A 1031 exchange is a tax-deferral tool that lets a real estate investor sell one investment property and reinvest the proceeds into another without immediately paying capital gains tax. Investors have exactly 45 days to identify replacement property and must complete the purchase within 180 days, which is why financing and coordination matter so much when the clock starts.

If you're holding a rental or commercial property with strong appreciation, you're probably looking at two competing goals. You want to sell and move into a better asset, but you don't want a large tax bill to strip away equity that could have gone into the next deal. That's where a 1031 exchange earns its place.

Used correctly, it helps you keep more capital working inside your portfolio. Used carelessly, it can fail on timing, structure, or financing. The investors who close these deals well usually don't treat a 1031 exchange like a tax form. They treat it like an execution challenge.

The Investor's Dilemma Selling a Profitable Property

You've owned a rental for years. The cash flow has been solid, tenants have paid down the loan, and the property has appreciated. Selling should feel like a win.

Then you realize the sale can trigger a tax bill right when you need that equity most.

That moment changes the conversation. Instead of asking, "Should I sell?" you start asking, "How do I move this money into a stronger property without losing momentum?" A 1031 exchange exists for exactly that reason. It gives investors a legal way to defer gain by rolling proceeds from one investment property into another qualifying property rather than cashing out.

This isn't some fringe tactic. Approximately 10% to 20% of all commercial real estate transactions in the United States involve a 1031 exchange, which shows how central it is to real estate capital strategy (National Association of Realtors summary).

Why investors keep using it

A successful exchange lets you do a few important things at once:

- Keep equity in play: More of your sale proceeds stay available for the next acquisition.

- Trade into a better fit: You can move from a smaller asset to a larger one, or from a management-heavy property into something simpler.

- Reposition the portfolio: Some investors consolidate. Others diversify across asset types or locations.

A 1031 exchange matters most when the sale is profitable and you don't want taxes to interrupt your next move.

The attraction isn't complexity. It's control. You worked to build the equity. The exchange helps you redeploy it instead of watching a chunk of it leave the deal at closing.

