Flex space is a hybrid commercial property that combines office, warehouse, and sometimes showroom space in one unit, usually in the 500 to 2,500 square foot range. It's built for adaptable use, with layouts that can shift between office-heavy and warehouse-heavy needs, clear ceiling heights of 14 to 20 feet, and garage doors that are typically 12 to 14 feet high.

If you're looking at commercial deals right now, you've probably run into the same problem many investors do. Traditional office feels exposed. Pure retail can be tenant-specific. Standard industrial is strong, but not every tenant needs a full warehouse box. Flex space sits in the middle, and that's exactly why it keeps showing up in smart portfolios.

The simple version of what is flex space is this. It solves a real business need. Small distributors, e-commerce operators, trades, light manufacturers, service companies, and growing local businesses want one place where they can store product, run admin, meet clients, and keep overhead under control. Investors like it because that demand is practical, not trendy.

Where most articles stop at the definition, the essential work starts with financing. Flex space often looks attractive on paper, but many lenders hesitate once they see mixed use, unclear zoning, unusual layouts, or a tenant mix that doesn't fit a bank's standard box. That's where deals either move forward or die.

Your Next Investment in a Changing Economy

Investors are hunting for assets that can handle economic uncertainty without becoming dead weight. That usually means avoiding property types that rely on one narrow tenant profile or one rigid use. Flex space earns attention because it can serve several business models inside the same footprint.

That matters more now than it did a few years ago. Businesses don't want to commit to space they can't adapt, and landlords don't want buildings that only work for one kind of occupant. According to Building Engines on flex space in commercial real estate, by 2030, industry analysts predict flexible space will account for approximately 30% of the total commercial real estate market. That projection is tied to remote and hybrid work reshaping how companies use space.

Why investors keep circling back to flex

Flex space gives you options when the market changes. A conventional office suite can sit empty if a tenant cuts headcount. A specialized industrial property can take longer to backfill if the buildout is too narrow. A flex unit can appeal to a broader set of tenants because the use case is more forgiving.

Practical rule: The more ways a tenant can use a property without major reconstruction, the easier that property is to lease, reposition, or sell.

The financing angle matters just as much. A flexible asset can be a strong investment, but only if you line up capital from a lender that understands hybrid commercial property. Investors who treat financing as an afterthought often lose the deal to a buyer who came in with a workable loan structure from day one.

What makes this asset class different

Three things separate flex from other commercial categories:

- It serves small and midsize operators well. These tenants often need office, storage, and operational space together.

- It can be reworked without a total gut job. That helps both lease-up and resale.

- It demands smarter underwriting. Mixed use, zoning language, and lease structure can complicate a loan even when the property itself makes perfect sense.

That last point is where experienced borrowers gain an edge. If you know how lenders look at flex, you can buy better, underwrite faster, and avoid chasing financing that was never realistic.

The Anatomy of a Flex Space Property

Flex space is the Swiss Army knife of commercial real estate. One unit can handle front-office administration, back-end storage, light assembly, customer meetings, and even limited showroom use. That versatility is the whole point. It isn't just “small industrial” and it isn't just “office with a roll-up door.”

According to WorkBay's flex space glossary, flex space units typically range from 500 to 2,500 square feet and often include clear ceiling heights of 14 to 20 feet with garage doors at least 12 to 14 feet high. Those physical specs are what open the door to mixed business use.

What the layout usually looks like

A true flex property blends different functions under one roof. The office component can be minimal or substantial depending on the tenant. In many buildings, the office share can shift from a small administrative corner to a large customer-facing area, while the rest of the space supports storage, production, shipping, or service operations.

That matters because tenants rarely need a “perfect” traditional layout. They need a workable one.

Typical features include:

- Front office area. Reception, desks, private office, or a small conference room.

- Warehouse or open work area. Storage, inventory, assembly, fulfillment, or equipment staging.

- Access for operations. Roll-up doors, loading access, and enough vertical clearance to make the space functional.

