. For a rental, a flip, or a bridge deal, that gap matters more than typically assumed. A real estate investors LLC isn't just paperwork. It's often the difference between a clean funding file and a messy one.

Serious investors treat each acquisition like part of an operating business. They think about liability, title, banking, insurance, and whether a lender can underwrite the entity without delay. If you're buying in one of the stronger cities for real estate investment in California, speed matters even more because the best non-owner-occupied deals rarely sit around waiting for entity cleanup.

Your Next Investment Needs a Business Plan Not Just a Deed

A lot of investors start the same way. They find a distressed rental or value-add property, run the after-repair value, and focus on getting the contract signed. That part is important, but it's only one piece of the deal.

The other piece is whether the purchase is set up to protect you and fund smoothly.

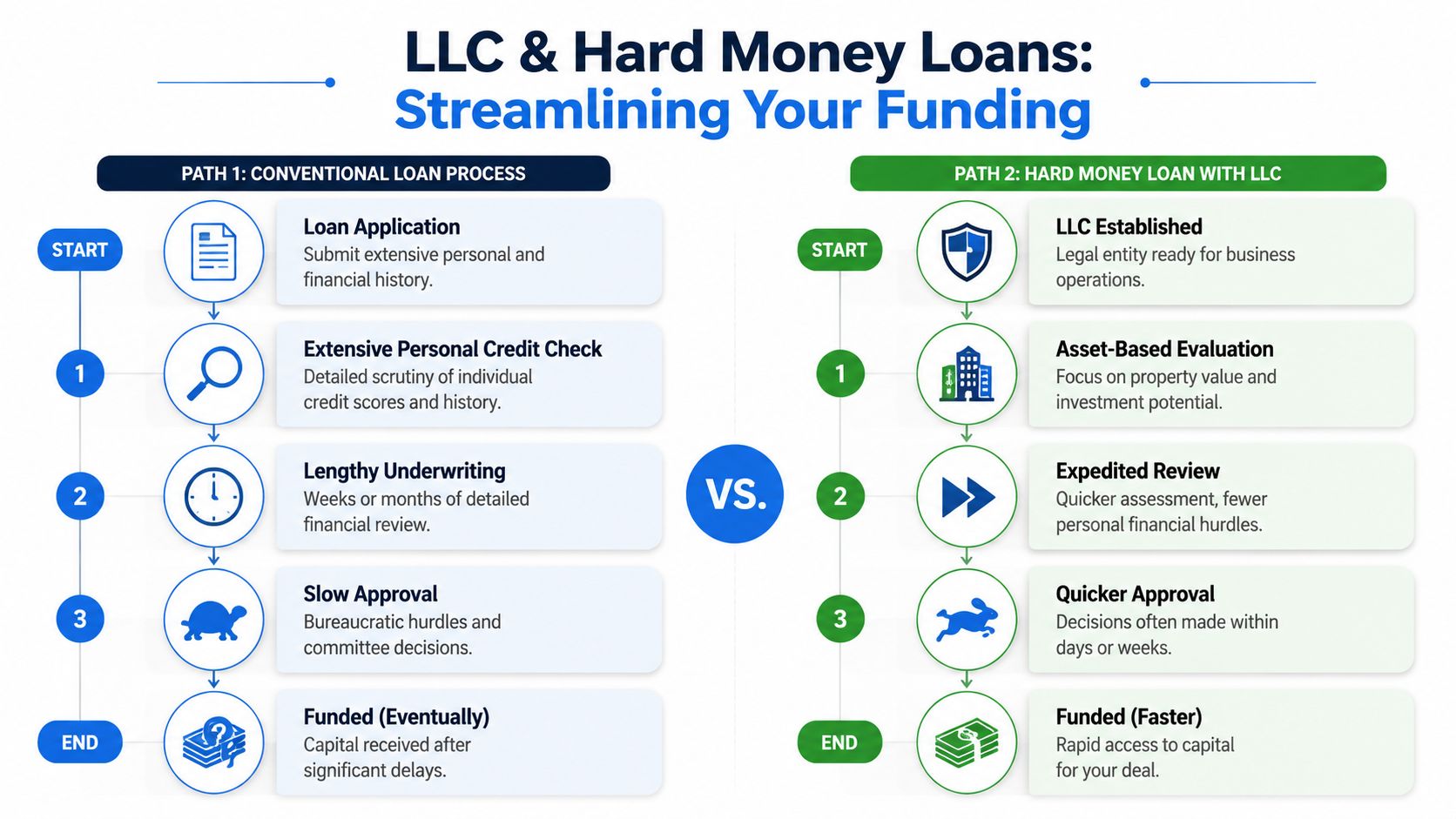

If title goes into your personal name, and the project later faces a lawsuit, contractor dispute, or debt problem, you've made the deal more personal than it needed to be. If the entity documents are weak or incomplete, the lender file can bog down at the exact moment you need speed. That's why experienced investors don't just ask, “Is this a good property?” They ask, “What's the right vehicle to own it, borrow against it, and exit cleanly?”

