You've got a deal in front of you. The broker says it's “priced to move,” the seller wants a quick close, and your gut says there's upside. The problem is simple. You don't have time to build a full model before deciding whether the property deserves another hour of your attention.

That's where cap rate earns its keep.

If you want to know how to calculate cap rate the right way, start with one rule. Use it as a fast filter, not a magic answer. On clean, stabilized rentals, the math is straightforward. On the kinds of properties private lenders often see, half-vacant buildings, dated units, deferred maintenance, light repositioning, the key work is deciding which income number and which value number belong in the formula.

Why Cap Rate Is Your First Look at a Good Deal

Cap rate is the first number I want to see because it cuts through noise. Before you get lost in loan terms, rehab budgets, and resale dreams, cap rate tells you whether the property's income justifies the price. It's a fast screen. That matters when you're competing against buyers who can move quickly.

For investors, speed matters almost as much as accuracy. A slow “perfect” analysis on a dead deal is wasted effort. A quick, disciplined cap rate review helps you decide whether to pass, renegotiate, or dig deeper.

What cap rate does well

Cap rate is useful when you need to answer a basic question fast: What does this property earn relative to what it costs? It strips out the financing piece so you can judge the asset itself.

That's why investors use it to compare one property against another, even when the loan structures will be different.

Practical rule: If you can't explain the property's cap rate in one minute, you probably don't understand the deal yet.

Where investors get sloppy

Most online explanations stop at the textbook formula. That's fine for a fully leased building with stable expenses. It breaks down when the property is in transition.

A vacant unit, below-market rents, bad management, or a rehab plan can make one cap rate look cheap or expensive for the wrong reason. If you're buying distressed rentals, mixed-use properties, or fix-and-flip inventory with an income angle, you need more than a formula on a napkin.

Here's how it works in practice:

- Use cap rate first to screen pricing.

- Check NOI hard because bad expense assumptions ruin the result.

- Separate current performance from projected performance when the deal isn't stabilized.

- Don't compare unlike properties just because the percentages look close.

That discipline keeps you from chasing “great deals” that only work in a spreadsheet fantasy.

The Cap Rate Formula Demystified

The standard formula is simple: Cap Rate = (NOI / Market Value) × 100. That's the industry-standard equation cited by Investopedia in the verified guidance above.

What the formula is really telling you

The numerator is Net Operating Income, or NOI. That's the property's income after operating expenses. It does not include mortgage payments or income taxes. The denominator is the property's current market value or purchase price.

That's why cap rate is often treated as an unlevered yield. It lets you compare the asset without letting financing muddy the picture.

If you want a deeper primer on valuation logic beyond cap rate alone, this guide to expert real estate valuation is a useful companion read.

A clean example

The verified data gives a straightforward example: if a property produces $120,000 in annual NOI and its market value is $1,200,000, the cap rate is 10% because $120,000 / $1,200,000 = 0.10, or 10%.

That's the cleanest version of how to calculate cap rate.

| Piece | Amount |

|---|---|

| Net Operating Income | $120,000 |

| Market Value | $1,200,000 |

| Cap Rate | 10% |

Why investors like this metric

The appeal is obvious. You can compare two deals without mixing in down payment size, rate, amortization, or whether one buyer is all cash and the other is using significant debt.

It also helps explain price movement. The verified data notes that if a market trades at an average 6% cap rate, a property with $60,000 in NOI would be valued at about $1,000,000 using the income approach. Same logic, reversed. When cap rates compress, values rise if NOI holds steady.

Cap rate is a pricing language. Sellers, brokers, appraisers, and lenders all use it because it converts income into a shorthand for value.

That said, the formula only works as well as the NOI you feed into it. That's where most mistakes start.

Calculating Net Operating Income The Right Way

If your NOI is wrong, your cap rate is fiction. That's not a minor issue. It's the entire game.

The verified data is clear on this point. NOI comes from gross rental income minus operating expenses such as insurance, property taxes, and maintenance, while excluding debt service. If you include the mortgage, you're no longer calculating NOI.

