You found a property that should work on paper. The location is right, the spread looks good, and the renovation plan is straightforward. Then the financing stalls.

That's the point where many investors learn a hard truth about purchase and renovation loans for non-owner occupied properties. The deal may make sense to you, your contractor, and your agent. It still may not fit a bank's box. If the property needs work, if rent isn't there yet, or if your timing is tight, conventional financing often becomes the weakest part of the transaction.

The fix isn't just “find a lender.” The fix is matching the loan to the strategy, the property condition, and your exit. If you're flipping, you need one kind of structure. If you're planning to rehab, rent, and refinance, you need another. When you get that match right, the deal moves. When you don't, you burn time, lose bargaining power with the seller, and sometimes lose the property.

Funding Your Next Big Project When Banks Say No

A common scenario looks like this. You identify a non-owner-occupied property with clear upside, but it has an outdated kitchen, deferred maintenance, or condition issues that make a standard mortgage difficult. The seller wants a fast close. Your contractor is ready. The bank asks for a cleaner property, more documentation, and more time than the deal allows.

That friction is real in the broader market. Urban Institute research reports that renovation loans have a 43% denial rate versus 10.6% for standard purchase loans, which shows how much harder it is to combine acquisition and rehab through traditional channels (Urban Institute chartbook).

Why banks hesitate

Banks struggle with these deals for predictable reasons.

- Condition risk: If the property needs substantial repairs, it may not meet normal lending standards at closing.

- Execution risk: The lender has to trust that the renovation plan is realistic and that the work will be completed.

- Exit uncertainty: A flip depends on resale timing. A BRRRR deal depends on refinance timing and lease-up.

- Valuation complexity: Future value is harder to underwrite than current value.

A conventional lender usually wants the property, borrower, and timeline to be clean and easy to document. Distressed or transitional properties rarely look clean on paper.

What works instead

Private and hard money lending exists for this exact gap. These lenders don't ignore risk. They underwrite it differently. They focus on the asset, the rehab scope, your equity, and whether the exit plan is credible.

Practical rule: If your deal depends on speed, property condition, or a staged renovation plan, don't start by asking which lender has the lowest rate. Start by asking which lender can actually close the structure your deal needs.

The right financing can turn a rough property into a financeable opportunity. The wrong financing can kill a deal that otherwise had strong margins.

Understanding Your Financing Options

Most investors don't need a long list of loan products. They need a fast way to decide which structure fits the business plan. That's the better way to think about purchase and renovation loans for non-owner occupied properties.

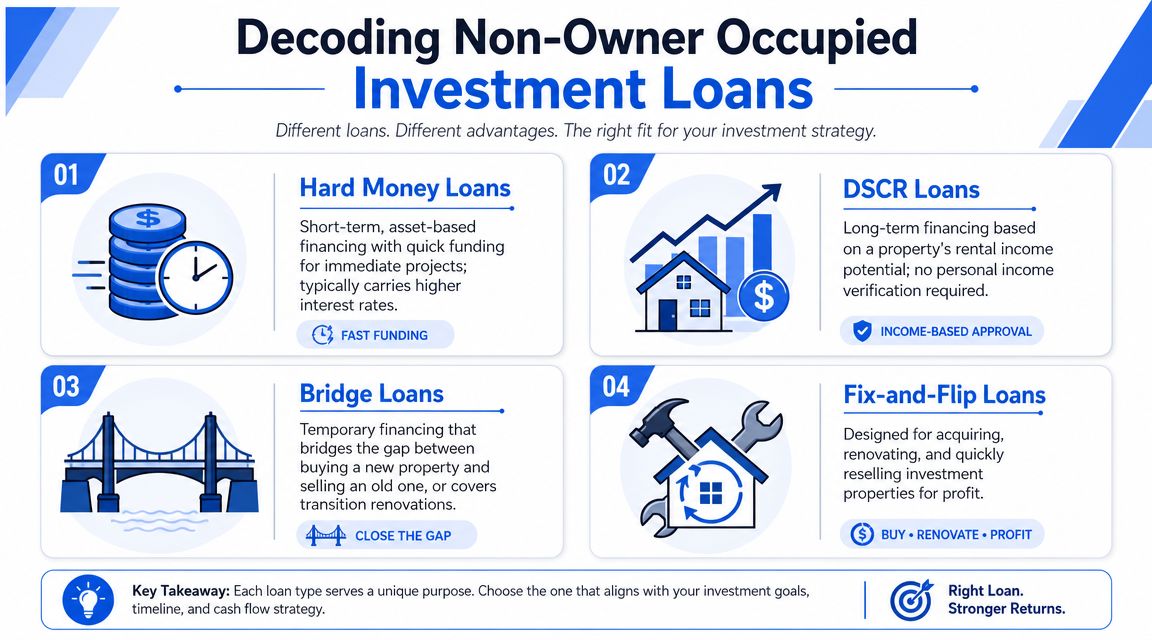

The four loan types investors use most

Hard money loans work when speed and property condition matter more than perfect documentation. They're usually asset-focused and useful for distressed acquisitions, short timelines, and borrowers who need flexibility.

