A deal shows up on Tuesday. The property needs work, the seller wants certainty, and the contract says close fast or lose it.

That is where most investors and brokers split into two groups. One group sends the file to a bank and watches the timeline kill the deal. The other group uses hard money lender loans the way they were meant to be used, as short-term tools for speed, flexibility, and execution on non-owner-occupied real estate.

These loans are not built for every property or every borrower. They are built for the moments when timing matters more than perfect paperwork, when the asset matters more than W-2 income, and when a clear exit matters more than a low coupon. If you are brokering or buying investment property, that difference is everything.

When Banks Say No Hard Money Says Yes

A distressed property rarely waits for a conventional underwriting queue.

A broker gets a call from an investor. The house is vacant, the roof leaks, and the seller wants a short closing because the property has already fallen out of escrow once. The investor has experience and a solid plan, but the property condition is rough and the timeline is tighter than any bank can realistically hit.

That file usually dies in conventional lending for simple reasons. The property may not qualify in its current state. The appraisal process drags. Income documentation becomes a side story that takes over the entire transaction. By the time the loan committee is ready, the seller is gone.

Hard money changes the sequence. The lender starts with the property, the investor’s plan, and the exit. That is why investors use it to win deals that do not fit a bank’s timeline or box.

In projected 2026 market data, over 40% of fix-and-flip projects are funded through private hard money channels, and the average time from application to funding has dropped 15%, enabling closings in as little as 3-7 days, compared with the weeks or months often required for bank loans, according to hard money statistics for 2026.

Why speed matters more than rate on some deals

A cheap loan that misses the contract deadline is not cheap. It is useless.

If the spread on the deal is strong, the faster lender often creates more value than the lower-rate lender. That is especially true when the seller cares about certainty, the property has deferred maintenance, or the investor needs to start rehab immediately.

Practical takeaway: On time-sensitive investment property, compare financing by total deal outcome, not just note rate. The loan that closes and funds rehab can be the lower-cost choice in real life.

What hard money solves well

- Tight closings: Purchase contracts with short deadlines.

- Property condition issues: Homes and commercial assets that conventional lenders hesitate to touch.

- Borrower profile gaps: Investors whose tax returns or debt ratios do not tell the full story.

- Execution pressure: Situations where missing the close means losing the opportunity.

For brokers, strong relationships matter. You do not need a lender who says “maybe.” You need one who can quickly tell you if the deal works, what financing amount is realistic, and what documents will move it to funding.

Hard Money vs Conventional Loans The Key Differences

A broker sees this every week. The borrower has a good deal, a seller wants certainty, and the property needs work before it fits a bank’s standards. The question is not which loan is better in the abstract. The question is which loan fits the job in front of you.

Hard money and bank financing solve different problems. One is built around the asset, the business plan, and the exit. The other is built around borrower documentation, income stability, and guideline compliance. That difference changes how you size the loan, package the file, and set expectations with the client.

How the two loan types function in practice

| Feature | Hard Money Loan (LendingXpress) | Conventional Bank Loan |

|---|---|---|

| Primary underwriting lens | Property value, deal structure, and exit plan | Income, credit, debt ratios, reserves, and full documentation |

| Timeline | Short-term investment execution | Longer-term financing for stabilized scenarios |

| Property condition tolerance | Can work for distressed, outdated, or transitional assets | Usually prefers properties in financeable condition |

| Rehab proceeds | Often structured into the loan through draws | Commonly limited, separate, or unavailable |

| Deal flexibility | Terms shaped around the project and timeline | Terms shaped around bank policy |

| Best fit | Non-owner-occupied investment deals with a clear value-add plan | Borrowers and properties that already fit agency or bank standards |

The real underwriting difference

With hard money, the lender starts by asking whether the property and exit support the request.

That shifts the conversation. Instead of spending most of the file trying to prove salaried income or explain tax return write-offs, the focus stays on purchase price, current value, rehab scope, projected value, marketability, and payoff strategy. Borrower quality still matters. Experience, liquidity, and credit profile help the file. But the deal itself has to carry weight.

Conventional lenders approach the file from the opposite direction. They want a borrower who fits policy and a property that creates few surprises. That works well for stabilized rentals, owner-occupied homes, and refinances where time is available and the property already checks every box.

Where brokers lose deals

The mistake is usually a fit problem.

A short-term value-add project gets submitted to a bank that wants a finished property. Or a clean long-term hold gets pushed into expensive short-term debt when permanent financing was available all along. Good brokers save clients money by matching the loan to the stage of the project, not by forcing every deal into one channel.

If you need a clearer view of how private lending products are structured, this guide to different types of private money lenders and loan use cases is a good reference point.

