You find a property that works. The numbers pencil. The location is right. The seller wants certainty and a fast close because the property needs work, tenants just moved out, or a previous buyer couldn’t perform.

Then your bank says it needs more time.

That’s the moment most newer investors learn what experienced operators already know. In California, a good deal doesn’t wait for a lender’s committee, a stack of tax returns, or a slow appraisal pipeline. If you need to move on a non-owner-occupied property, speed isn’t a luxury. It’s part of the strategy.

That’s where california private money lenders come in. Used well, private money isn’t a fallback for weak deals. It’s a tool for winning properties, controlling timing, and creating options that conventional financing often can’t support.

The Investor's Dilemma Speed Wins Deals Banks Lose

A common California deal looks like this. A dated single-family home hits the market. It’s not financeable in its current condition through a typical bank program. The seller wants a short escrow because they’re done dealing with the property and don’t want repairs, extensions, or financing drama.

You submit an offer with a conventional loan, and the listing agent barely takes it seriously.

A private money offer is different. It tells the seller you understand the assignment. You’re buying an investment property, you know the property has issues, and you’re bringing financing built for that kind of deal.

Why timing changes everything

Banks usually work best when the property is clean, the borrower is easy to underwrite, and nobody is in a rush. Investors often face the opposite conditions.

A fix-and-flip deal may need fast approval, minimal back-and-forth, and a lender that’s more interested in the property than in explaining every line of your tax return. A bridge situation may involve one closing chasing another. A rental acquisition may require you to act before another buyer with cash takes it.

Speed changes who can compete. When financing is built for investors, more deals become possible.

What newer investors often miss

Private money costs more than bank money. That part is true. But that’s only half the conversation.

The actual comparison isn’t private money versus the cheapest rate on paper. It’s private money versus losing the property, missing the timing, or tying up a deal so long that the seller walks. In practice, many investors use private capital because it helps them capture an opportunity first, then improve the financing later.

That mindset matters. The strongest investors don’t ask, “Is private money cheap?” They ask, “Does it help me buy right, move fast, and exit cleanly?”

What Exactly Are California Private Money Loans

California private money loans are short-term, asset-based loans used mainly for investment property. They are built for deals that need a decision based on the asset, the numbers, and the exit, not a long review of personal income documents.

A bank usually underwrites the borrower first. A private lender usually underwrites the deal first.

That distinction matters more than newer investors realize. In practice, private money is less about replacing bank financing and more about buying time, solving a property problem, or creating a path to a better exit. Investors use it to acquire a property that needs work, close before a seller loses patience, or bridge into a refinance once the property is stabilized.

The practical difference between bank money and private money

Private lenders still review the borrower, but they put more weight on collateral, equity, renovation scope, and exit strategy. The questions are straightforward. What is the property worth today? What will it likely be worth after repairs? How much cash is in the deal? How realistic is the sale or refinance plan?

That approach is why private money can move faster. California private money lenders often quote interest rates in the 8% to 15% range and close in 3 to 10 days, while traditional bank loans often take 30 to 90 days and rely more heavily on credit and income underwriting. Private Lender Link’s California market overview also notes that private lending exceeded $1 billion in monthly volume throughout 2023 (Private Lender Link’s California market overview).

The trade-off is simple. You pay more for speed, flexibility, and a lender who can handle a property or timeline that does not fit bank guidelines.

When private money makes sense

Private money usually works best for non-owner-occupied deals where a conventional loan creates friction or delay.

- The property has condition issues: Deferred maintenance, vacancy, incomplete renovations, or title complications can push a bank to the sidelines.

- The deal has a short fuse: Estate sales, partnership disputes, expiring contracts, and failed escrows often reward the buyer who can close fast.

- The borrower’s tax returns do not tell the full story: Real estate investors often have write-offs, multiple LLCs, and uneven income that make bank underwriting slower than it should be.