The shift from buyer to operator

A deed transfers ownership. It doesn't create a business system.

An LLC can. For non-owner-occupied real estate, the right LLC structure helps separate business risk from personal risk. It also gives brokers, title companies, insurance carriers, and lenders a cleaner framework to work with. That matters on bridge loans, fix and flip deals, and rental acquisitions where timing is tight and conventional financing often drags.

Practical rule: If you expect to buy more than one investment property, start acting like an operator from deal one.

What actually matters in the field

Most investors don't need a law school explanation. They need a short list of what affects the deal:

- Ownership clarity: Who owns the property, and is that entity properly formed?

- Liability separation: Can a problem at the property stay at the property?

- Financing readiness: Does the LLC have the documents a private lender will ask for?

- Operational discipline: Are the bank account, insurance, and title all aligned with the entity?

That's the primary purpose of a real estate investors LLC. It gives the deal structure, not just title.

What Is an LLC and How Does It Protect You

An LLC, or Limited Liability Company, is a legal entity that sits between you and the investment property. The simplest way to think about it is a financial firewall. You own the LLC, and the LLC owns the asset. That separation is the point.

For non-owner-occupied investments, that separation matters because rental properties and rehab projects create real exposure. Tenants can sue. Contractors can file claims. Someone can get hurt on site. A deal can default. As noted in this asset protection discussion for real estate investors, establishing an LLC for non-owner-occupied real estate investments provides legal separation between personal assets and business liabilities, and private lenders often require or strongly encourage that structure.

What the protection does

If the LLC is properly formed and properly run, claims tied to the property usually stay tied to the LLC. That means your personal home, savings, and unrelated assets have a layer of protection that doesn't exist when you buy and operate in your own name.

That protection isn't magical. It works when the entity is real in practice, not just on paper.

A judge looks at how you operated. Did you keep separate accounts? Did you sign contracts in the LLC name? Was the property deeded into the entity? Did you treat the LLC like a business, or like a nickname for yourself?

A strong LLC won't fix careless operations. It rewards clean operations.

The trade-offs investors should understand

An LLC is worth the effort for most active investors, but it's not free and it's not passive.

Here are the practical pros and cons:

- Liability separation: This is the main reason people use an LLC for investment property.

- Tax flexibility: Many LLCs use pass-through taxation, which avoids corporate-style double taxation.

- Cleaner lender file: A properly documented entity often makes underwriting more straightforward for private financing.

- More paperwork: You'll need formation documents, an operating agreement, and ongoing compliance.

- Ongoing costs: Filing fees and state requirements add overhead.

- Discipline required: If you mix personal and business funds, you weaken the shield you formed the LLC to create.

Where investors often get confused

Some people think “I formed an LLC” means the job is done. It isn't. Formation is the first move. Maintenance is what preserves protection.

If you want a deeper legal overview of state-specific planning issues, this Florida asset protection LLC guide is a useful reference. On the financing side, investors should also understand the borrowing risks tied to entity ownership, especially on short-term projects. This practical resource on ways to protect personal assets when working with flip loans is worth reviewing before your next acquisition.

Choosing the Right LLC Structure for Your Investments

Not every LLC setup fits every investor. The right structure depends on who owns the deal, how many properties you plan to hold, and how much administration you're willing to manage. For most non-owner-occupied investors, the main choice comes down to three models: single-member LLC, multi-member LLC, and Series LLC.

The simple version

A single-member LLC usually fits the solo investor.

A multi-member LLC usually fits a partnership.

A Series LLC is designed for investors who want one umbrella entity with multiple internal series, each acting as a separate liability bucket. That can work well in some states. It's less useful in places that don't recognize it.

LLC structure comparison for real estate investors

| Structure | Best For | Key Feature | California Note |

|---|---|---|---|

| Single-Member LLC | Solo investors buying one property or isolating each property | One owner, straightforward control | Common choice for single-property ownership |

| Multi-Member LLC | Partnerships, spouses investing together, joint ventures | Shared ownership and management rights | Useful when roles and profit splits need to be documented clearly |

| Series LLC | Investors with multiple properties seeking internal segregation under one master entity | Master LLC with separate cells or series | Not recognized in California, so it's less practical there for liability isolation |

Single-member LLC

This is the workhorse structure for many investors. One person owns the LLC, controls decisions, signs on behalf of the entity, and uses that LLC to own a non-owner-occupied property.