What tends to get approved faster

Hard money files move well when the package answers the lender’s practical questions early:

- What is the borrower buying, and at what basis?

- What work is being done, and what does it cost?

- What supports the projected value?

- How does the borrower plan to exit the loan?

- Does the asset support the requested proceeds?

Files slow down when those answers are vague.

Common problems include inflated ARV, thin rehab budgets, no reserve plan, weak comps, and an exit that depends on perfect market conditions. Short-term capital can solve a lot of problems, but it does not fix a thin deal.

Broker tip: When you present hard money lender loans, emphasize speed, asset-based underwriting, rehab execution, and fit for non-owner-occupied investment property. That framing is more accurate and it attracts the right borrower.

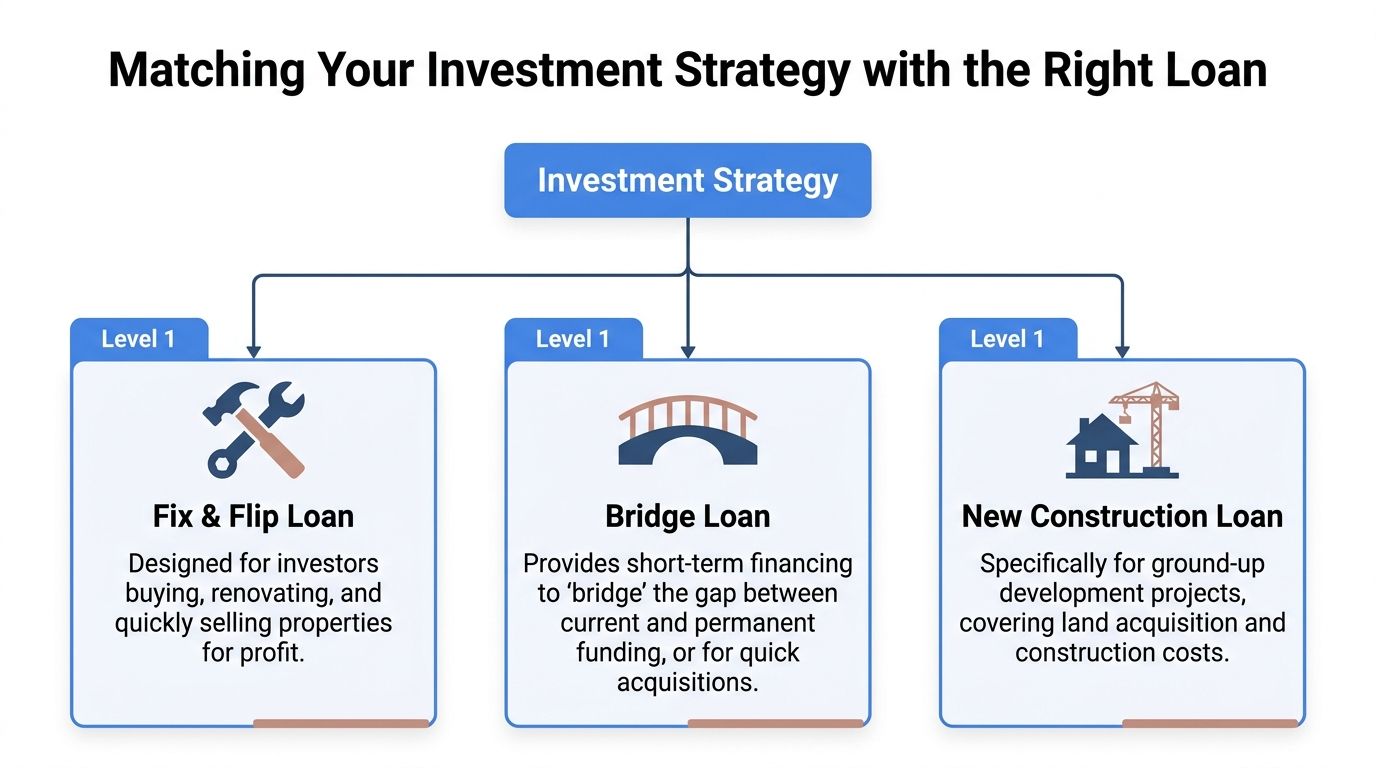

Matching the Right Loan to Your Investment Strategy

Hard money is not one product. It is a category of tools.

Investors get into trouble when they use the right loan at the wrong time. A fix and flip file should not be structured like a bridge deal. A property that needs seasoning before long-term debt should not be pushed into permanent financing too early.

Private lending became important in real estate during periods when banks tightened credit. Hard money lending gained prominence during the Great Depression and the Savings and Loan Crisis because private lenders kept funding deals with asset-based, flexible structures when conventional institutions pulled back, as described in this review of the history and resilience of hard money lending.