- Adaptable partitions. Modular walls and open spans that let tenants reconfigure use over time.

How flex differs from office, retail, and industrial

A standard office building is built for desk work. A retail unit is built for foot traffic and customer presentation. A pure industrial building prioritizes storage, shipping, or manufacturing. Flex space sits between those categories.

Here's the practical distinction:

| Property type | Best use | Main limitation |

|---|---|---|

| Office | Administration, meetings, professional services | Weak for storage or operations |

| Retail | Sales, visibility, customer traffic | Often inefficient for back-end operations |

| Industrial | Warehousing, shipping, production | Can be too raw for office or client-facing needs |

| Flex space | Mixed operations under one roof | Can confuse inexperienced lenders |

If you want a feel for how the workspace side of this category overlaps with modern occupier demand, Freeform House's guide to best flexible workspaces is useful context. It shows why adaptable space has become normal for many businesses, even outside traditional industrial leasing.

The tenant profiles that fit best

Flex space tends to attract operators who can't justify a large specialized building but have outgrown a simple office suite or storage unit.

Common examples include:

- E-commerce businesses. They need inventory space plus desks for customer service and admin.

- Trades and home service companies. Plumbers, electricians, HVAC contractors, and similar operators use the office for dispatch and the warehouse side for tools and materials.

- Light industrial users. Small assembly, fabrication, and packaging businesses often fit well.

- R&D or product development teams. They may need office, testing, storage, and meeting space in one unit.

- Showroom-based operators. Some businesses need a front-facing display area with operations in back.

A flex unit works best when the tenant's business has more than one function and doesn't want to pay for separate locations.

That broad utility is a big reason investors like the category. WorkBay also notes that the industrial real estate market that includes flex space has historically increased in value by approximately 11% per year in its cited overview. The exact result on any single property depends on purchase basis, tenant quality, location, and financing structure, but the appeal is clear.

Why Flex Space Is Gaining Market Momentum

Demand for flex space isn't coming from one trend. It's coming from several practical shifts happening at the same time. Businesses want shorter commitments, more efficient layouts, and locations that can support both administrative work and physical operations without paying for excess square footage.

The tenant demand is broad, not narrow

Small logistics operators need local distribution space. Service businesses need storage and dispatch in one place. Product companies need room for samples, shipping, and staff. Flex space meets those needs without forcing tenants into a bigger industrial lease than they can use.

That broad demand base helps investors in a simple way. When one tenant type slows down, another may still be active. You're not relying on one highly specialized use.

A few strong drivers keep showing up:

- Local fulfillment needs. Small and midsize operators want space close to customers.

- Service business growth. Many trades need a practical base of operations, not a polished office tower.

- Hybrid work habits. Teams still need in-person space, but they want it to do more than hold desks.

Why investors like the lease story

Flex space usually gives tenants room to grow without leaving the property immediately. A company may start with more warehouse use and later add office buildout, or do the opposite. That kind of scalability can help retention because the space adapts as the business changes.

Investors also benefit from that same flexibility on the ownership side. If one leasing strategy stalls, the building may be repositioned for a different tenant profile without an extreme overhaul.

For a wider look at how occupiers are rethinking layouts and operational planning, Facility Management Insights has a solid piece on workspace management for 2026. It's useful because it connects day-to-day workspace decisions with the broader move toward adaptable properties.

A short overview helps frame the shift in practical terms:

What doesn't work

Not every flex deal is automatically good. Investors get into trouble when they buy a building that's too customized, poorly located, or physically awkward for everyday users. A property can be labeled “flex” and still be hard to lease if truck access is poor, the office buildout is excessive, or the warehouse side is too compromised to function.

Buy for utility first. Marketing language won't save a space that's inconvenient for the tenant's actual workflow.

The strongest flex assets are simple to understand when you walk them. The tenant can receive goods, store product, run the office, and serve customers or crews without friction. When a building does that well, momentum usually follows.