- The business plan is short-term by design: A flip, a bridge between closings, or a purchase followed by a refinance usually fits private money better than 30-year debt.

For example, an investor buying a tired duplex in Los Angeles may need 10 days to close, 60 days to renovate, and six months to refinance into permanent debt. A lender focused on the asset can often handle that structure more efficiently than a bank. For deals built around short timing windows, California bridge loan financing for investment properties is often the more practical fit.

What private money is not

Private money is a tool for a specific job. It works well when speed creates profit, protects a discount, or keeps a deal alive that would otherwise die in underwriting.

It also demands discipline. Higher carrying costs can squeeze a thin project. A weak exit plan can turn a good acquisition into an expensive problem. Experienced investors know the rate matters, but the core question is whether the loan helps them control the deal, execute the plan, and exit before the cost of capital eats the margin.

That is the right way to view private money in California. It is not fallback financing for people who cannot get a bank loan. It is strategic capital for investors who know when speed is worth paying for.

Common Loan Types and Typical Terms for Investors

Investors usually reach for private money for one of three reasons. They need to close before the seller loses patience, they need a property a bank will not touch in its current condition, or they need short-term capital that matches a clear business plan.

That matters because the loan type should match the job.

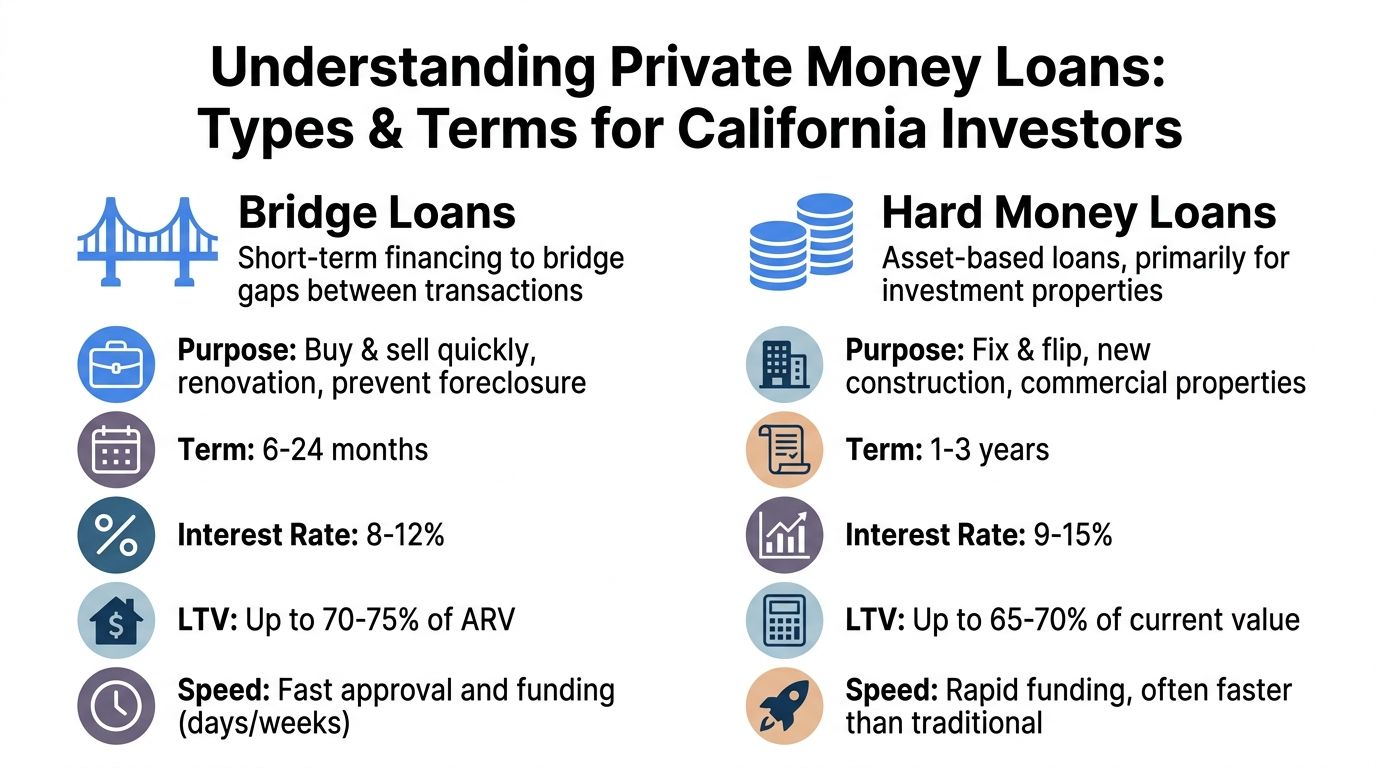

Fix and flip loans

This is the standard play for value-add investors. You buy below finished value, improve the property, then sell or refinance before the short-term debt becomes expensive.

For a flip loan, lenders usually focus on three practical questions:

Does the purchase make sense?

The basis has to leave enough room for rehab costs, carrying costs, financing costs, and profit.Is the rehab plan clear?

A real scope of work, a line-item budget, and a believable timeline make underwriting easier and draw requests smoother.How do you exit the loan?

The lender wants to know whether the property will be listed for sale, refinanced into rental debt, or held another way.

Some lenders will advance rehab funds through draws rather than hand over the full renovation budget at closing. That helps preserve your cash, but it also means your contractor schedule, inspection process, and paperwork need to stay tight. If the project is disorganized, the draw structure can slow the job down.

Bridge loans

A bridge loan is usually about timing, not heavy construction. The property may be fine. The problem is that the opportunity will not wait for conventional financing.