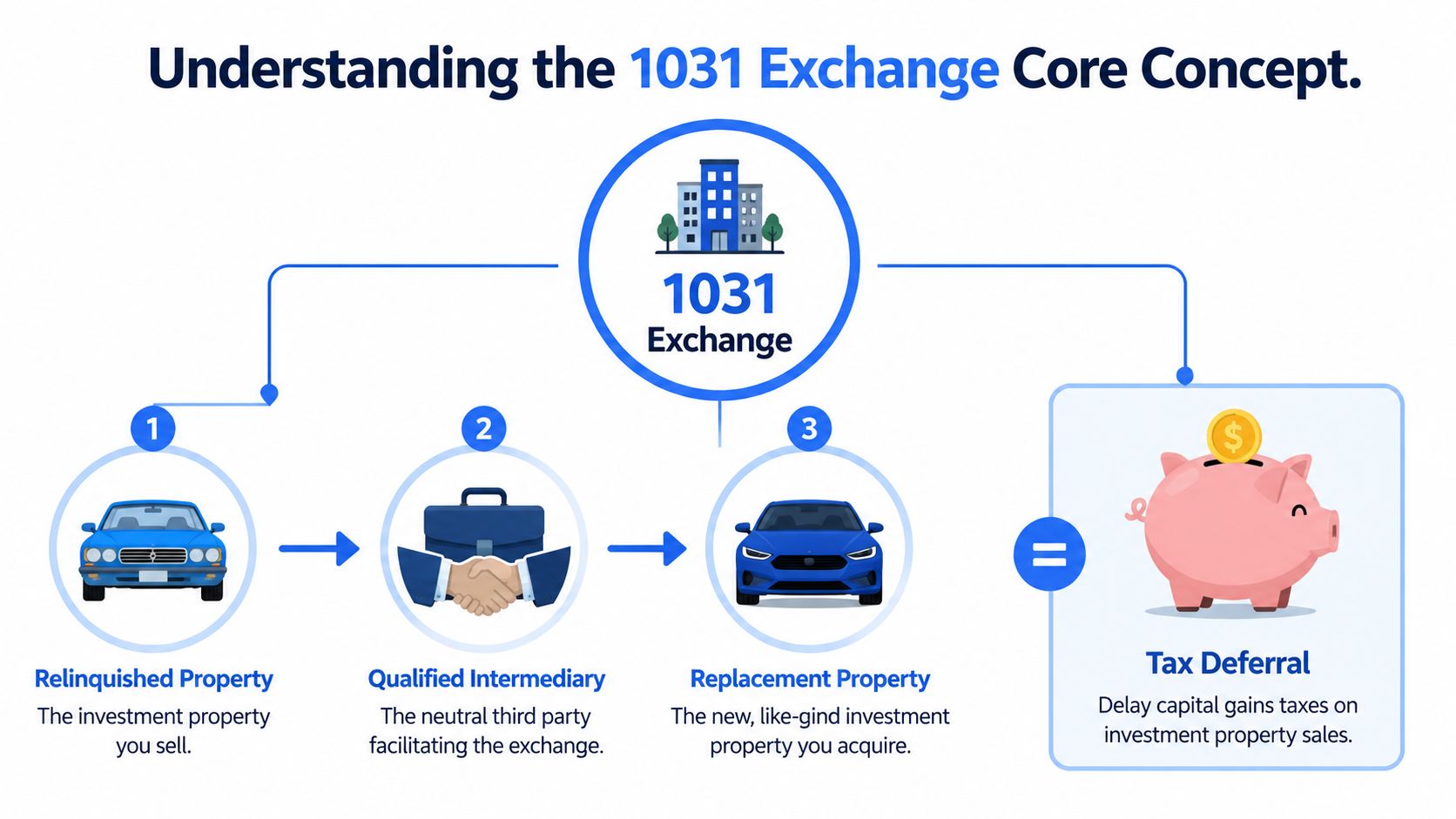

Understanding the 1031 Exchange Core Concept

What is a 1031 exchange? It's a way to defer tax, not erase it.

It's like trading one business tool for another better-suited tool. You're not stepping out of investment activity and pocketing the cash. You're continuing the investment by moving from one property into another. The tax on gain is postponed as long as the exchange is structured properly.

If you want a second plain-English walkthrough after this one, the Top Wealth Guide on 1031 exchanges is a useful companion resource.

Tax-deferred is not tax-free

Many investors misinterpret the nature of a 1031 exchange. It doesn't make the gain disappear. Rather, it postpones recognition of gain until a later taxable event, assuming you follow the exchange rules and don't receive the sale proceeds directly.

The IRS makes that distinction clear in its explanation of exchange treatment and taxable boot (IRS fact sheet on Section 1031 exchanges).

The three terms that matter most

Here are the concepts worth understanding before you get fancy:

- Relinquished property: The investment property you sell.

- Replacement property: The investment property you buy as part of the exchange.

- Qualified Intermediary: The neutral third party who holds the funds so you don't take possession of them.

If you touch the proceeds, the exchange can collapse. That's why the money doesn't flow from closing straight into your bank account.

What like-kind usually means in practice

For real estate investors, like-kind often sounds narrower than it is. In practical terms, investment or business real estate can usually be exchanged for other investment or business real estate. You're generally not limited to swapping the same property type for itself.

A rental house can be exchanged into a small apartment building. A retail property can be exchanged into another investment asset. The key is investment or business use, not cosmetic similarity.

What boot means

Boot is any cash or non-like-kind value you receive in the exchange. That's the leftover value that can become taxable.

Practical rule: Full deferral usually means reinvesting all net equity and replacing equal or greater debt so you don't create taxable boot at closing.

That single point explains why exchange financing matters so much. Even when the tax strategy is sound, poor loan structure can create a surprise tax result.

Navigating the Critical 1031 Timelines and Rules

A 1031 exchange is won or lost on process. The rules aren't flexible, and the timeline starts the day the old property closes.

The two deadlines you can't miss

Investors have exactly 45 days from the sale of the relinquished property to identify replacement properties in writing, and the entire exchange must be completed no later than 180 days after the sale (Fidelity's overview of 1031 exchange timing rules).

Those aren't target dates. They're hard stops.

Miss the identification deadline, and the exchange can fail. Miss the closing deadline, and the gain can become immediately taxable.

What has to happen before closing the sale

Most exchange problems don't start after the sale. They start before it, when the investor assumes they can figure out the replacement purchase later.

