You found a property that fits your strategy. The price makes sense, the location works, and the upside is clear. Then the financing stalls.

A bank asks for layers of paperwork, wants to study your personal income, and moves on a timeline that doesn't match the deal. Sellers don't wait for that. Brokers don't wait for that. Good opportunities definitely don't.

That gap is where asset-based real estate lending for LLCs becomes useful. If you're buying, refinancing, rehabbing, or stabilizing a non-owner-occupied property through an entity, this approach can help you move when conventional lending can't.

Seize Real Estate Opportunities Banks Make You Miss

The most common version of this problem looks like this. An investor finds a rental or mixed-use property that needs quick execution. The deal is solid, but the file doesn't fit a bank box. Maybe the borrower is self-employed. Maybe the property needs work. Maybe the LLC is new. Maybe prior tax returns don't tell the actual story.

The bank still underwrites the borrower first and the property second. That works for owner-occupied homes. It often fails real investors.

Asset-based real estate lending for LLCs flips that order. The lender looks at the property, the collateral, the cash flow path, and the exit. If the property supports the loan, the deal can move. That's why investors often use it for acquisitions, short-term holds, rehab projects, and transitional assets.

This isn't some fringe corner of lending. The global asset-based lending market was valued at USD 661.7 billion in 2023 and is projected to exceed USD 1.5 trillion by 2032, according to GM Insights on the asset-based lending market. That matters because it shows the structure is a standard financing model, not a workaround used only when everything else fails.

Where the opportunity usually gets lost

A bank tends to slow down when any of these show up:

- Entity ownership: The property is being bought in an LLC, not personal name.

- Property condition: The building needs renovation or lease-up before it fits long-term financing.

- Complex income: Your tax returns don't reflect current liquidity or real estate experience.

- Short deadlines: The seller wants a fast close, or the property came with a real deadline.

In those situations, investors usually need a bridge, not a lecture.

If the business plan is short-term, a lender focused on collateral and execution is often a better fit than a conventional lender trying to force an investment deal into a consumer mortgage process. For investors comparing short-term options, a bridge loan for investment property is often the first place to start.

The best financing isn't the cheapest quote on paper. It's the loan that lets you actually close the deal you want.

Understanding the Asset-Based Lending Philosophy

A traditional bank loan asks, "How strong is the borrower?" Asset-based lending asks, "How strong is the asset, and what is the plan?"

That difference changes almost everything about how a file is reviewed.

What the lender is really underwriting

In asset-based real estate lending for LLCs, the property sits at the center of the deal. The lender wants to know what it's worth today, what condition it's in, what income it produces or can produce, and how the loan gets paid off.

Published real estate facility parameters show advances of up to 80% of appraised fair market value, with 2- to 4-year terms, and asset-based loans often have weighted-average lives of 1 to 2 years, which is why they're commonly used for fast, short-term capital, as outlined by First Business Bank's asset-based lending parameters.

That structure tells you the philosophy. These loans are built around collateral coverage and a realistic timeline, not around proving stable W-2 income over a long lookback period.

Why the legal side matters

When real estate secures the loan, lien position matters. The lender wants a clean, enforceable security interest in the collateral and clear authority for the LLC to borrow. If you want a plain-English primer on that side of the process, Kons Law on security interests gives useful context on how lenders protect their claim.

From a practical standpoint, borrowers should expect scrutiny in a few areas:

- Title and lien position: The lender wants to know who has rights against the property.

- Entity authority: The operating agreement and resolutions have to show who can sign.

- Exit clarity: Refinance, sale, or stabilization has to be believable.

- Liquidity: Even when personal income isn't the main focus, borrowers still need enough cash to execute the plan.

Practical rule: "Asset-based" doesn't mean "no underwriting." It means the underwriting is aimed at the property first.

A strong borrower with a weak asset still struggles. A strong asset with a clean plan can often get done even when the borrower's tax-return story is messy.