Common situations include:

- buying before another sale closes

- paying off a maturing loan

- acquiring a property with temporary vacancy or short-term operational issues

- closing fast in a multiple-offer situation, then refinancing after the property stabilizes

For that kind of deal, terms are often simpler than a full rehab structure. If your main issue is speed and transition rather than major renovation, a focused California bridge loan program for investment properties usually fits better than a broader fix-and-flip loan.

Rental property and stabilization loans

Private money also works well for rentals that are not ready for agency or bank debt yet. That includes properties with vacancy, unfinished turns, weak lease files, recent improvements that have not seasoned, or rents that need to be brought up to market.

Newer investors sometimes misinterpret the strategy. They look at private money as the full financing plan, when it is really the first phase. The goal is to buy control of the asset, clean up the issues, improve income, and move into cheaper long-term debt as soon as the property is ready.

Used that way, the higher rate can make sense.

Typical investor expectations

Terms vary by property, sponsor, location, and exit, but the structure usually looks like this:

| Loan type | Common use | Typical structure |

|---|---|---|

| Fix and flip | Purchase plus renovation | Asset-based, short-term, rehab funds may be released in draws |

| Bridge | Timing gap between transactions or financing events | Short-term, focused on property value, timeline, and exit |

| Rental stabilization | Acquire or season a rental before refinance | Interim financing until the property qualifies for longer-term debt |

Private money terms are often more conservative on the financing provided than bank debt, and that is part of why these lenders can move faster. They are protecting the collateral position and underwriting the exit, not trying to force a short-term investment deal into a long-term consumer loan box.

The better way to compare lenders is to look past rate alone and ask:

- How much of the purchase and rehab will they fund

- How realistic is the term for your business plan

- How are draws handled

- What fees hit at closing

- How confident are you that this lender can close on schedule

Experienced investors pay close attention to those details. A lower quote is not always the cheaper loan if weak execution costs you the deal, delays the rehab, or forces an extension.

The Application and Closing Process Simplified

Bank financing often feels like a document scavenger hunt. Private money is different. The process is still professional, but it’s usually much more direct because the lender is focused on the property, the timeline, and the exit.

That’s one reason investors like it. You can usually tell early whether the deal has a path.