That's risky. Before your sale closes, line up:

- Your Qualified Intermediary: They need to be in place before proceeds move.

- Your replacement property strategy: You should already know what kinds of assets you're targeting.

- Your financing path: Lender conversations, documentation, and fallback options should begin early.

- Your closing team: Broker, escrow, title, attorney or tax counsel, and lender all need the same calendar.

The replacement purchase can't be improvised once the identification window begins.

The role of the Qualified Intermediary

The Qualified Intermediary is not a side character. They're central to the exchange structure.

Their job is to hold the proceeds and facilitate the exchange so you don't have actual or constructive receipt of the funds. If the money passes through your hands, you've undercut the tax deferral mechanism.

A simple checklist helps:

| Step | What needs to happen |

|---|---|

| Sale closing | Proceeds go to the Qualified Intermediary, not to you |

| Identification period | Replacement properties are identified in writing |

| Purchase period | One identified property is acquired before the deadline |

Where investors usually get stuck

Not on the rules themselves. The rules are simple. The friction shows up in execution.

Common trouble spots include:

- Financing delays: Appraisal, underwriting, or lender conditions can drag.

- Title issues: Clouds on title can slow a scheduled closing.

- Unclear identification: Loose descriptions or incomplete paperwork can create problems.

- Debt mismatch: A replacement purchase with less debt or less equity can trigger boot.

The investors who handle exchanges well build margin into every step. They don't plan to close on the last possible day unless they have no other option.