Bridge loans fit transitional situations. You may use one to buy a property that isn't ready for permanent financing yet, or to carry the project through rehab and lease-up until you refinance or sell.

Fix-and-flip loans are purpose-built for the short hold. They combine purchase money and rehab funds with the expectation that you'll improve the property and exit by sale.

DSCR or rental loans are for the long hold, not the heavy lift at the front end. They're commonly used after the property is stabilized, repaired, and either rented or ready to be rented.

If you want a broader view of how experienced operators think about real estate investor financing, that overview is useful because it frames financing as part of the investment plan, not just a loan search.

Purchase and Renovation Loan Comparison

| Loan Type | Best For | Term Length | Underwriting Focus | Rehab Funding |

|---|---|---|---|---|

| Hard Money | Fast purchases, distressed assets, borrowers needing flexible structure | Short-term | Asset, equity, exit plan, property condition | Often staged through draws |

| Bridge | Transitional deals, lease-up, refinance-to-stabilization strategy | Short-term | Collateral and clear exit strategy | Can be structured with construction draws |

| Fix-and-Flip | Investors planning to renovate and sell | Short-term | Deal viability, scope of work, resale plan | Commonly tied to approved rehab budget and draws |

| DSCR or Rental | Stabilized buy-and-hold properties | Longer-term | Property income potential and long-term hold strategy | Usually not the first choice for heavy rehab at acquisition |

How to choose based on strategy

Use a fix-and-flip loan when the property's value will come from renovation and resale. The loan should support a short business cycle and a defined rehab schedule.

Use a bridge loan when the property is in transition. That could mean the asset needs work before it qualifies for permanent financing, or you need time to stabilize it before moving into a rental loan.

Use hard money when the deal is messy, time-sensitive, or outside normal bank underwriting. That includes inherited properties, heavy deferred maintenance, and fast seller deadlines.

Use DSCR or rental financing after the hard part is over. Once the property is improved and income-ready, long-term debt makes more sense than short-term capital.

The biggest mistake investors make here is choosing the cheapest loan instead of the loan that matches the execution plan.

A practical next step is reviewing how financing structures differ for rentals versus rehab deals. This guide on how to finance investment property is useful if you're comparing short-term acquisition financing with a longer-term hold strategy.

How to Qualify for a Purchase and Renovation Loan

Qualification for non-owner-occupied rehab financing is more practical than many borrowers expect. Private lenders still underwrite carefully, but they usually care less about fitting your file into a rigid consumer-mortgage template and more about whether the deal is financeable.

What lenders actually look at

The first issue is equity. For investment property lending, the debt-to-equity ratio is managed carefully. Conventional investment-property mortgages often require 15% to 30% down, and lenders use that higher equity contribution to offset vacancy and renovation risk while paying close attention to reserves and deal strength (Quicken Loans overview of non-owner-occupied mortgage requirements).

The second issue is your plan. A good file answers basic questions clearly:

- What are you buying?

- What work are you doing?

- How long should the project take?

- How do you exit the loan?

If any of those answers are vague, underwriting gets harder.

The file that gets approved faster

Bring the lender a package that shows control, not just interest.

- Purchase contract: The signed agreement tells the lender where the basis starts.

- Scope of work: A line-item rehab budget matters more than broad statements like “full cosmetic remodel.”

- Experience summary: If you've done similar projects, say so clearly. If you haven't, show who is helping manage the job.

- Liquidity evidence: Lenders want to know you can cover payments, overruns, and surprises.

- Entity documents: If you're borrowing in an LLC or other entity, have the paperwork ready.

A clean document package reduces back-and-forth. For borrowers who want a simple prep list before applying, this essential mortgage checklist 2025 is a helpful organizational tool.

What doesn't work

Some borrowers try to qualify with a strong story but weak documentation. That rarely ends well. A lender can't underwrite “I'll figure out the contractor later” or “the property should be worth a lot more once it's nicer.”

A rehab lender doesn't need perfection. They do need evidence that you understand the project, the budget, and the exit.

The strongest submissions are boring in a good way. Clear scope, realistic timeline, enough cash, and a believable plan.