Valuing and Underwriting Flex Space Investments

A lot of investors assume valuing flex space is straightforward. It isn't. A hybrid property can look simple from the street and still create underwriting headaches once a lender starts asking how much of the building is office, how much is warehouse, what the zoning allows, and whether the current use matches the legal use.

Why hybrid use complicates valuation

A bank loves clean labels. Office. Industrial. Retail. Flex space doesn't always fit neatly into any one of them. That creates friction in appraisal selection, comparable sales analysis, and loan sizing. If the appraiser uses the wrong comp set, value can come in soft. If the lender's credit box doesn't allow mixed-use ambiguity, the deal stalls before it gets serious.

During this stage, experienced investors spend more time before submitting a loan package. They verify legal use, current tenancy, configuration, and whether the property's income story matches its physical design.

Key underwriting questions usually include:

- How functional is the office-to-warehouse mix? A layout that works for real tenants supports value better than one that looks overbuilt.

- What does the zoning permit? Legal conformity matters more than marketing language.

- Who is the likely next tenant? Exit liquidity depends on re-tenanting potential, not just the current lease.

- Does the building need repositioning? Deferred maintenance or awkward buildout can shrink lender comfort.

Zoning can change the whole deal

Regulation can improve a flex project or make it harder to finance. According to DeskFlex's discussion of flex space and zoning, in late 2024, 14 new California cities adopted flex zoning ordinances allowing 12% higher square footage for mixed-use flex units, with reported ROI potential increasing by 8 to 11% for developers. For investors and lenders, that's not just a planning issue. It directly affects the business plan, valuation upside, and whether an improvement strategy is financeable.

That's why smart borrowers don't submit a loan request with a vague story. They come in with the zoning summary, lease plan, and renovation scope already aligned.

What lenders want to see before they say yes

A strong flex loan package usually includes clear documentation that reduces interpretation risk. The easier you make the story to underwrite, the faster the lender can move.

A practical checklist looks like this:

- Rent roll and lease summary. Keep it clean and easy to read.

- Current photos and site notes. Show office area, warehouse area, access points, and any deferred issues.

- Zoning confirmation. Don't assume the use is obvious.

- Business plan. Stabilize, renovate, re-tenant, refinance, or sell. Pick one and support it.

- Financing request matched to the plan. For investors exploring options, commercial property investment loans give a useful reference point for how these deals can be structured.

Underwriting gets easier when the borrower has already answered the questions that usually kill mixed-use loans.