Fix and flip loan

This is the tool for a property you plan to buy, improve, and resell.

The key is that the renovation plan has to be tight. Scope of work, timeline, contractor alignment, and resale logic all matter. If the business plan depends on vague upgrades or an inflated sale price, the loan turns from useful to dangerous.

A strong fix and flip scenario usually includes:

- A below-market purchase: The investor is buying enough margin, not hoping to create it later.

- A documented rehab plan: Line items, contractor bids, and draw expectations are clear.

- A realistic resale path: The property has obvious marketability after repairs.

Some lenders structure these loans with staged rehab disbursements, which helps control project risk and keeps capital tied to progress instead of promises.

Bridge loan

A bridge loan solves a timing gap.

That gap might be between purchase and refinance, between one sale and the next acquisition, or between current equity and an urgent business need tied to real estate. This is often the right move when the asset is solid but the borrower cannot wait for a slower lender.

Bridge financing works well when the investor knows exactly what event pays off the loan. Sale, refinance, lease-up, or recapitalization. One of those needs to be the plan from day one.

Rental loan

Some projects are not flips. They are reposition-and-hold deals.

An investor buys an underperforming rental, stabilizes it, improves operations, and then moves into a longer-term loan once the property and financials are ready. In that scenario, short-term private money can be the first step, not the finish line.

The best rental strategy is disciplined. Improve the asset, document the work, support rents, then refinance out of the short-term debt on schedule.

New construction and more specialized structures

Some investors need ground-up construction rather than a rehab or short bridge. In those cases, the loan structure, draw administration, and project monitoring become more detailed. For a broader overview of private lending structures, this breakdown of different types of private money lenders is a useful reference.

One practical note. The right product is the one that matches the actual business plan, not the one that looks cheapest on the term sheet.

Understanding Hard Money Rates Terms and Rehab Funds

A lot of deals look good until the loan terms hit the desk.

The investor sees spread. The lender sees risk, timing, and whether the exit is realistic. If you want to know whether a hard money file can close, focus on three things first: ARV, LTV, and rehab draw structure. Those are the terms that decide how much money is available, how much cash the borrower needs to bring in, and how tight the execution window will be.

Start with ARV and not emotion

ARV means After Repair Value. It is the lender’s estimate of what the property should be worth once the work is done.

That number drives the whole structure. If the purchase price, rehab budget, and closing costs push the request too high relative to the finished value, the deal gets tighter fast. The borrower may need more cash down, a smaller scope of work, or a lower purchase price. Sometimes the right answer is to pass.

New investors usually miss one point here. ARV is not based on hope or on the highest comp in the neighborhood. It has to be supported by condition, layout, location, and a scope of work that matches the resale target.

What terms usually look like

Hard money is short-term capital. The pricing reflects speed, flexibility, and the fact that the lender is often stepping into deals banks will not touch.

Terms often include interest-only payments, points charged at closing, and a balloon payment at maturity. That structure works well for a flip, a bridge, or a fast repositioning play. It creates pressure if the timeline slips. Every extra month adds carrying cost, and a weak exit plan can turn a profitable deal into a thin one.

I tell brokers to underwrite the delay, not just the ideal timeline. If the rehab takes longer, permits stall, or the sale drags, the deal still needs room to survive.

A practical fix and flip example

Here is the simple screen I would use on an early call.

An investor contracts a property at $200,000 and projects a $300,000 after-repair value. If the lender is comfortable with the ARV and budget, the loan may cover a large part of the purchase and some or all of the rehab, but only if the total exposure fits the lender’s guidelines.

This is the true test. If the project only works with an aggressive value, a thin reserve position, and a perfect resale timeline, it is not a strong hard money deal. It is a fragile one.

How rehab draws work in the field

Rehab money is often released in stages instead of being wired in full at closing.

That protects the lender from unfinished work and cost overruns. It also forces discipline on the project. The borrower completes a phase, documents it, requests a draw, and then moves to the next phase. On a well-run project, that process keeps contractors, budget, and timeline aligned.

If you want a clearer picture of staged funding, this guide on using rehab loans to fund real estate investment projects explains how draw-based financing fits into actual execution.

A short explainer helps if you are new to draw-based financing:

Where borrowers usually miscalculate

Borrowers rarely lose control of a project because they forgot the note rate. The bigger misses are operational:

- ARV was overstated

- Scope of work missed real repair costs

- Timeline ignored permit, labor, or inspection delays

- Exit strategy depended on a best-case market

LendingXpress structures bridge, fix and flip, and rental loans for non-owner-occupied property with asset-based underwriting, staged rehab funding, and closings in as little as three days when the file is ready. On the right deal, rehab proceeds can cover up to 100% of renovation costs. The key phrase is on the right deal. The property, budget, and exit still have to make sense.