How Rehab Funding and Draws Actually Work

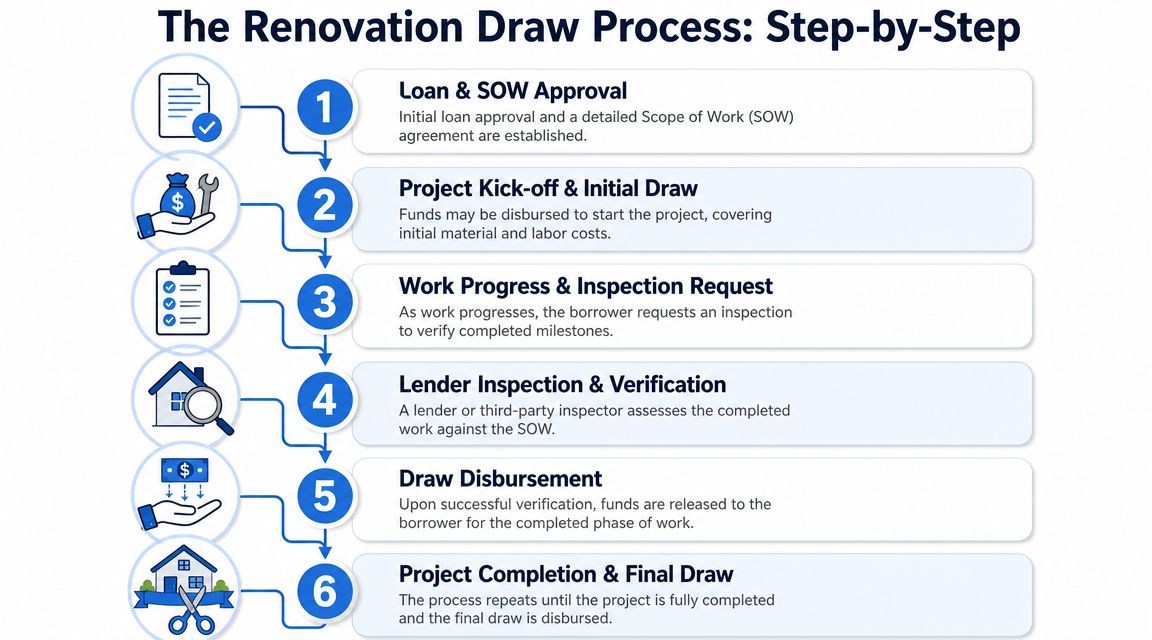

Rehab money usually doesn't hit your account in one lump sum at closing. Most lenders control renovation funds through a draw process. That protects the lender, but it also helps keep the project organized.

Think of rehab funds as an approved construction allowance. The lender agrees to fund a defined budget, then releases money as work is completed and verified.

The valuation issue that surprises investors

The hardest part of rehab financing usually isn't whether a lender likes your budget. It's whether the valuation supports the proceeds you expect. As MortgageDepot explains, the critical question isn't just whether you can finance the rehab, but how much of the project the lender will recognize in the valuation. Loan proceeds are constrained by an after-improvement appraisal, so tighter assumptions can reduce proceeds even when the scope of work is solid (MortgageDepot explanation of non-owner-occupied renovation loans).

That's why two investors can bring the same rehab concept to different lenders and get different usable financing. The budget may look fine. The appraisal assumptions may not.

The draw cycle in plain English

Loan approval and scope review

The lender approves the project based on the purchase, budget, valuation, and exit.Closing

Purchase funds are wired. Rehab funds are typically held back.Work begins

Your contractor starts according to the approved scope.Inspection request

Once a phase is complete, you request a draw.Verification

The lender or inspector checks completed work against the approved budget.Funds released

Draw money is disbursed for verified work.

Here's a visual walkthrough of that process.

What borrowers should ask before signing

Not all draw systems feel the same in practice. Ask these questions early:

- How are draws requested? Some lenders are simple and responsive. Others create delays with too many steps.

- What counts as completed work? You want clarity before the first inspection.

- Can initial funds be released for materials or startup costs? That affects your upfront cash needs.

- How are change orders handled? Real projects shift. Your lender should have a process.

If you're evaluating rehab structures in more detail, this article on using rehab loans to fund real estate investment projects gives a practical look at how investors use these funds on active deals.

Real-World Scenarios Fix and Flip vs Buy and Hold

The same property can lead to two different loan choices depending on the business plan.

Scenario one for a fix and flip

An investor contracts a dated single-family property in a strong resale neighborhood. The house needs a fast cosmetic and systems update. The investor doesn't need long-term financing. The investor needs to acquire, renovate, and sell without wasting time in a bank pipeline.