It's clean. It's familiar to lenders, title, and insurance. It also works well if you want one LLC per property, which many investors prefer for risk isolation.

Multi-member LLC

A multi-member LLC works when two or more people own the investment together. That could be a husband and wife buying rentals, two partners doing flips, or an experienced operator teaming up with a capital partner.

The advantage isn't just ownership. It's governance. A good operating agreement can define voting rights, profit splits, responsibilities, and what happens when one member wants out. Without that clarity, disputes show up at the worst time, usually mid-project or near payoff.

Before forming a multi-member LLC, decide who controls borrowing, who approves rehab draws, and who can sign closing documents.

Series LLC

The Series LLC gets attention because it offers a technical advantage for multi-property investors. It creates one master LLC with separate cells, and each cell can function as its own liability shield. In theory, that lets an investor group different properties under one umbrella while keeping risks separated.

That said, state law controls whether that structure is worth using. California does not recognize the Series LLC structure, which is why California investors often default to a separate single-property LLC model instead. In California, trying to force a Series LLC approach usually creates more confusion than savings.

What tends to work best in California

For California investors, the most practical pattern is often simple:

- One investor, one property: Single-member LLC

- Two or more owners on one deal: Multi-member LLC

- Multiple California properties with liability separation as the priority: Separate LLCs for separate assets

This isn't the lightest administrative route, but it's often the clearest. And in lending, clarity wins.

Forming Your California Real Estate LLC Step by Step

California formation isn't hard, but investors lose time when they do it out of sequence or skip documents they'll need later for funding. If your target is a non-owner-occupied rental, flip, or bridge deal, form the entity like you expect a title officer and lender to review it.

The formation sequence that keeps files clean

Choose the LLC name

Make sure the name is compliant and available in California. Keep it simple. Fancy branding doesn't matter nearly as much as consistency across formation docs, banking, insurance, and title.File the Articles of Organization

This creates the entity with the state. Until this is done, you don't have the LLC you think you have.Appoint a registered agent

This is the party designated to receive legal notices. It can be a service company or another eligible party, depending on your setup.Draft the operating agreement

Many investors treat this like a formality. That's a mistake. For lending purposes, this is one of the most important documents in the file.

The documents that matter after formation

Once the LLC exists, build the rest of the file immediately:

- Get the EIN: The LLC needs its own tax identity.

- File the Statement of Information: Don't let a fresh entity fall out of compliance.

- Open a dedicated bank account: This is essential if you want real separation.

- Handle title correctly: If the property is going into the LLC, the deed needs to reflect that.

- Pay required California fees and taxes: Staying active matters as much as getting active.

Investors often lose days, not because the loan is hard, but because the entity file is incomplete.

Why separate entities per property remain the benchmark

For investors focused on strong liability separation, forming separate single-member LLCs for separate properties remains the standard approach. The benchmark for maintaining the corporate veil is straightforward: each LLC should have its own EIN, Articles of Organization, Operating Agreement, and separate bank account.

That sounds like more work because it is. But it also gives you cleaner segregation if one property runs into trouble. For California investors, that structure is often easier to explain, easier to document, and easier to defend than a more complex workaround.

How Your LLC Impacts Getting a Hard Money Loan

A lot of investors think once the LLC exists, financing takes care of itself. It doesn't. The lender isn't just looking at the property. The lender is also looking at whether the entity is authorized to borrow, pledge collateral, and sign enforceable loan documents.

That's where deals get delayed for avoidable reasons.

The operating agreement issue most investors miss

The most overlooked document in entity-based borrowing is the operating agreement. Not because it exists, but because of what it says.

According to the National Association of Realtors, 34% of LLC-denied loans in 2024 stemmed from missing underwriting provisions in the operating agreement that explicitly allow incurring debt. For fast bridge financing, private lenders often need to see that authority clearly in the document before they can move the file forward.

If your operating agreement is silent, vague, or copied from a generic template, the lender may have to stop and ask for amendments, resolutions, or legal clarification. On a fast-moving acquisition, that can kill the timeline.

What private lenders review differently

Traditional banks often lean hard on personal income, tax returns, debt-to-income ratios, and a long financial paper trail. Private lending for non-owner-occupied real estate is usually more practical. The property, the equity, the exit plan, and the entity documents carry more weight.

A useful benchmark appears in this overview of LLCs as real estate investment vehicles, which notes that traditional banks often require a 700 to 720 credit score and DTI under 43% for non-owner-occupied rentals, while private hard money lenders may accept scores as low as 600 and can close in as little as 3 days.

That difference is why borrowers who don't fit a bank box still get deals done through private capital. But speed only works when the LLC file is clean.