What goes into NOI

Start with the property's recurring income. For a rental, that usually means collected rent and other steady income tied to normal operations.

Then subtract ordinary operating expenses. Think in plain English. What does it cost to keep the property functioning and producing income?

Common operating expenses include:

- Property taxes because the property can't operate without them.

- Insurance because it's a recurring ownership cost.

- Maintenance for routine upkeep and repairs.

- Management fees if the property needs active oversight.

- Utilities paid by the owner when tenants don't cover them.

- Common area costs on properties with shared spaces.

If you want a practical expense checklist, this roundup of 2026 rental expense deductions is a useful reference for the categories investors usually review.

What stays out of NOI

Beginners often get this wrong.

Do not include:

- Mortgage payments

- Loan interest

- Principal paydown

- Capital improvements

- Large one-time renovation costs

- Depreciation for cap rate purposes

Those items matter for cash flow, tax planning, and return analysis. They do not belong in NOI.

If a cost exists because of how you financed the deal, it's not an operating expense.

A practical workflow

When I review a property, I don't start with a fancy template. I start with a few blunt questions.

- What rent is being collected today? Not “market rent.” Actual collections.

- What expenses recur whether I like them or not? Taxes, insurance, repairs, management, utilities.

- What costs are temporary or capital in nature? Those stay out of NOI.

- What's missing from the broker sheet? Missing expenses are usually where bad deals hide.

A lot of offering memorandums understate repairs, management, or vacancy pressure. Don't blindly trust seller math.

A simple line-item example

Use a small rental as a working model. The exact mix will vary, but the logic stays the same.

| Line Item | Treatment in NOI |

|---|---|

| Rental income | Included |

| Parking or laundry income if recurring | Included |

| Property taxes | Subtracted |

| Insurance | Subtracted |

| Routine maintenance | Subtracted |

| Property management | Subtracted |

| Mortgage payment | Excluded |

| Renovation budget | Excluded |

| New roof or major upgrade | Excluded |

The point isn't to memorize categories. The point is to keep NOI tied to operations, not financing or one-off project costs.

A quick walkthrough can help if you want to see someone work through the logic visually:

The common-sense test

If the property were owned free and clear, would this income and expense still exist? If yes, it probably belongs in NOI. If no, it probably doesn't.

That simple test saves a lot of bad analysis.