Your Checklist for a Fast and Smooth Closing

Fast closings are rarely won by rushing. They are won by preparing the file before underwriting asks for the obvious.

If you want hard money lender loans to move quickly, give the lender a package that answers the first round of questions up front. That cuts friction, reduces back-and-forth, and keeps title and escrow from waiting on missing items.

Investor checklist

- Purchase contract: Signed and complete, including addenda and the actual close date.

- Entity documents: LLC or corporate formation documents, operating agreement if applicable, and signer information.

- Property details: Address, current condition, rent roll if occupied, and any known title issues.

- Scope of work: A line-item rehab budget, contractor bids, and a realistic completion timeline.

- Exit strategy: Sale, refinance, or lease-up plan stated clearly and supported by the property story.

- Liquidity support: Proof of funds for down payment, reserves, closing costs, or carry.

Broker checklist

A good broker package saves everyone time.

- Lead with the summary: Loan purpose, purchase price or payoff, estimated value, requested loan-to-value, and exit.

- Explain the business plan: Distressed flip, bridge refinance, cash-out for business purpose, or stabilization play.

- Pre-clear weak spots: If the borrower has credit events, title complexity, or experience gaps, explain them before underwriting flags them.

- Organize the file: Put contracts, budget, entity docs, and property photos in one clean package.

- Set timeline expectations: Confirm escrow deadlines, inspection milestones, and any seller pressure points.

Match the paperwork to the loan structure

Hard money loans are typically short-term. Verified guidance notes that they commonly run for periods from several months to a few years, often with interest-only payments and a balloon payoff, with pricing that includes a higher interest rate and origination points compared to conventional loans. That structure works well for quick-turn investment projects, but only when the borrower has a real exit and understands how delays increase cost.

Closing tip: The smoothest files have a documented scope, a believable timeline, and an exit that does not depend on luck.

If you are the borrower, think like an underwriter. If you are the broker, think like a deal manager. That shift alone speeds up approvals.

Two Investors One Goal Success with LendingXpress

The best way to understand hard money is to watch how investors use it.

The fix and flip investor

An investor tied up a dated property that needed more than cosmetic work. The opportunity was strong because the house had margin, but the file was weak for a bank. Condition issues, a short escrow, and a renovation-heavy plan made conventional financing a poor fit.

The solution was a short-term asset-based loan with rehab funds controlled through draws. That let the investor acquire the property quickly, renovate in phases, and avoid draining all available cash on day one.

What worked was not magic. The purchase made sense, the scope was detailed, and the resale plan was grounded in the actual neighborhood. The investor treated the loan as a tool, not as permission to overspend.

The commercial owner with a timing problem

A business owner had equity in a commercial asset and needed to move fast on a separate opportunity tied to operations. A slower refinance would have missed the window.

A bridge structure solved the timing gap. The borrower used existing real estate as collateral, accessed capital quickly, and bought time to execute the next step without waiting on a long approval cycle.

The difference maker was a defined payoff path. This was not open-ended debt. The owner knew how the bridge would be cleared and how long the capital needed to stay in place.

The shared lesson

Both investors had the same goal. They needed capital that matched the actual problem.

What failed in similar situations was usually one of three things:

- No realistic exit

- Overestimated value after improvements

- Using short-term debt for a project with no urgency discipline

What helped was conservative financing, a first-position lien, and a borrower who understood that speed is useful only when the plan is tighter than the timeline. That is where a relationship-based lender becomes valuable. Not because the lender removes risk, but because the lender structures around it.

Your Hard Money Loan Questions Answered

Is recourse a big deal

Yes.

A key question in hard money is whether the loan is recourse or non-recourse. A recourse loan allows the lender to pursue your personal assets if the property sale does not cover the debt. A non-recourse loan generally limits recovery to the collateral property itself. That distinction matters because it affects your personal exposure if the project goes badly, as explained in this article on questions to ask about recourse in hard money lending.

How do you spot a lender worth using

Start with transparency.

Ask how the lender underwrites ARV, how draws are released, who makes the credit decision, what fees show up outside the quoted rate and points, and what happens if the project needs more time. You want direct answers, not vague reassurance.

Also ask about licensing, documentation standards, and whether the lender has a clear process for title, escrow, and closing coordination. A clean process usually signals a serious operation.

If you are structuring a non-owner-occupied purchase, bridge refinance, or rehab-heavy investment deal and need a practical second opinion, LendingXpress is one place to review deal fit, timeline, and loan options before a contract window closes.