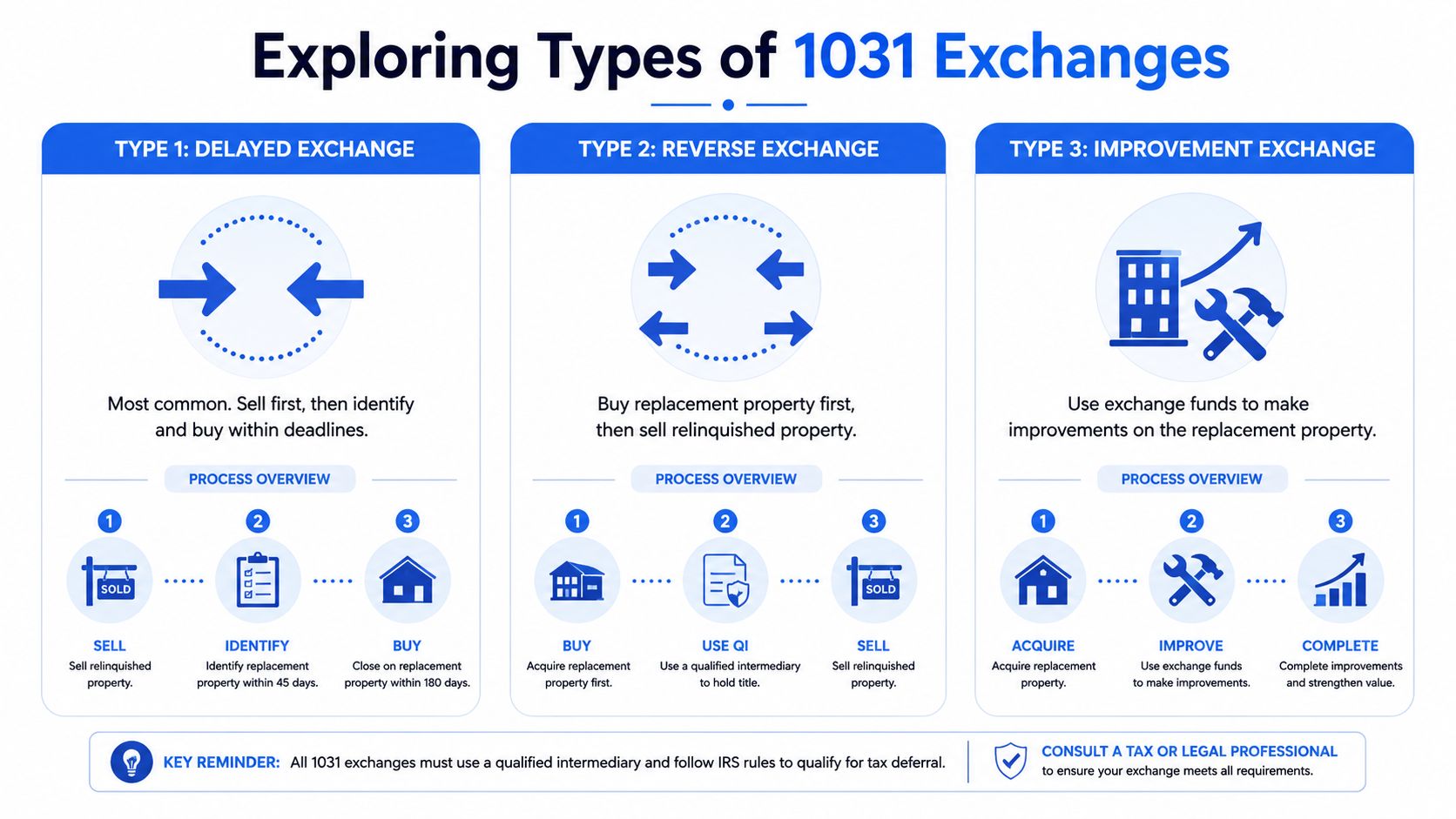

Exploring Different Types of 1031 Exchanges

Hearing "1031 exchange" often evokes the standard sell-then-buy sequence. That's the delayed exchange, and it's the most familiar version. But it's not the only structure.

Delayed exchange

This is the classic model. You sell first, then identify and acquire the replacement property within the required timeline.

It fits investors who already have a marketable asset and a decent pipeline of possible replacements. The challenge is obvious. Once the sale closes, the countdown begins, and every financing or escrow delay matters more.

Reverse exchange

A reverse exchange flips the sequence. You acquire the replacement property first, then sell the relinquished property afterward.

This structure can help when you've found a rare asset and don't want to risk losing it while waiting for your current property to sell. It can also help in competitive markets where sellers prefer buyers who can move quickly and cleanly.

The tradeoff is complexity. Holding the new property while the old one is still in play often requires sharper coordination and more flexible capital.

Improvement exchange

An improvement exchange, sometimes called a build-to-suit exchange, is designed for investors who want the replacement property to be upgraded as part of the exchange strategy.

This can make sense when the right location is available but the asset needs work to meet your investment plan. Instead of waiting to renovate later, the exchange structure can support improvements tied to the replacement property.

Which one solves your problem

A quick comparison makes the use case clearer:

| Exchange type | Best fit | Main challenge |

|---|---|---|

| Delayed | You can sell first and buy soon after | Time pressure after sale |

| Reverse | You need to secure the new property first | More complex structure and funding |

| Improvement | The new property needs work to match your plan | Construction and timeline coordination |

Choose the exchange structure based on the problem you're solving, not on what sounds most familiar.

A lot of investors default to delayed exchanges because that's what they hear about most often. But if your real issue is timing, scarce inventory, or a property that needs rehab, a different structure may fit better.

A Real World 1031 Exchange Example

A simple example makes the mechanics easier to see. Let's use a fictional investor named Sarah.

She owns a duplex that's been a solid rental for years. Rents have gone up, the property has appreciated, and management has become more hands-on than she wants. She'd rather own a small apartment building with on-site management potential and stronger long-term scale.

How Sarah structures the deal

Sarah lists and sells the duplex. Before closing, she hires a Qualified Intermediary so the sale proceeds don't go to her directly. She also talks with her broker and lender in advance because she knows the replacement purchase has to move fast.

After closing, she doesn't wait around to "see what's out there." She tours candidates immediately, reviews rent rolls, and works with her team to identify several replacement options in writing before the identification deadline expires.

That step matters. She isn't picking one dream property and hoping everything goes perfectly. She's building backup choices in case inspection, title, or financing issues knock out the first target.

Where financing becomes the real issue

Sarah finds the apartment building she wants, but the seller wants a buyer who can close without drama. A conventional bank process could work, but only if everything moves smoothly. That uncertainty is what worries her.

The exchange itself may be valid, but if the financing drags and the closing slips too far, the tax deferral can still collapse.

In a 1031 exchange, the tax strategy and the financing strategy are really the same strategy. If the loan doesn't close, the exchange doesn't close.