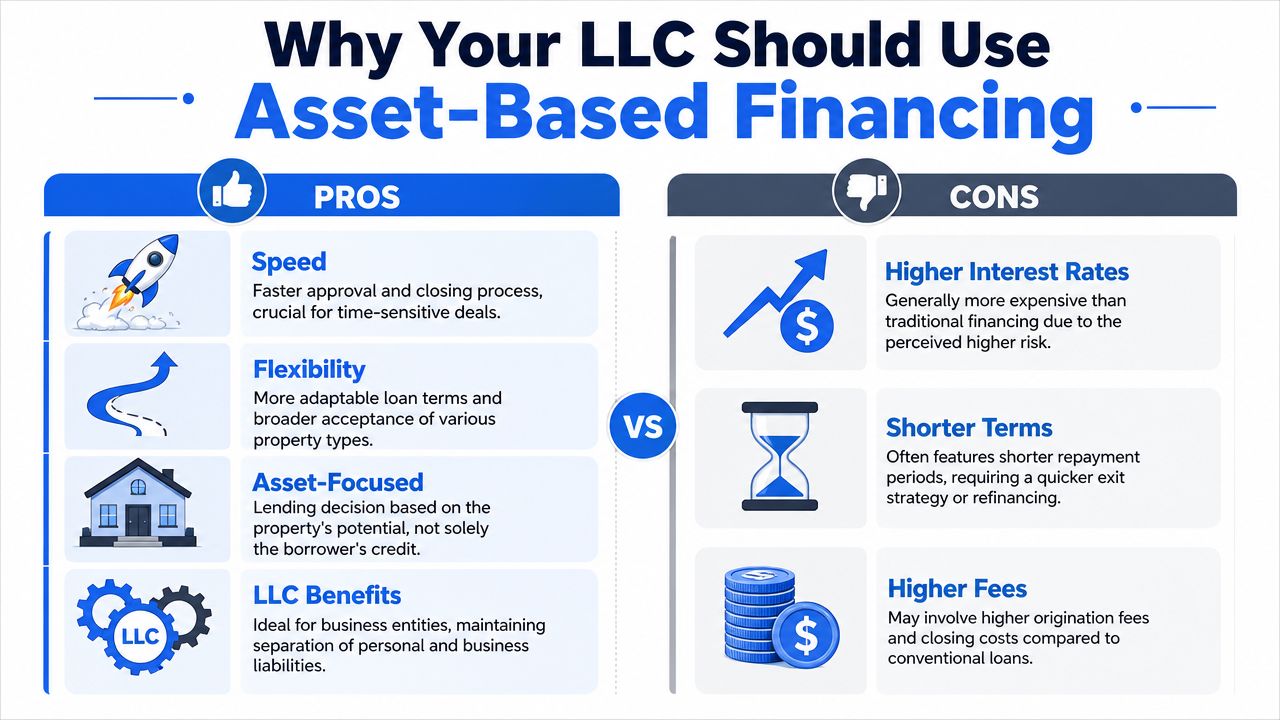

Why Your LLC Should Use Asset-Based Financing

For the right investor, this loan type isn't just a fallback. It's a tool.

When speed matters, entity-based investing usually benefits from financing that matches the deal rather than forcing the deal to match the lender. That's where asset-based lending can make sense for acquisitions, cash-out refinances, and transitional properties that need time before permanent debt fits.

When this approach works well

Asset-based financing is usually a strong fit when the property is the story.

- Fast acquisitions: You need to close quickly to win the deal.

- Value-add projects: The asset needs rehab, lease-up, or cleanup before a bank will touch it.

- Entity ownership: You want the property held in an LLC for business and liability reasons.

- Bridge situations: You're buying now and planning to refinance once the property is stabilized.

- Cash-out strategy: You need to pull equity from one property to fund another move.

This is also why private lenders stay active in deals banks reject as "too complicated." Often, the deal isn't bad. It's just outside the narrow rules of conventional underwriting.

A short overview of how investors think about these trade-offs can help:

| Advantage | Why it matters |

|---|---|

| Speed | You can move on real timelines, not bank timelines |

| Flexibility | Transitional assets and imperfect borrower profiles can still be financeable |

| LLC-friendly structure | The borrowing entity can align with how you hold title and operate |

| Property focus | The value and performance of the real estate carry more weight |

To see how investors use this type of financing in the field, this short video gives a helpful overview.

Where borrowers get it wrong

The trade-offs are real. Short-term asset-based debt usually costs more than conventional financing, and the term is usually shorter. If your plan is vague, or your refinance path is weak, the loan can solve one problem and create another later.

What doesn't work is using short-term debt on a long-term hold with no clear takeout. What does work is using it intentionally, with a defined business plan and enough margin for execution.

One option in this category is LendingXpress, which structures asset-backed bridge, fix-and-flip, and rental property loans for non-owner-occupied residential and commercial assets. The fit depends on the property, loan structure, and exit plan.

If you're using a short-term loan, act like it's short-term from day one. Know your payoff strategy before you close, not after.