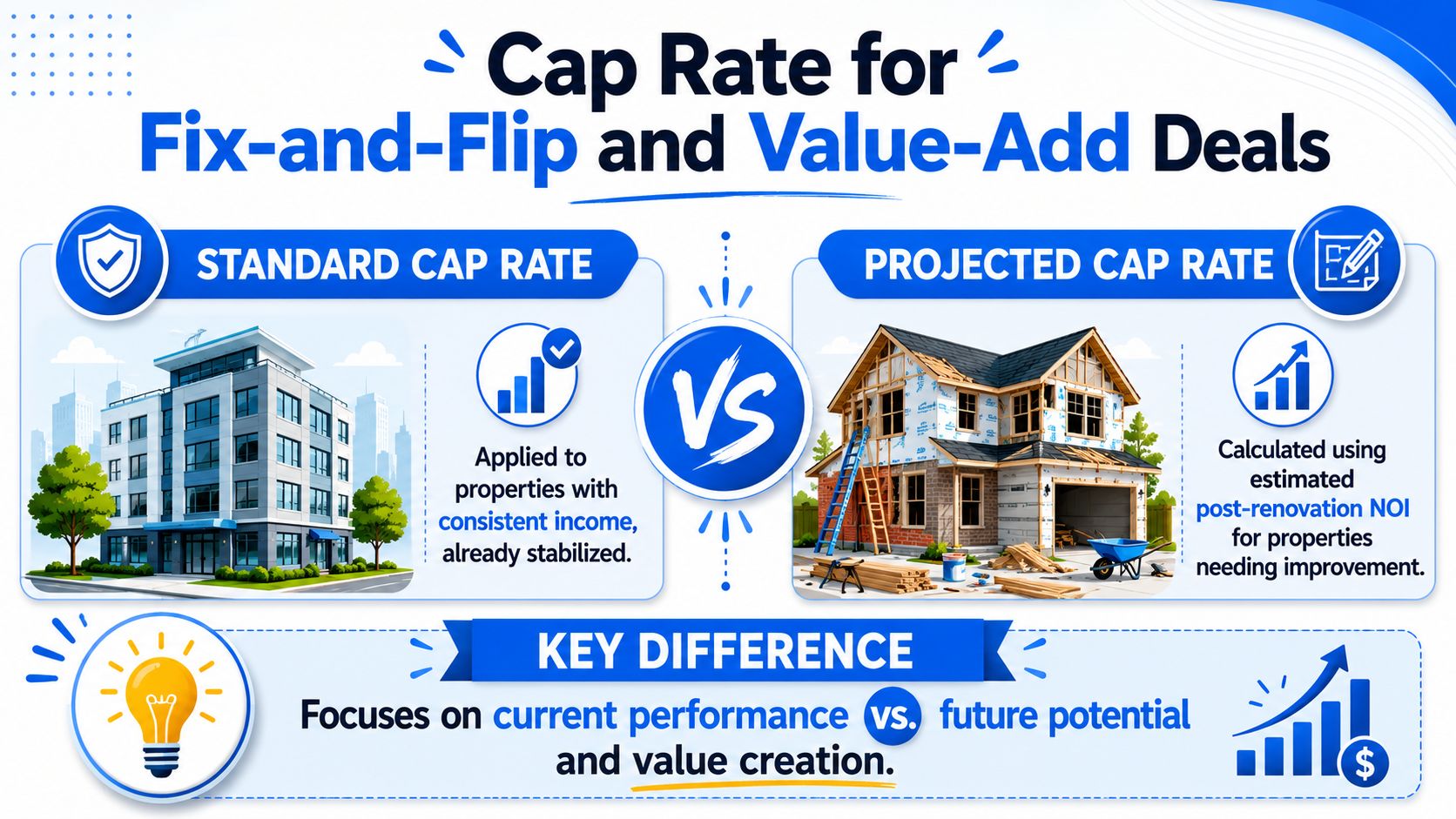

Cap Rate for Fix-and-Flip and Value-Add Deals

Most articles fall apart. They explain cap rate as if every property is already running smoothly. That's not how real deals look.

A neglected property with low rents, vacancy, or an unfinished rehab can't be judged by one cap rate alone. The verified guidance tied to PNC's cap rate overview makes the key point: for renovated or value-add properties, you need to separate in-place cap rate, projected or stabilized cap rate, and yield-on-cost because they can produce very different answers on the same project.

In-place cap rate

This uses the property as it sits today. Current income. Current operating reality. Current value or purchase price.

That number matters because it tells you how weak or strong the asset is on day one. If rents are under market, units are offline, or expenses are messy, the in-place cap rate may look ugly. That doesn't kill the deal. It just tells the truth about the starting point.

Stabilized cap rate

This is based on the property after the business plan works. Units are renovated. Rents are reset. Occupancy is normal. Expenses are cleaned up.

This number is useful, but it's also where investors start lying to themselves. If your projected rents are aggressive or your turnaround timeline is fantasy, your stabilized cap rate is fantasy too.

Underwrite the property you can actually create, not the one you want to brag about.

Yield-on-cost

This is the metric I think more investors should use on value-add deals. Instead of dividing NOI by current market value alone, you compare your stabilized NOI against your total project cost, including acquisition and rehab.

That tells you whether the repositioning effort creates enough income relative to the capital you're putting in. It's often the clearest way to judge whether a renovation plan makes sense.

When to use each one

| Metric | Best use |

|---|---|

| In-place cap rate | Judge the property's current performance |

| Stabilized cap rate | Evaluate the post-renovation business plan |

| Yield-on-cost | Test whether total project cost is justified |

PNC's guidance also notes that cap rates should be judged against like-kind comparables and adjusted for factors such as condition, tenant quality, and expected rent growth. That's critical. Don't compare a tired building with vacancy issues to a clean, stabilized asset and act like the same market cap rate applies without adjustment.

