You're under contract on a tired house in Los Angeles County, Orange County, or the Inland Empire. The listing says “investor special.” The seller wants proof you can close. Your agent is asking how fast your lender can move. Another buyer already came in with cash.

That's the primary problem in Southern California. It usually isn't finding a property that needs work. It's getting a lender to underwrite the deal, believe the rehab story, and move fast enough that your contract still matters by the end of the week.

For non-owner-occupied deals, traditional bank financing often breaks down at exactly the wrong moment. The property condition may be rough, the timeline is short, and the file doesn't fit a clean box. That's where Southern California fix and flip funding specialists come in. They're built for distressed assets, short holds, rehab draws, and fast closings.

The Southern California Fix and Flip Gauntlet

Southern California is unforgiving to investors who confuse a cheap rate with a workable loan. On a flip, execution beats theory. If your lender can't keep pace with escrow, contractor scheduling, and the resale timeline, the deal can go sideways even if the note rate looked good on paper.

California still offers meaningful upside, but the margin for error is tighter than many new investors think. ATTOM-backed commentary summarized here noted California's average gross profit per flip was about $100,000, while a separate Q2 2025 analysis reported a U.S. median gross profit of $65,300 and an ROI of 25.1%, the lowest since 2008. The same discussion noted a record $259,700 median purchase price in Q2 2025. That mix explains why speed matters so much. Rising acquisition costs leave less room for delays, bad bids, or sloppy draw management.

What stalls bank financing

A bank underwriter wants stability. A flip file usually looks unstable.

The property may have deferred maintenance. The borrower may be self-employed. The exit is a resale, not a long-term hold. The rehab budget may be a moving target until inspections and contractor walk-throughs are complete. None of that works well in a process built for owner-occupied homes and long amortization.

Here's what tends to kill momentum:

- Property condition issues: Missing kitchens, roof damage, or obvious deferred maintenance can push the file outside conventional guidelines.

- Time pressure in escrow: Sellers don't care that your lender needs another committee review.

- Income complexity: Investors often write off aggressively, own multiple entities, or move capital between projects.

- Project-based underwriting: A flip isn't just about borrower income. It's about purchase basis, rehab scope, and exit realism.

What a specialist actually does

A funding specialist doesn't just quote terms. A good one helps shape the file into something that can close. That means reviewing the scope of work early, spotting weak assumptions in the resale plan, and pushing title, insurance, valuation, and docs in parallel instead of one at a time.

In this market, the lender who asks sharper questions up front usually closes faster at the end.

That's the lens you want. Not “Who has the cheapest advertised rate?” but “Who can look at this exact property and tell me what will jam the file before escrow finds out first?”