A short video can help if you want to hear the concept explained another way:

What the successful outcome looks like

Sarah closes on the replacement property within the required window. Her exchange funds move through the intermediary into the new acquisition, and she keeps her equity working in real estate instead of reducing it with an immediate tax payment.

The practical result is more important than the paperwork. She traded out of a smaller, management-heavy asset and into a property that better matches her next stage of investing.

That's the power of a 1031 exchange. It lets an investor reposition, scale, or simplify without taking a tax hit at every sale along the way.

The Critical Role of Financing in a 1031 Exchange

Most failed exchanges don't fail because the investor misunderstood the concept. They fail because the replacement purchase doesn't close in time.

That's why financing deserves more attention than it usually gets.

Why traditional loan timing can be a problem

Banks can be a fit for some investment properties, but a 1031 exchange creates a different kind of pressure. The deadlines are rigid. Sellers want confidence. Underwriting conditions can change late. Appraisals, document requests, committee review, and title cleanup can all eat up time you don't have.

When you're buying a replacement asset under deadline, certainty often matters as much as rate.

What flexible financing actually solves

Private money and hard money aren't just fallback tools for borrowers who can't qualify conventionally. In a 1031 exchange, they can be execution tools.

They can help investors:

- Move faster: Faster decisions can make a replacement offer more competitive.

- Handle unusual properties: Mixed-use, value-add, or transitional assets may not fit cleanly into a bank box.

- Bridge the timing gap: An investor can secure the replacement property first, then refinance later if that makes sense.

- Reduce closing risk: A financing plan built around the exchange timeline can prevent last-minute failure.

If you're comparing options, this guide on how to finance investment property gives a practical look at loan paths for non-owner-occupied deals.

Why this matters most under pressure

The hardest exchange deals usually involve one of three things: a seller who won't wait, a property with quirks, or a borrower whose timeline is tighter than a bank likes. That's where private lending becomes strategic rather than optional.

For example, a bridge lender may help you close the replacement property quickly, preserve the exchange, and give you time to stabilize or refinance later. That can be more valuable than chasing the lowest possible rate and missing the deadline.

LendingXpress is one example of a private lender that works on non-owner-occupied real estate and structures bridge and investment-property loans when timing is tight. In the context of a 1031 exchange, that kind of financing can support a fast acquisition when a conventional process doesn't line up with the clock.

If your exchange timeline is tight, don't start by asking who has the cheapest money. Start by asking who can actually close inside your deadline.

Common Questions and Is a 1031 Exchange Right for You

A few questions come up almost every time.

Common investor questions

- Can you use a 1031 exchange for a personal residence? No. The exchange is for property held for investment or business use, not for a primary home.

- Can you take some cash out? Yes, but that cash can create taxable boot.

- What happens if the exchange fails? The deferred gain can become taxable.

- Can vacation property qualify? It depends on whether it's held for investment rather than personal use, so this is a point to review carefully with tax and legal advisors.

If your deal involves a complicated closing, title issue, entity question, or local legal wrinkle, it's smart to have counsel involved early. For California investors dealing with Los Angeles transactions, Lerner & Weiss for LA property law is a useful legal resource.

When a 1031 exchange makes sense

A 1031 exchange is often a strong fit when you want to:

- Scale up: Move into a larger or better-performing asset

- Simplify management: Trade several properties for one, or move into a different asset type

- Reposition equity: Shift your portfolio without immediate tax friction

It may be less attractive if you want full liquidity now, don't want the compliance burden, or aren't prepared to move quickly.

One practical test

Ask yourself this. Do you want cash, or do you want continued investment exposure?

If you want to stay invested, a 1031 exchange can be one of the cleanest tools available. If you need liquidity for other purposes, forcing an exchange can create stress and bad buying decisions.

And if your next move depends on pulling equity after the replacement property is in place, it helps to understand how investors use tools like a cash-out refinance on a rental property later in the cycle.

A good exchange starts long before the sale closes. It starts with the right team, the right backup plan, and financing that matches the actual timeline.

If you're working on a non-owner-occupied purchase, bridge loan, or time-sensitive exchange and need financing that can move on investor timelines, LendingXpress is worth a look. The right lender won't make the 1031 rules easier, but they can make it much more realistic to close the replacement property before the deadline runs out.