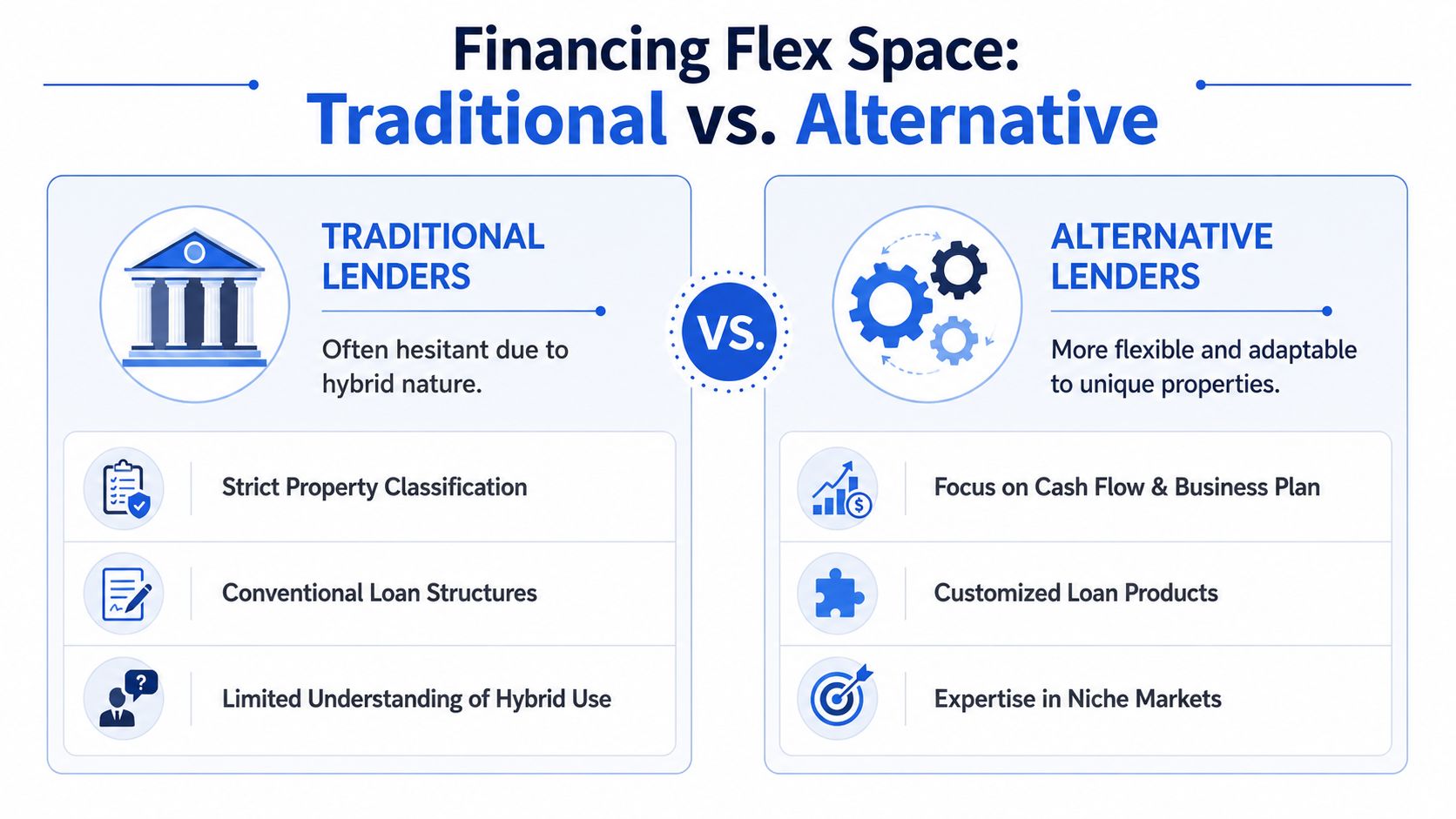

Financing Flex Space When Traditional Lenders Falter

Under these circumstances, many good flex deals run into a wall. The property works. The tenant demand is there. The numbers may pencil. Then the lender gets involved and starts treating the deal like a problem file because the asset doesn't fit a standard category.

Traditional banks often struggle with non-owner-occupied flex space for a few reasons. They may dislike short leases, mixed layouts, older business park inventory, or zoning language that requires interpretation. Even private lenders can pass if they don't know how to underwrite a property that serves multiple uses under one roof.

What makes these loans harder

For investment properties, the borrower already faces stricter financing standards than an owner-occupant. As noted by LoanGuys on owner-occupied versus non-owner-occupied loans, non-owner-occupied loans typically require a down payment of 20 to 30%. Related guidance from Free & Clear on reserve requirements for non-owner-occupied mortgages states that lenders may also require cash reserves of six or twelve months of total monthly housing expenses at closing, depending on the borrower profile and loan type.

Those requirements aren't impossible. But they become harder to satisfy when the property itself also needs a lender comfortable with mixed-use underwriting.

Traditional bank loan versus private lending

Here's the practical comparison investors care about most:

| Issue | Traditional lender response | Private lender response |

|---|---|---|

| Hybrid property type | Often wants a tighter category fit | More willing to underwrite actual use |

| Speed | Slower committee process | Faster decision path |

| Value-add plan | Can be restrictive | Often more adaptable |

| Non-owner-occupied borrower profile | Heavy documentation and reserve review | More room for asset-based common-sense review |

That doesn't mean private capital ignores risk. It means the lender can judge the asset, the exit, and the borrower's plan without forcing every flex deal into a standard bank template.