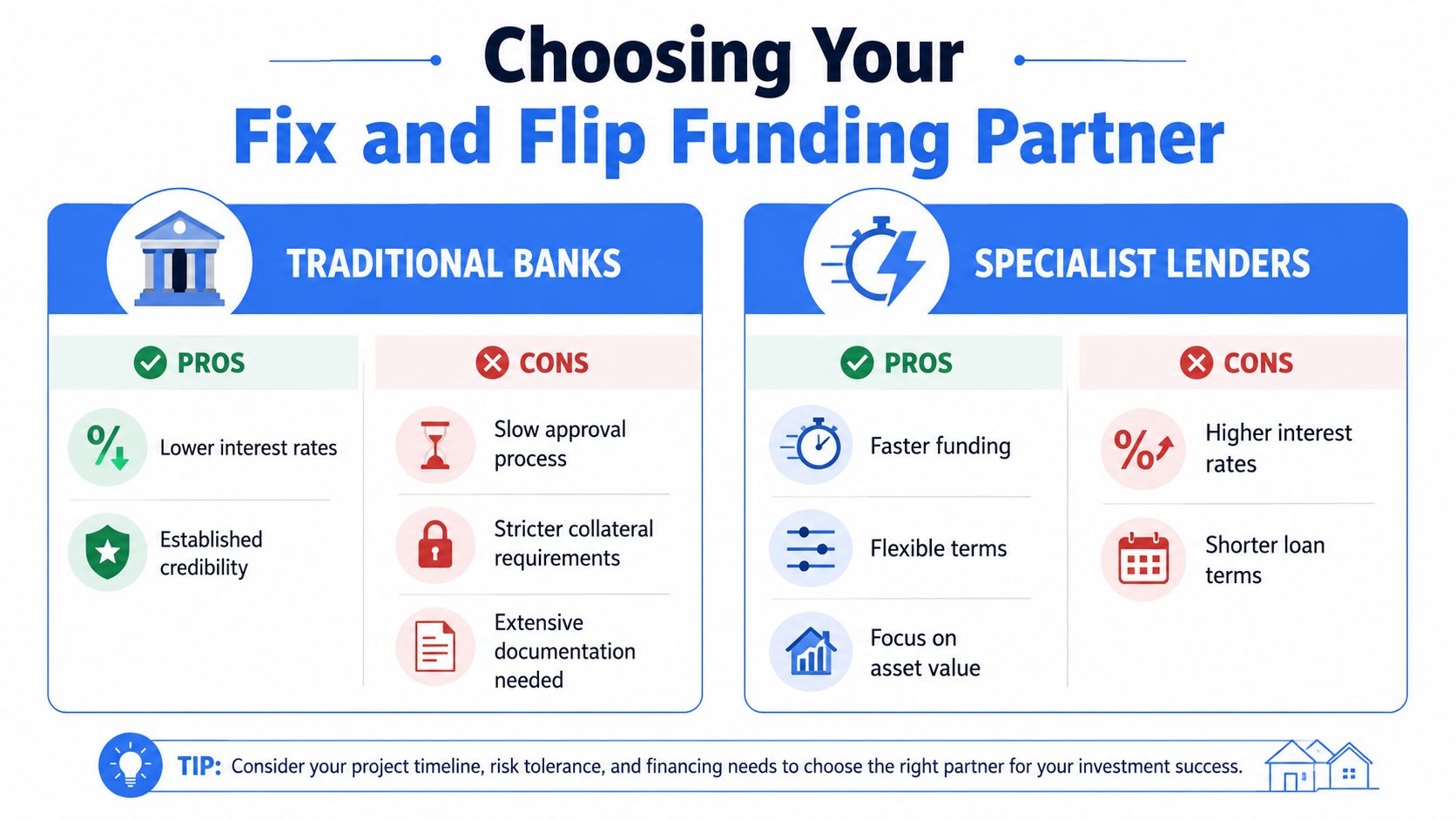

Choosing Your Fix and Flip Funding Partner

The wrong lender creates friction at every step. The right one feels organized from the first call. You can tell quickly by the questions they ask and the way they explain their draw process, valuation approach, and closing steps.

The practical difference between lender types

For flips, the main comparison isn't “good lender versus bad lender.” It's conventional process versus investor process.

| Lender type | Usually works best for | Main weakness on flips |

|---|---|---|

| Traditional bank | Clean properties, slower timelines, borrowers with simple docs | Slow approvals and less flexibility on distressed assets |

| Private lender | Unique scenarios, relationship-driven lending, faster decisions | Terms vary widely by lender and file quality |

| Hard money specialist | Distressed properties, short escrows, rehab-driven execution | Higher cost and shorter term |

Published California guidance on hard money fix and flip loans says deals commonly close in 5–14 days, terms often run 6–24 months, financing frequently covers 70%–80% of acquisition funds with 20%–30% held for rehab draws, and rates commonly range from 8%–14% with 1–3 points in origination fees, as summarized in this California fix and flip loan guide. That structure exists for one reason: investors need speed and staged rehab funding more than they need long-term amortization.

What to ask before you send a deal

A lot of borrowers ask about rate first. That's understandable, but it's not the first screening question I'd use.

Start here instead:

- How do you value the exit? Ask whether the lender relies only on current value, only on after-repair value, or some blend.

- How are rehab funds controlled? You need to know whether money is advanced in draws, what triggers an inspection, and how quickly funds are released.

- Who is coordinating escrow? If nobody owns the closing checklist, little issues become deadline problems.