A fix-and-flip or short-term hard money structure fits because the exit is sale, not long-term hold. Underwriting centers on the purchase basis, the rehab scope, the projected finished value, and whether the timeline is realistic.

What works in this scenario:

- A short loan term

- Interest-only carrying structure

- Rehab funds tied to a clear draw schedule

- A contractor who can move quickly

What usually doesn't work is trying to force the deal into a standard mortgage just because the rate looks lower. The lower rate means very little if the seller won't wait or the property won't qualify in current condition.

Scenario two for a BRRRR investor

A different investor buys a non-owner-occupied property with the intent to buy, rehab, rent, and refinance. The plan is not resale. The plan is to create a finished rental asset and then replace the short-term loan with permanent debt.

A bridge-to-rental approach usually makes more sense. The bridge loan carries the acquisition and renovation phase. After repairs are complete and the property is leased or lease-ready, the investor refinances into a DSCR or other rental loan.

If your true goal is long-term cash flow, don't choose your first loan as if the project ends at closing. Choose it based on the refinance path you'll need later.

What works here is keeping the rehab scope disciplined. A BRRRR project can fail if the renovation timeline drifts, the budget expands, or the refinance assumptions were too optimistic at the start.

The strategy should drive the capital stack. Flippers need speed and resale flexibility. Buy-and-hold investors need a clean path from transition debt into stable long-term financing.

Choosing the Right Lending Partner

The wrong lender can kill a good deal even after you get approved.

For a fix and flip, slow underwriting and sloppy draw management can leave your contractor idle and your holding costs rising. For a BRRRR project, the bigger risk is choosing a lender who will fund the purchase and rehab but does not care whether your refinance path still works once the property is stabilized. The right partner is the one whose process fits your strategy, timeline, and exit.

A term sheet only tells part of the story. You also need to know how the lender handles real friction. Appraisal revisions, title issues, insurance questions, contractor changes, and draw disputes are what delay closings and disrupt rehabs.

What to look for

- A clear approval process: Ask who makes the credit decision and who can clear conditions fast.

- Fees you can model: Review rate, points, draw fees, extension costs, inspection charges, and reserve requirements before you commit.

- Fast, predictable draws: A lender with a weak draw process creates jobsite delays and unnecessary change orders.

- Experience with your plan: A flip lender should understand resale timing. A BRRRR lender should understand how rehab scope, rent, and refinance timing connect.

- Direct communication: You want real answers from someone who can solve problems, not generic updates from a portal.

If you are buying for long-term hold, test the deal before you close. Tools for estimating rental property profits can help you check whether the stabilized numbers still make sense after debt service, rehab costs, and operating expenses.

A simple due diligence check

Ask every lender the same three questions.

How fast can you close with a complete file? How are rehab funds released and how long do inspections take? What are the most common reasons your deals get delayed after term sheet?

Then compare the answers against your actual business plan. A flipper usually needs certainty of execution and responsive draws. A BRRRR investor usually needs a lender who can fund the front end without creating problems for the refinance on the back end.

Good investors do not choose a lending partner by rate alone. They choose the lender most likely to get this specific deal to the finish line.

Frequently Asked Questions for Investors and Brokers

Do I need a contractor bid before I apply

You don't always need a final bid on day one, but you do need a clear scope of work. A lender can't evaluate rehab funds without knowing what work is planned, what it should cost, and whether the timeline is plausible.

Can I do the renovation work myself

Sometimes, but many lenders prefer third-party contractors, especially on larger or more technical projects. If you plan to self-manage or self-perform part of the work, raise that early. The lender will want to know your experience and how inspections will verify progress.

How is after-repair value determined

It's typically based on an appraisal that considers the property's expected condition after the approved improvements are completed. The appraiser reviews the scope of work and compares the finished product to relevant renovated properties. If the valuation comes in tighter than expected, your proceeds may be lower even if the rehab plan is solid.

Can I buy in an LLC

Often yes, especially for business-purpose non-owner-occupied borrowing. But you should have your entity documents organized before closing. Last-minute entity cleanup causes avoidable delays.

What are typical closing costs

They vary by lender and deal structure. Instead of guessing, ask for a full fee summary early. You want to see origination charges, third-party reports, title and escrow items, draw-related charges, and any extension terms in writing.

What helps a broker get these deals done faster

A complete package. Send the purchase contract, scope of work, borrower summary, entity documents if applicable, and a short explanation of the exit. Brokers who package the story cleanly usually get faster answers and fewer conditions.

If you're working on a non-owner-occupied purchase and rehab deal and need a lender who can look at the asset, the plan, and the timeline in practical terms, LendingXpress is worth a look. Reach out early in the process so you can match the financing structure to your strategy before the deal gets stuck.