How Lenders Evaluate Your Asset-Based Deal

The phrase "asset-based" causes some borrowers to think underwriting gets easy. It doesn't. It gets narrower and more practical.

The lender isn't trying to read your entire financial life. The lender is trying to answer a more focused set of questions. Is the collateral solid? Is the financing appropriate? Can the property support the plan? Is there a believable way out of the loan?

The numbers and documents that usually matter most

In practice, lenders typically limit borrowing to around 70% loan-to-value, may require 20% to 30% down, and can close in 1 to 3 weeks because underwriting is focused on property-level data such as rent rolls and operating expenses rather than personal tax returns, according to Capital Source Group's discussion of real estate asset-based lending.

That doesn't mean the lender ignores the borrower. It means the lender looks at the borrower through the lens of execution risk.

Expect requests for items like:

- Property financials: Rent roll, leases, trailing income, and expense details if the property is operating.

- Valuation support: Appraisal, broker opinion, or rehab scope if value will change.

- Purchase and title documents: Contract, preliminary title, and entity vesting information.

- Liquidity proof: Enough cash to close and enough cushion to carry the project.

- Exit plan: Sale, refinance, or stabilization strategy that makes sense for the property type.

What makes a file move faster

The cleanest files answer the lender's real questions before the lender asks them.

If it's a rental, show current or projected income clearly. If it's a rehab, provide a real scope of work and budget. If the asset is in transition, explain why and show what stabilizes it. A rushed email saying "great deal, need to close fast" doesn't help much unless the package behind it is organized.

Here is a practical lender-side checklist:

Value support first

If the valuation story is weak or inconsistent, everything slows down.Explain the business plan in plain language

Buy, improve, lease, refinance. Or buy, renovate, sell. Simple wins.Match the loan term to the actual timeline

Don't assume a fast rehab or instant refinance if the property reality says otherwise.Disclose issues early

Vacancy, deferred maintenance, title concerns, partner disputes, unpaid taxes. Those are underwritable if surfaced early. They kill speed when hidden.

A lender can work through risk. What slows a deal down is unclear risk.

A good asset-based package is less about volume and more about precision. Give the lender a clear asset, a clean entity, and a realistic exit, and approvals tend to move much faster.

Structuring Your LLC for a Smooth Approval

A lot of borrowers focus on the property and ignore the entity. Then closing gets delayed by basic LLC issues that should have been fixed before the application started.

For asset-based real estate lending for LLCs, the entity doesn't need to be complicated. It needs to be clean. The lender wants to confirm who owns the company, who controls it, who can sign, and whether the borrowing structure creates problems elsewhere in the portfolio.

Keep the entity file clean

At a minimum, your LLC package should be internally consistent. The name on the purchase contract, formation documents, title, and bank records should line up. If the manager signs, the operating agreement should support that authority. If there are multiple members, ownership should be clear.

A separate business account also helps keep the file clean and supports the fact that the LLC is operating as its own business. If you're still sorting that out, this guide on opening an LLC bank account is a useful practical reference.

Borrowers usually move faster when they have these ready:

- Formation documents: Articles and any amendments.

- Operating agreement: Signed and current.

- EIN confirmation: Basic, but often overlooked.

- Bank statements: Enough to show liquidity and clean activity.

- Borrowing authorization: If required by the ownership structure.

Think carefully before pledging multiple properties

For LLCs with multiple assets, the lender's real question is how much flexibility the LLC keeps once the lender has a first lien. That includes whether one loan can trigger cross-default issues or affect financing on other assets, as discussed by Malve Capital on asset-based loans.

Entity structure matters more than many investors expect. A special-purpose LLC holding one property can be simpler to underwrite because the collateral and liabilities are easier to isolate. An operating LLC with several properties may still work, but the lender will look harder at intercompany relationships, existing liens, and whether one problem can spread across the rest of the portfolio.

If you're financing a rental or refinance through an entity, a business purpose mortgage for real estate investors can be a better structural fit than trying to adapt a consumer-style loan.

Clean entities close faster. Messy entities create legal questions, and legal questions slow money down.