What you usually need to submit

Most private lenders don’t need a giant package to start. They usually want enough information to understand the transaction and the collateral.

A typical starting file includes:

- Property details: Address, property type, current condition, occupancy, and photos if available.

- Purchase or refinance terms: Purchase contract, current payoff information, or summary of what the loan will do.

- Borrowing entity documents: LLC or corporation paperwork if you’re borrowing through an entity.

- Project plan: Rehab budget, scope of work, and timeline if improvements are part of the strategy.

- Exit summary: Sale, refinance, or stabilization plan.

If you present the file cleanly, underwriting usually moves faster. If the lender has to reconstruct the whole story from scattered emails and partial attachments, you lose the speed advantage you came for.

How the process usually moves

The mechanics are straightforward:

Initial deal review

You send the scenario. The lender decides whether the property and structure fit its box.Term sheet or quote

If the deal looks workable, you get a proposed structure with key terms.Valuation and due diligence

Depending on the asset and timeline, the lender may use an appraisal, broker opinion, internal valuation, or another property review process.Docs and closing coordination

Title, insurance, entity documents, and closing instructions get handled.Funding

Once conditions are cleared, the loan closes and funds.

A clean package beats a long explanation. Good private money files are organized, not dramatic.

Fast doesn’t mean unregulated

Some newer borrowers hear “private money” and assume it’s informal. Reputable lenders in California don’t operate that way.

For non-consumer loans, licensed California brokers are subject to disclosure requirements that help protect borrowers and investors and support enforceability of the loan documents, as explained in this review of California BRE disclosure rules for private money trust deed lending.

That matters for practical reasons. When disclosures, servicing, title work, and closing documents are handled correctly, the transaction tends to move with fewer surprises. Fast is useful. Fast and sloppy is not.

What helps a deal close smoothly

The borrowers who close fastest usually do a few things well:

- They know their numbers: Purchase price, repair cost, after-repair plan, and payoff path are clear.

- They respond quickly: Delays often come from missing documents and slow decision-making, not from the lender.

- They keep the structure simple: Complicated ownership issues, unresolved liens, or messy title questions can slow any transaction.

- They respect the short-term nature of the loan: They already know how they plan to get out before they sign.

That last point matters more than people think. Private money is forgiving about speed and flexibility. It is not forgiving about borrowers who never planned the exit.

Real-World Scenarios Where Private Money Creates Opportunity

The value of private money makes the most sense when you see it inside an actual investor decision.

A rate sheet alone won’t tell you much. The key question is whether the loan helps you take control of a property you otherwise would have missed.

The cosmetic fixer that scared off retail buyers

A small investor finds a house with an outdated kitchen, old flooring, and deferred maintenance. The property isn’t a full teardown, but it’s rough enough that many owner-occupant buyers can’t use standard financing cleanly.

That creates an opening.

The investor uses private money to buy the property, complete the rehab, and stay competitive with a short closing timeline. The lender focuses on the property and the scope of work, not on turning the file into a conventional mortgage application. Once construction starts, the project lives or dies by execution. Contractor management, budget discipline, and resale pricing matter more than anything in the loan docs.

Private money works well. It gives an investor a chance to turn complexity into equity.

The bridge loan that keeps a portfolio moving

Another investor is under contract on a small income property but hasn’t yet closed the sale of another asset. A bank sees incomplete timing and starts asking for more seasoning, more conditions, and more time.

The investor doesn’t have time.

A short-term bridge loan solves the gap. They buy the new property first, protect the acquisition, and deal with the permanent financing later. That’s often the difference between growing a portfolio and watching someone else take the deal.

If the property is right and the exit is clear, temporary debt can be the most practical path to a permanent win.

A useful explanation of this timing strategy appears in this overview of private money bridge loans and later DSCR refinancing. It notes that investors sometimes use a fast bridge loan first, then refinance into a long-term DSCR loan, and that this hybrid approach can save 2% to 4% on long-term rates while still letting them compete where speed matters.