- What properties make you hesitate? Their answer tells you how honest they'll be once your file gets messy.

“I'm buying a non-owner-occupied property in Southern California. It needs renovation. I need to know how you handle distressed-condition assets, what your draw process looks like, and whether you can underwrite the deal based on a realistic exit instead of a bank-style box.”

That opening script gets better answers than “What's your rate?”

What a workable partner looks like

A workable lender is transparent about trade-offs. They'll tell you when your contractor bid is light, when your ARV story is too aggressive, or when the title profile could slow the file. That's what you want.

If you're comparing active lenders in the region, this overview of Southern California hard money lenders is the type of resource worth reviewing because it reflects the investor-focused side of the market rather than owner-occupied mortgage logic.

A broker or investor should leave the first call with three things: a realistic sense of funding potential, a list of conditions that matter, and a clear picture of whether the lender can perform inside your escrow window.

How to Get Your Deal Funded Fast

Fast approvals don't come from rushing. They come from sending a clean package the first time. Underwriters don't just need documents. They need a believable story with enough support to move the file without chasing you for missing pieces.

Build the package the way an underwriter reads it

An underwriter usually wants to answer four questions.

What is the property?

Send the purchase contract, listing, photos, and any inspection information you have.What are you changing?

Your rehab budget should break work into real categories, not one-line guesses. Roof, windows, kitchen, baths, flooring, electrical, plumbing, exterior, landscaping. If the lender can't see where the money is going, they'll discount the plan.Why will the exit work?

Support the resale plan with relevant comps and a short explanation of buyer profile. Don't overtalk it. Just make it credible.Can you finish the project?

Include entity docs if applicable, liquidity evidence, experience summary, and contractor information.

The documents that carry the most weight

Some documents matter because they answer risk questions quickly.

- Purchase agreement: Shows timing, seller concessions, assignment structure, and whether your escrow is realistic.

- Scope of work: Tells the lender whether you're doing cosmetic improvement or opening every wall in the house.

- Budget and bids: These reveal whether you understand local labor and material realities.

- Exit summary: A short paragraph beats a rambling memo. State whether the plan is resale or refinance and why it makes sense.

- Borrower track record: If you've completed flips before, present them cleanly with addresses, timelines, and outcomes in simple terms.

Lender guidance summarized here notes that lenders often prefer borrowers with at least 3 successful flips for simplified documentation and better pricing. The same discussion notes California's average hard money loan size was $1,041,880 in Q2 2025, which tells you these aren't tiny hobby projects. It also notes that some programs may offer up to 90% of purchase price plus 100% rehab for qualified deals. Experience changes how much trust the lender gives your execution plan.

Here's a quick explainer worth watching if you want to think through the funding process from a borrower's side:

Questions to ask your loan officer

Questions to ask your loan officer

What would make you decline this file quickly?

Which part of my budget looks under-supported?

Are you more concerned about the purchase basis, the rehab scope, or the exit timing?

How are draws requested, reviewed, and released?

What should escrow receive from me today so closing doesn't slip?

Those questions force specificity.

What slows files down

The biggest slowdown is usually not a “bad deal.” It's a half-prepared file. Investors send a contract but no scope. Or they send a budget with no contractor support. Or they claim a strong resale value with comps that don't match size, finish level, or neighborhood.

A fast file feels complete before the lender asks for the missing page.

If you're new, don't try to sound overly complex. Be organized instead. Clean presentation beats jargon every time.