Here's a short explainer worth watching before you submit your next entity-held deal:

What should be in the file before you apply

If you want a hard money file to move, prepare these early:

- Operating agreement with borrowing authority: The document should clearly allow debt financing and the signing of loan documents.

- Formation documents: Articles and state filings should match the entity name used in the purchase and title work.

- EIN and banking setup: These help show the entity is active and functional.

- Ownership clarity: The lender needs to know who the members or managers are.

- Exit plan: Sale, refinance, or stabilization should be obvious from the start.

A private lender can move fast on a property. It can't move fast through missing authority.

Where a practical lender helps

For California non-owner-occupied deals, some private lenders work comfortably with LLC borrowers and focus on asset-backed underwriting rather than bank-style friction. Investors comparing options can review California hard money loan details and see how bridge and investment financing is structured for entity-held properties. The key is less about branding and more about whether the lender understands entity documents well enough to keep the process moving.

Maintaining Your LLC to Keep Your Assets Safe

The LLC only protects you if you keep it alive as a real business. Investors lose protection when they get casual after closing. They use the wrong bank account, sign contracts personally, forget annual filings, or leave the property title inconsistent with the entity.

That's how the liability shield gets weakened.

The mistakes that cause problems

The biggest problem is commingling. If rent goes into your personal account, rehab expenses get paid on a personal card without proper bookkeeping, or the LLC pays personal bills, you've blurred the line the entity was supposed to create.

The second problem is bad paperwork discipline. If the deed never moved into the LLC, or insurance still names the wrong party, you've created a mismatch between ownership, liability, and coverage.

What disciplined investors do

Strong operators keep the entity boring. That's good. They use one bank account for that LLC. They sign as manager or member of the LLC, not as an individual unless the transaction specifically requires that capacity. They keep records, save resolutions, and respond to state compliance deadlines before they become urgent.

A short maintenance checklist looks like this:

- Keep funds separate: No personal deposits, no mixed spending, no shortcuts.

- Check title and insurance: The named insured and titled owner should match the actual ownership plan.

- Stay in good standing: File required state reports and pay required state obligations on time.

- Document major actions: Loans, manager changes, and ownership changes should be reflected in writing.

The corporate veil doesn't disappear all at once. Investors usually weaken it through a series of small habits.

Why this matters for future borrowing too

Clean maintenance doesn't just help in a lawsuit. It helps on the next loan request. A lender reviewing an entity-held rental or bridge deal wants to see an LLC that behaves like a real operating business.

That matters even more when you're using private financing because speed depends on confidence. As noted earlier in the lending benchmark for non-owner-occupied rentals, traditional banks often require stronger personal credit and lower DTI, while private hard money lenders may work with lower scores and asset-focused underwriting. If you want that flexibility, keep the entity clean enough that the lender doesn't have to wonder what's behind it.

Action Checklist for Investors and Brokers

By the time a deal is under contract, most of the outcome is already being shaped by preparation. Investors and brokers who treat the LLC as part of funding, not just part of ownership, close cleaner files.

Use this checklist before the next non-owner-occupied deal goes live.

Before you tie up the property

- Choose the ownership plan: Decide whether this deal belongs in a single-member LLC, a multi-member LLC, or its own standalone entity.

- Confirm who has authority: If there are partners, decide who can sign contracts, loan documents, and closing instructions.

- Review the deal type: A flip, bridge refinance, and rental hold don't create the same document needs or timing pressure.

During formation and loan prep

- File the entity correctly: Match the entity name across formation documents, purchase contract strategy, and title instructions.

- Draft the operating agreement for real financing: Include borrowing authority and management authority that a lender can rely on.

- Get the EIN and bank account opened: Don't wait until underwriting asks for them.

- Prepare the entity package: Keep formation docs, operating agreement, and proof of good standing in one place.

After closing

- Make sure title is correct: The deed should reflect the actual vesting plan.

- Keep finances separate from day one: Rent, deposits, rehab spending, and loan payments should flow through the LLC account.

- Align insurance with ownership: The named insured should match the entity and the property use.

- Maintain records as you go: Waiting until tax time or payoff creates avoidable gaps.

What brokers should verify before sending a file

Brokers can save a lot of time by checking four things before they submit a deal:

- Is the LLC active and in good standing?

- Does the operating agreement allow debt financing?

- Do the signer names and entity names match the contract file?

- Is the borrower asking for a structure that fits the property and exit?

If those pieces are handled early, the rest of the file usually moves with less friction.

If you're financing a non-owner-occupied purchase, bridge refinance, or rehab project through an LLC, LendingXpress is one option to consider. The firm works on California investment-property loans, including bridge and fix and flip scenarios, and focuses on fast underwriting for borrowers who need a practical path when traditional banks don't fit the deal.