My recommendation for messy deals

Use all three views and keep them separate on paper. Don't blend current and projected numbers into one polished but misleading cap rate.

For fix-and-flip investors who pivot into rental holds, or for investors buying transitional assets, this is the difference between disciplined underwriting and wishful thinking. If you're active in that space, it also helps to understand how lenders look at rehab-heavy projects and bridge execution in fix-and-flip financing scenarios.

A good value-add analysis doesn't just ask, “What's the cap rate?” It asks, “Which cap rate are we talking about?”

Using Cap Rate to Price Deals and Secure Financing

Cap rate isn't just for screening. It's also a pricing tool.

The verified data gives the reverse formula plainly: Price = NOI / Cap Rate. That's one of the most useful shortcuts in real estate because it helps you back into a reasonable value based on income and market expectations.

Reverse the formula before you make an offer

One verified example shows that if a property has a first-year NOI of $80,000 and the market cap rate is 8%, the estimated value is $1,000,000 because $80,000 / 0.08 = $1,000,000.

That's the move smart investors use before they start negotiating. They don't ask, “What does the seller want?” They ask, “What does the income support?”

Why pricing discipline matters

The same verified data shows how sensitive value is to cap rate changes. If a property has $100,000 in NOI, a cap rate move from 5% to 7% drops value from $2,000,000 to about $1,428,571.

That's a brutal reminder. Small changes in market yield expectations can hit value hard. If you overpay because you used optimistic assumptions, the math won't forgive you later.

How this helps with financing

Lenders don't fund stories. They fund deals that make sense.

When you present a property with a clean NOI analysis, a supportable market cap rate, and a reasonable value conclusion, you make the lender's job easier. That doesn't guarantee approval, but it signals competence. And competent borrowers usually get further, faster.

For investors comparing funding paths, broad Hand Vetted Co. financing insights can help frame how different capital options fit different project types. If your focus is specifically non-owner-occupied property, this guide on financing investment property is also worth reviewing.

The borrower who knows the property's NOI, market cap rate, and realistic value almost always has a better conversation with a lender than the borrower who says, “I think it should appraise.”

A short offer test

Before you submit an LOI, ask yourself:

- Income test. Is the NOI real, or broker-polished?

- Market test. Are you using a cap rate from suitably comparable assets?

- Value test. Does the reverse cap rate formula support your price?

- Execution test. If the property needs work, have you separated day-one value from post-renovation value?

If those answers are solid, your pricing is probably in the right zip code.

Common Cap Rate Pitfalls and Your Next Step

Cap rate is useful because it's simple. It's dangerous for the same reason.

Most costly mistakes come from bad inputs, bad comparisons, or lazy projections. Investors overstate rents, ignore operating expenses, use the wrong denominator, or compare a rough asset to polished comps and call it “close enough.” It isn't.

The mistakes that hurt the most

- Using projected rent as if it already exists when the property is still underperforming.

- Leaving out real expenses like management, maintenance, insurance, or owner-paid utilities.

- Including debt service in NOI and corrupting the whole formula.

- Comparing different property types or conditions as if cap rates transfer cleanly.

- Relying on one cap rate for a transitional deal instead of separating in-place, stabilized, and yield-on-cost views.

The right mindset

Cap rate starts the conversation. It doesn't finish it.

A smart investor uses cap rate to decide whether to keep digging. Then they pressure-test NOI, validate comparables, and match the analysis to the actual business plan. That's especially important when the property is distressed, vacant, half-renovated, or being repositioned.

Good cap rate analysis is less about math and more about honesty.

If you stay honest about the income, the expenses, and the asset's true condition, cap rate becomes a sharp tool. If you use it to dress up a weak deal, it turns into a trap.

If you're buying, refinancing, or rehabbing non-owner-occupied property and need a lender that understands real-world deals, LendingXpress is a practical place to start. They work with investors who need speed, flexible structuring, and common-sense underwriting when traditional banks won't get there.