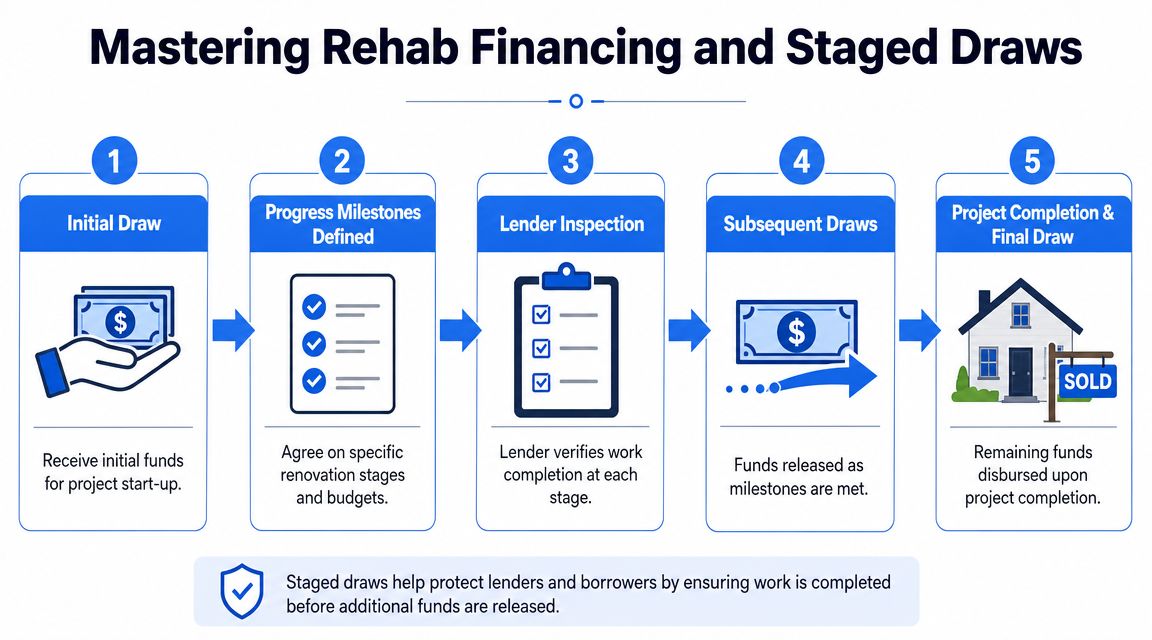

Mastering Rehab Financing and Staged Draws

Rehab money sounds simple until the first contractor invoice hits before your lender releases the next draw. That's where many first-time flippers realize the loan structure matters as much as the approval.

How staged draws work in real life

Rehab financing usually isn't handed over in one unrestricted lump sum. The lender controls the renovation budget through staged draws tied to progress.

A common sequence looks like this:

- Initial setup: The lender approves the budget and identifies draw categories.

- Work begins: Your contractor starts the first phase with the cash available at closing or your own fronted capital, depending on the structure.

- Draw request: You submit photos, invoices, and a summary of completed work.

- Inspection or verification: The lender confirms progress.

- Fund release: The next tranche is wired or sent through the approved process.

That sounds straightforward. The stress comes from timing. If your contractor expects same-day payment and your lender takes time to verify work, you need enough liquidity and planning to bridge the gap.

Align your contractor schedule with the loan

Operators separate themselves from amateurs. A contractor payment schedule should match the draw logic of the loan. If those two systems are fighting each other, your project starts bleeding time.

Use this field checklist:

- Match milestones to scope: Tie payment stages to visible completion points, not vague calendar dates.

- Get written clarity early: Everyone should know what counts as “complete” for cabinets, flooring, rough trades, and final punch.

- Keep invoice backup clean: Missing receipts and blurry photos create avoidable delays.

- Avoid front-loading too much labor: If your contractor wants a large advance with little verification, the draw process will get messy fast.

For investors who need a better handle on budget tracking, Constructo Marketing's job cost guide is a useful resource because it breaks down how to monitor project costs by phase instead of treating the rehab as one giant bucket.

Where borrowers get surprised

The surprise usually isn't that draws exist. It's that draws require discipline.

Borrowers run into trouble when they underestimate how much documentation is needed, assume every change order will be easy, or let the contractor move outside the approved scope without telling the lender. Any of those mistakes can freeze momentum.

A lender that offers investor rehab programs, including fix and flip loans with 100 rehab funding, still needs structure around inspections, milestones, and fund control. “Up to 100% rehab” doesn't mean “no process.” It means the lender may finance the renovation budget within a managed draw framework.

If your draw file is sloppy, the project starts to feel expensive long before interest becomes the main problem.