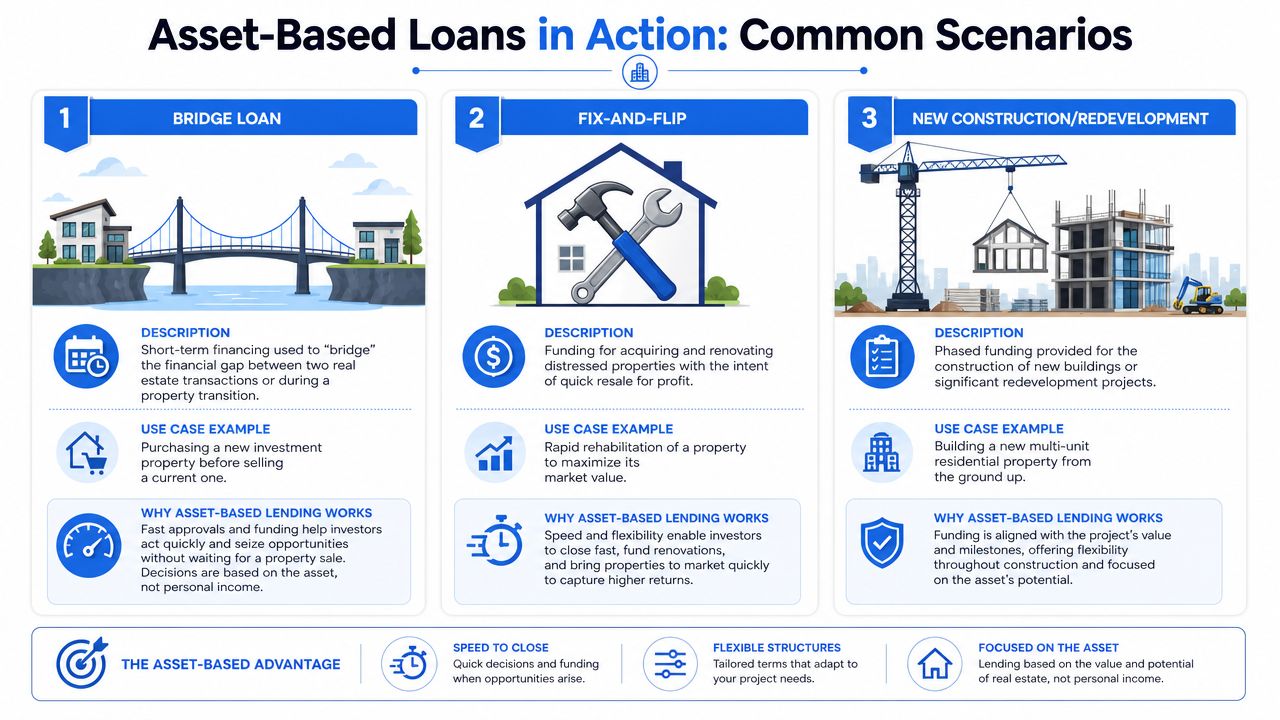

Asset-Based Loans in Action Common Scenarios

Borrowers usually understand this loan type once they see it in real situations. The structure changes depending on the deal, but the logic stays the same. The lender funds against the property and the plan, not just the borrower's personal income history.

Bridge loan on a transitional property

An investor has an LLC under contract on a small commercial property. The seller wants a fast closing. The building is partly vacant, and the current condition doesn't support conventional bank debt yet.

This is a typical bridge use. The lender focuses on current value, downside protection, and the borrower's plan to lease or improve the property before refinancing or selling. The term is short by design because the loan exists to get the borrower from today's condition to tomorrow's financeable condition.

Fix-and-flip with rehab execution

Another investor buys a distressed residential investment property through an LLC. The property needs cosmetic work, deferred maintenance repair, and a tighter construction budget than a bank wants to monitor.

The loan structure here often centers on purchase plus rehab, with draw management tied to project progress. The underwriting leans heavily on the condition of the asset, the renovation scope, and whether the after-repair plan is believable.

Rental acquisition or refinance without the usual borrower friction

A third scenario is a stabilized or near-stabilized rental. The borrower wants the property in an LLC and doesn't want the loan decision to hinge on personal tax returns that don't reflect the current investment picture.

In that case, the lender reviews the property income, operating expenses, title, valuation, and borrower liquidity. If the rent profile and collateral make sense, the loan can often move without the usual bank friction.

A simple comparison makes the use cases clearer:

| Loan Type | Primary Use | Typical Term | Key Underwriting Focus |

|---|---|---|---|

| Bridge loan | Fast acquisition, refinance gap, lease-up period | Short-term | Current collateral value and clear exit |

| Fix-and-flip loan | Purchase and renovation of distressed property | Short-term | Property condition, rehab scope, resale plan |

| Rental property loan | Buy or refinance income property held by an LLC | Medium to longer hold structure | Property cash flow, valuation, and entity readiness |

What works across all three is clarity. A lender can usually handle a property that needs work, a new LLC, or a borrower with a nontraditional income file. What doesn't work is a loose plan with no documented path to payoff.