When private capital makes the most sense

Private money is often the better fit when you need to close quickly, when the property needs renovation, when the tenant story is still being stabilized, or when the bank has already said no for reasons that have more to do with policy than with the actual deal.

These are common scenarios:

- Bridge acquisition. You found a flex property with a short closing window and can't wait through a conventional process.

- Value-add repositioning. The unit needs buildout changes, lease-up work, or deferred maintenance addressed before a bank will touch it.

- Refinance of an existing loan. You need more time to stabilize the asset before moving into long-term debt.

- Cash-out for improvements. You want to upgrade loading, office layout, or curb appeal to widen the tenant pool.

One financing path investors use for this type of property is hard money lender loans, especially when timing matters more than rate shopping and the plan depends on speed. In that lane, LendingXpress is one example of a California private lender that finances non-owner-occupied residential and commercial assets, including scenarios where borrowers need quick bridge capital and rehab funding tied to an investment business plan.

If a lender spends more time arguing about what to call the property than how to finance it, you're probably talking to the wrong lender.

What works in the loan package

Borrowers improve their odds when they present the property as an operating asset, not just a building with mixed features. The package should make the lender comfortable with both present value and exit.

The strongest submissions usually include:

- A clear use narrative. Explain who the target tenant is and why the layout fits.

- Realistic renovation scope. Show what changes are needed and why they matter.

- Exit clarity. Refinance, sale to another investor, or sale to an owner-user.

- Clean borrower organization. Entity docs, insurance plan, and timeline should already be in order.

What doesn't work is a vague pitch built around “flex is hot.” Lenders fund specific plans. They want to know how you'll create stability, not just that the category is attractive.

Risks Exit Strategies and Your Next Steps

Flex space has real upside, but it isn't a free pass. Tenant turnover can be higher than in some longer-term industrial holdings. Mixed-use layouts can narrow the buyer pool if the property is overbuilt for one use. And if you miss on zoning, access, or functionality, the same flexibility that looked appealing on paper can become a leasing problem in practice.

The risks worth managing early

Most flex problems can be reduced before closing if you stay disciplined.

A practical risk screen includes:

- Tenant fit risk. Match the layout to a broad user base, not one highly specific occupant.

- Physical utility risk. Confirm access, loading, clear height, and office ratio are practically usable.

- Financing risk. Know your loan path before you go hard on deposits.

- Exit risk. Underwrite who will buy the property from you, not just why you want it now.

Buy the next borrower's refinance and the next buyer's purchase. If neither one makes sense, your current deal probably needs another look.

Three exits that usually make sense

Most investors in flex space are working toward one of three outcomes.

First, you can stabilize and sell to another investor. This works well when leases are in place, the building is cleaned up, and the income story is easy to understand.

Second, you can sell to an owner-user. Many small businesses want exactly this kind of property because it lets them control operations and occupancy in one location.

Third, you can refinance into longer-term debt once the property is leased, improved, and documented well enough for a conventional lender to get comfortable. For broader planning around these outcomes, Homebase has useful insights on real estate exit planning that pair well with flex acquisitions.

What to do next

If you're evaluating what is flex space from an investor's angle, start with the basics. Walk the building with a tenant-use mindset. Confirm zoning before assuming anything. Build your financing plan before you negotiate like capital is guaranteed.

Then move fast when the deal checks out. Good flex properties often attract buyers who understand that adaptable space solves practical business problems. If you want to compete on those deals, your financing has to be ready before the property goes fully competitive.

If you're buying, refinancing, or repositioning a non-owner-occupied flex property and need a lender that can evaluate the deal on its actual merits, LendingXpress is worth a look. The firm focuses on private real estate lending for investors who need speed, flexible structuring, and a clearer path forward when traditional financing doesn't fit the property or the timeline.