The operator's mindset

Treat your rehab budget like a live operating plan, not a one-time estimate. Update it when permits shift, when materials change, and when labor sequencing moves. Keep a version the lender understands and a version your project team uses daily. They should agree.

The borrowers who stay on schedule usually do two things well. They communicate early, and they document everything.

Your Fast-Track Closing Checklist

Once the loan is approved, the work changes. You're no longer selling the deal. You're clearing conditions and getting money to the table. This is the part that should feel mechanical.

What to confirm with escrow and title

Start with names, email addresses, and direct lines for everyone involved. Don't assume your lender, escrow officer, broker, and title contact are all aligned. Confirm that they have the same vesting information, entity documents, insurance requirements, and wiring instructions.

Use a simple closeout list:

- Entity and vesting review: Make sure the borrowing entity matches the purchase contract or approved assignment structure.

- Title conditions: Read exceptions and required payoff items early. Title surprises don't get smaller with time.

- Insurance: The policy has to match lender requirements and property use.

- Settlement figures: Review fees and cash to close before signing day, not on signing day.

Read the loan documents like an operator

Most closing friction comes from borrowers who only skim the note and deed of trust, then get upset about a fee or reserve item they could have caught earlier.

Focus on these items:

| Document item | Why it matters |

|---|---|

| Interest calculation | You need to know how payments are applied |

| Origination fees and charges | This is part of your all-in cost |

| Draw administration language | It affects your rehab cash flow |

| Extension terms | Important if the project slips |

| Prepayment language | Matters if you sell quickly |

If something doesn't match the term sheet, ask immediately. Not after documents are out for signature.

What helps files close smoothly

The smoothest closings share a pattern. The borrower replies quickly, escrow has complete contact information, and title issues are surfaced early instead of buried.

A few practical habits help:

- Answer same day when possible: Delayed replies create chain reactions.

- Send complete items: Partial uploads force your lender to re-review.

- Keep wires organized: Confirm exact amounts and timing before cutoff windows.

- Don't change entities late: Last-minute vesting changes can disrupt docs and title prep.

Clean closings come from early coordination, not last-minute hustle.

If you're brokering the loan, your fee is earned. Keep everyone focused on the last five details that fund the deal.

Red Flags That Can Derail Your Flip

Most bad flips don't fail because the investor chose the wrong interest rate. They fail because the investor ran out of time, cash, or discipline.

The biggest hidden risk is often the calendar. As summarized in this California fix and flip lending discussion, typical loan terms are often only 6–24 months, and even a modest delay tied to labor overruns or permit issues can force a costly refinance or a pressured sale that erodes equity.

The red flags lenders notice early

Some problems show up before closing. Others reveal themselves during the first week of rehab.

Watch for these:

- A budget that looks too neat: Real projects have messy line items. Thin budgets usually mean missing scope.

- An aggressive resale assumption: If the finish level, buyer pool, or comp set doesn't support the exit, the whole file is fragile.

- A contractor with no process: Good contractors document, schedule, and communicate. Poor ones improvise.

- No reserve mindset: Even strong deals need room for surprises.

- A vague backup exit: If the sale takes longer than expected, you need a second plan before the property hits the market.

Stress-test the deal before the lender does

A disciplined investor asks harder questions than the lender.

Try this internal review:

- Timeline pressure test: What happens if permits drag or a trade falls behind?

- Scope pressure test: Which line items are most likely to change after demolition starts?

- Exit pressure test: If the resale plan weakens, can you still get out without forcing the deal?

- Communication pressure test: Who approves change orders, tracks invoices, and handles lender draw requests?

The project usually breaks where the borrower assumed “that part will work itself out.”

That assumption is expensive in Southern California. Labor, permits, insurance, and buyer expectations all move fast. Your equity cushion can disappear if the schedule slips and the rehab plan loses control.

The safest borrowers aren't timid. They're realistic. They buy with a margin, borrow with a plan, and manage the project like a business instead of a side hustle.

If you need a private lending partner for a non-owner-occupied fix and flip, LendingXpress works with California investors, brokers, and agents on bridge and rehab-focused loan scenarios where speed, staged funding, and straightforward execution matter.