Here’s a quick look at how that logic plays out:

| Situation | Why private money helps | What has to go right |

|---|---|---|

| Distressed purchase | Fast close on a property banks may avoid | Rehab stays on budget and on schedule |

| Timing gap between deals | Investor can buy now and refinance later | Exit financing is realistic |

| Rental stabilization | Property gets seasoned before long-term debt | Rents, occupancy, and expenses support refinance |

The rental that needs seasoning

Some properties are good long-term holds but poor candidates for immediate permanent financing. Maybe units were vacant. Maybe renovations just finished. Maybe rents need to catch up to market.

Private money can carry that asset through the transition period.

A lot of investors miss this because they think private money only belongs in flips. It can also be a tactical way to secure an asset, stabilize it, and hand it off to a more efficient loan once operations are cleaner.

A short walkthrough helps if you want to see this style of investor financing in action:

The important part isn’t just access to capital. It’s matching the capital to the phase of the project. Short-term money for short-term uncertainty. Long-term money for stabilized assets.

That’s the tactical lens experienced investors use.

How to Choose the Right Lending Partner in California

Choosing a lender in California is not a rate-shopping exercise. It is a deal execution decision.

Two lenders can quote terms that look close on paper and still perform very differently once escrow starts, title turns up an issue, or the property needs a fast valuation review. In a competitive market, the lender who can make a clear call and keep the file moving usually creates more value than the lender with the slightly lower headline rate.

Start by looking at how the lender handles real investor problems, not just how they market.

What to look for first

A solid lending partner should be able to explain the structure in plain English, point out the pressure points in your deal, and tell you early if something will create friction. That matters with California investment property because every delay has a cost. You can lose the seller, lose your window to assign contractors, or lose the refinance timeline you were counting on.

Use this checklist:

- Clear fee structure: Know the points, rate, lender fees, extension terms, draw process, and prepayment rules before you sign anything.

- Relevant asset experience: A lender who regularly funds investor deals in residential and commercial properties will usually spot issues faster and underwrite with fewer surprises.

- Fast, direct communication: If the lender is slow before issuing terms, expect more of the same once you are in escrow.

- Practical underwriting: Good lenders do not overpromise. They tell you what works, what does not, and what documents will be needed.

- Exit focus: The lender should ask how you plan to repay the loan. Sale, refinance, or stabilization. If they do not care about the exit, that is a warning sign.

Questions worth asking

A short conversation can tell you a lot about how a lender operates.

Ask these questions:

- How do you value this specific property type?

- What conditions usually delay your closings?

- How do rehab draws work in practice?

- What are the extension terms if the project runs long?

- Who owns the file from quote to funding?

For a stronger screening process, review these questions to ask when finding the right hard money lender.

Good private lenders quote quickly, underwrite clearly, and close the file they approved.

Where track record matters

Experience shows up when a deal gets messy.

California investor loans rarely move in a straight line. An LLC document is missing. Insurance needs to be rewritten. A title item appears late. The property condition is worse than the listing suggested. A lender with actual volume in non-owner-occupied lending has usually seen those issues before and knows how to work through them without creating panic at the eleventh hour.

That is one reason investors pay attention to lenders with an established history in this space. LendingXpress, for example, has funded a wide range of non-owner-occupied loan sizes and property types for California investors. The point is not the marketing claim. The point is whether the lender has enough real transaction history to make sound calls under pressure.

The practical takeaway is simple. Choose the lender that can explain the structure, set realistic expectations, and get to the closing table without drama. In California, that usually puts more money in your pocket than chasing the lowest advertised rate.

If you’re looking at a non-owner-occupied purchase, bridge loan, rehab project, or rental refinance and need a practical read on the deal, reach out to LendingXpress. A quick conversation can tell you whether private money fits the scenario, what structure makes sense, and how fast the file can move.