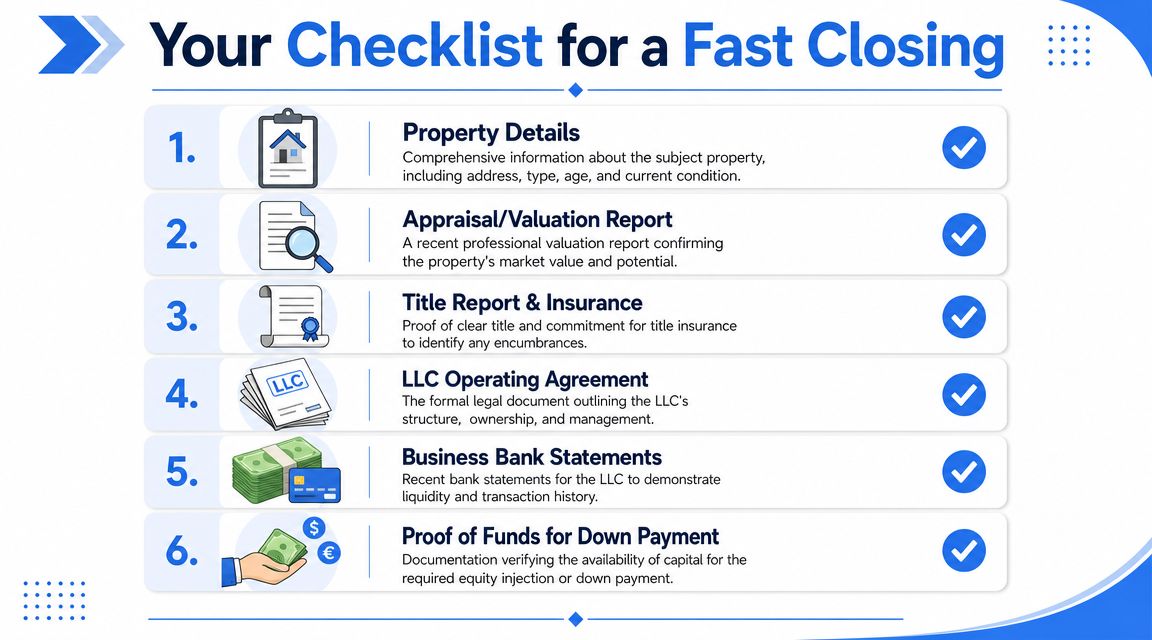

Your Checklist for a Fast Closing and FAQs

Most delays come from missing paperwork, unclear ownership, or an exit plan that lives only in the borrower's head. Fast closings happen when the file is organized before the lender starts chasing documents.

What to gather before you apply

Use this checklist before sending the deal out:

- Property package: Address, property type, current condition, occupancy, rent roll, and photos.

- Purchase or refinance details: Contract, payoff information, and a short explanation of the business purpose.

- LLC documents: Articles, operating agreement, EIN, and signing authority support.

- Liquidity evidence: Bank statements showing funds for down payment, reserves, and project carry.

- Valuation support: Any appraisal, broker value opinion, rehab scope, or budget already available.

- Exit summary: A few sentences on whether you'll sell, refinance, or stabilize and hold.

Common questions investors ask

Is asset-based lending the same as hard money?

They overlap, but they aren't always identical in how people use the terms. In practice, borrowers usually use both phrases to describe loans where the property carries the underwriting.

Can a new LLC qualify?

Yes, if the entity documents are clean and the deal itself makes sense. The lender cares more about the property, authority to borrow, and the guarantor's ability to execute than about the age of the LLC alone.

Is the loan really income-free?

Usually not. A better way to think about it is income-light. The lender may not rely on personal tax returns the way a bank would, but the property's financial story still matters.

Recourse or non-recourse?

That depends on the program, property, and risk profile. Many private real estate loans still include guarantees or some level of recourse, so you should ask early and review those provisions carefully.

Bring a lender a complete package, and you shorten the path to a decision. Bring fragments, and the clock starts over every time a new question appears.

If you're financing a non-owner-occupied property through an LLC and need a practical review of the deal, LendingXpress works on bridge, fix-and-flip, rental, and other asset-backed real estate scenarios where speed and flexibility matter.